*Special thanks to @BidenCho for feedback and review.

Hyperliquid is facing immense competition from new perp DEXs — Aster, Lighter, EdgeX and others.

Liquidity is highly incentive-driven, leading to short-term outflows of volume and capital toward new DEXs; yet Hyperliquid continues to hold a clear lead in open interest and user metrics.

The perp DEX market is likely to consolidate into a few winners; Hyperliquid’s infra, initiatives, and HyperEVM ecosystem position it to remain central.

In markets, success is rarely permanent. Each time a business demonstrates an attractive model, competitors inevitably emerge, often armed with imitation, incentives, or innovations of their own. The lesson, repeated across industries, is that no advantage is untested for long. This principle is as old as capitalism itself, and we’re watching it play out in real time within the emerging world of perp DEXes.

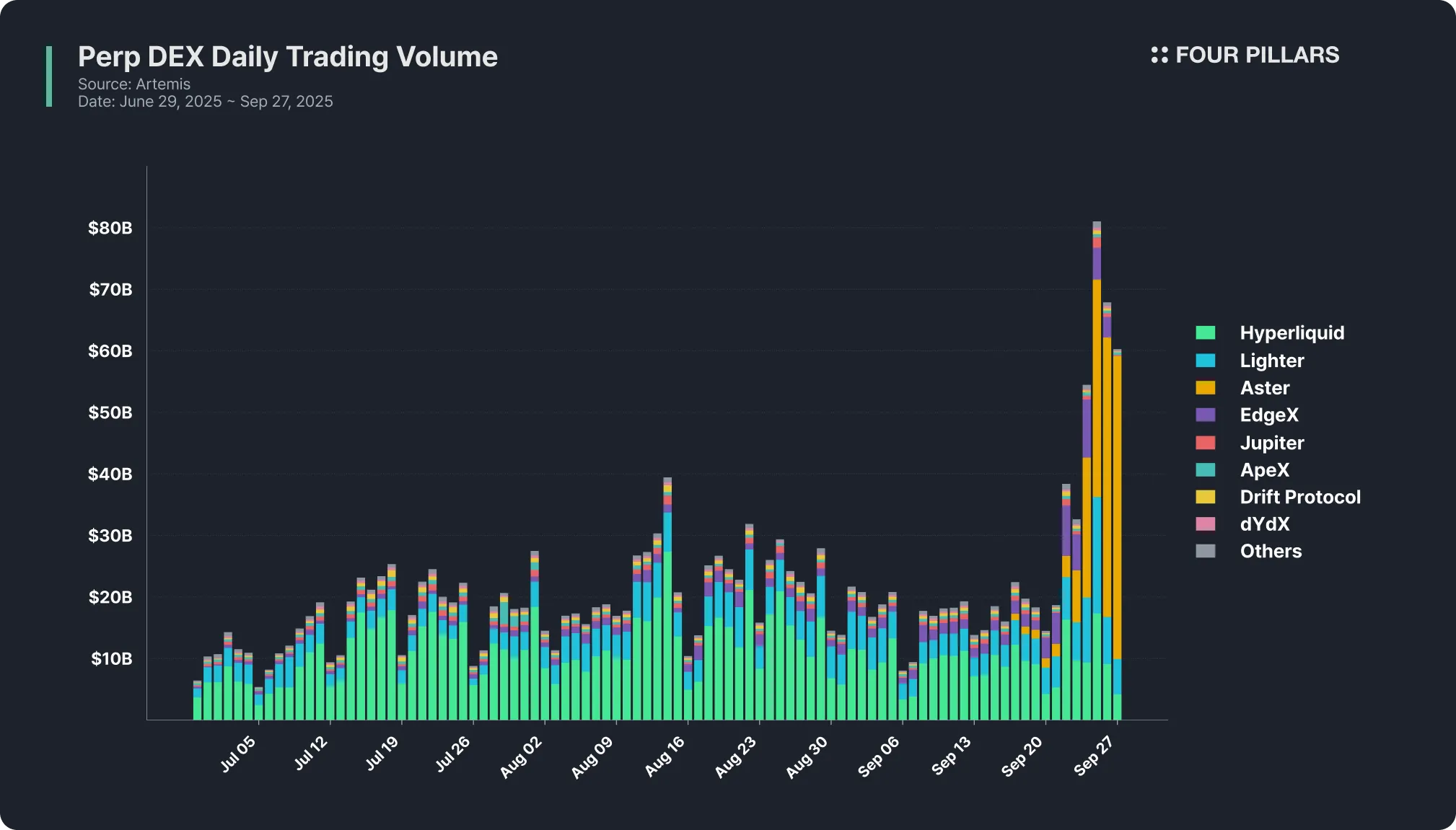

Hyperliquid is now under siege. After proving that a CLOB could work securely and at scale on a custom blockchain, it attracted users, liquidity, and recognition as the clear category leader. But recent weeks have shown that leadership invites challengers. A wave of perp DEXes (Aster, Lighter, EdgeX, Pacifica, Avantis, etc) have launched with the same core playbook: points based farming, aggressive airdrop promises, and headline grabbing incentives.

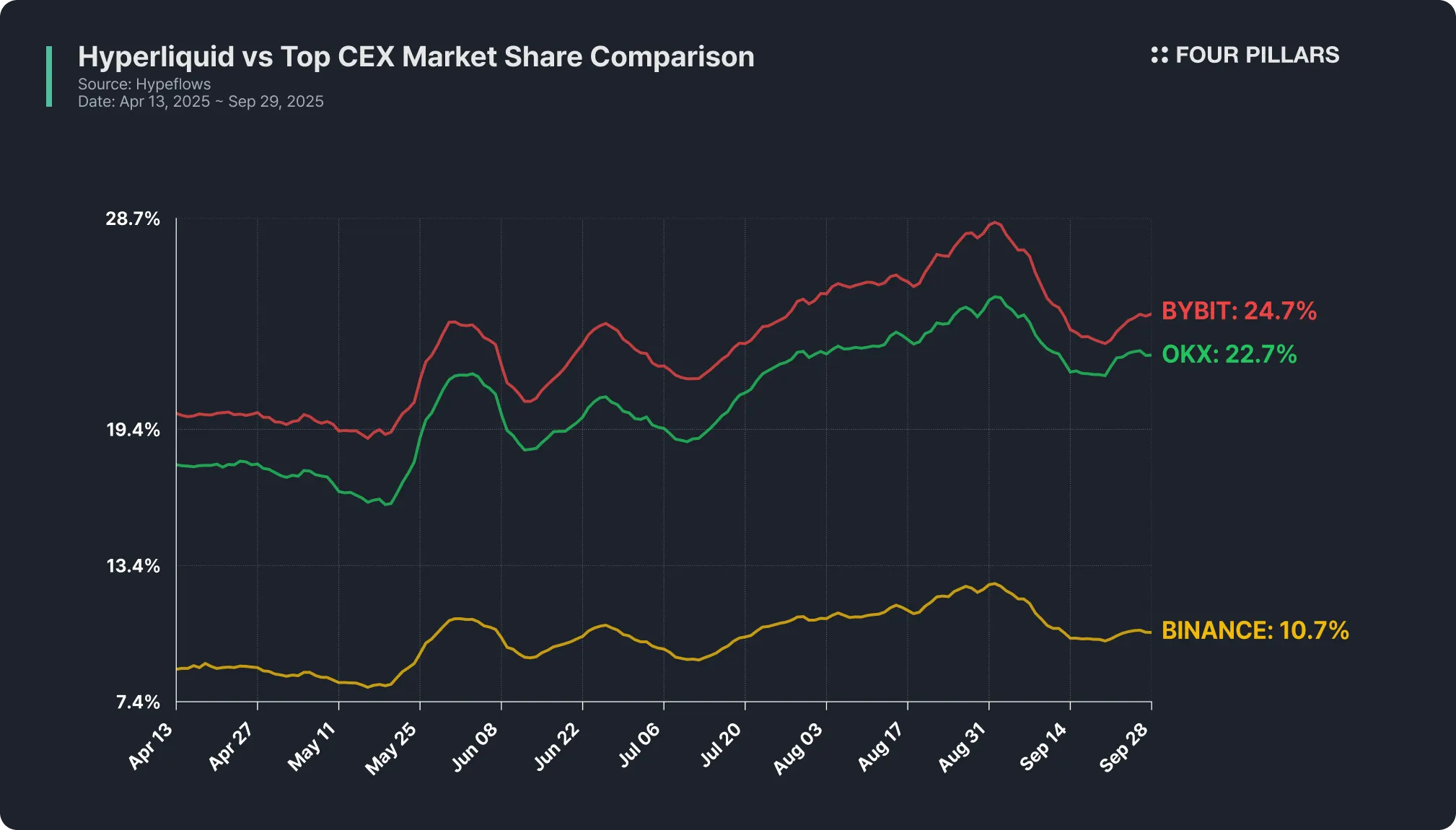

On a single day in late September, Aster and Lighter recorded $42.8 billion and $5.7 billion, respectively, in daily volume, surpassing Hyperliquid’s ~$4.6 billion. Other newcomers like EdgeX are not far behind, clearing $3.3 billion. To casual observers, it looked as if Hyperliquid had been dethroned. Just months earlier, it commanded over 70% of the entire on-chain perps market. Suddenly, it was ranked second or even third.

But context matters. Hyperliquid still processed nearly $300 billion in trading volume over that same month, a scale none of the newcomers have approached on a sustained basis. Active users and open interest, a better measure of capital commitment than one-day activity, has also remained far higher on Hyperliquid.

Liquidity is inherently mobile. Traders seek not only the best execution but also the best rewards. In crypto, where token incentives can dwarf trading fees, capital often behaves mercenarily, flowing to whichever venue is currently most lucrative.

That doesn’t mean all liquidity is the same. Some portion is opportunistic, arriving for yield and leaving just as quickly. Another portion is stickier, tied to confidence in a platform’s infrastructure, reputation, and long-term value proposition. The crucial question for Hyperliquid is how much of its liquidity is mercenary versus how much is durable.

Conventional wisdom holds that once incentives decline, farmers move on and incumbents reclaim their share. But it also forces us to ask: What if the meta of nomadic liquidity (constantly cycling from one pre-token platform to the next) becomes the new equilibrium?

In that world, the advantage of having already launched a token could paradoxically become a liability.

Hyperliquid is not only facing emerging competitors but also strategic adversaries with deep resources. The presence of Binance and its founder, CZ. Binance has long been known for aggressive competition. Many believe its actions hastened the downfall of FTX. With Hyperliquid now regularly processing +10% of Binance’s volume, it is only natural that CZ would notice.

His first action was listing perpetual contracts on $JELLYJELLY at the height of the incident, a move seen by the market as an attempt to amplify volatility and strain Hyperliquid’s liquidity pool (HLP) by increasing margin and liquidation risk.

Subsequently, CZ threw his weight behind Aster, a BNB chain DEX he had invested in. Still, Aster’s success is likely secondary. I believe CZ’s real objective is to disrupt Hyperliquid’s momentum, fragmenting capital and attention across rivals. Even if Aster never matches Hyperliquid’s scale, its role as a distraction already serves the purpose.

This strategy is rational from Binance’s perspective: fragmented competition prevents any one on-chain rival from consolidating too much power. Divide and conquer has been a classic tactic in business wars.

Bene Gesserit recites: “I must not fear. Fear is the mind-killer. Fear is the little-death that brings total obliteration.”

Markets often confirm this wisdom. Fear often does more damage than fundamentals.

Hyperliquid’s biggest risk today may not be any single rival, but the creeping perception that loyalty doesn’t pay. If traders come to believe they must constantly chase the next airdrop, then Hyperliquid’s long-term community cohesion weakens. FOMO becomes the true adversary.

It is now more important than ever for investors to distinguish between temporary disruption and lasting erosion. The discipline is not to deny fear but to acknowledge it, let it pass through, and return to fundamentals.

That said, it’s also worth remembering that this market is still young. Perp DEXs today may resemble CEXs in the late 2010s~early 2020s when Binance, Huobi, Gate.io, BitMEX, Bybit, and OKX were still fighting for dominance.

In time, we’ll likely see a similar consolidation among DEXs, where a handful emerge as the giants. The incentive battles now playing out are not the end state of the industry but part of its growing pains.

DEXs are now entering their own period of contest.

The war for liquidity is far from over. Hyperliquid faces serious tests from both opportunistic rivals and entrenched giants. Yet several factors suggest the odds remain in its favor:

Superior infra & dev ecosystem: Hyperliquid is a full L1 with a best-in-class CLOB engine and a robust developer community building on HyperEVM. Competitors operating only as standalone DEXs cannot easily replicate this foundation.

Trend setting initiatives: From HIP-3 to its native stablecoin, Hyperliquid has consistently set the pace. The USDH ticker auction was one of crypto’s most fiercely contested events, drawing participation from all major players, and native markets ultimately prevailed. With 50% of USDH revenue allocated to buybacks and AF, Hyperliquid is uniquely positioned among L1s to capture stablecoin revenues as well as protocol fees generated across multiple frontends via HIP-3.

Stickier liquidity: While daily volumes have fluctuated, Hyperliquid continues to dominate in open interest and active users. These metrics suggest that a loyal core base of traders remains anchored to the platform.

Season 3 points program (speculative): Updates to the points page suggest that a new Season 3 program is imminent. Incentive distribution has always been a Hyperliquid strength, with 38.8% of $HYPE supply reserved for community rewards worth roughly $5.8 billion at current prices. No competitor can match this incentive pool.

HyperEVM TGEs: Upcoming anticipated HyperEVM token launches (UNIT, Kinetiq, Felix, etc.) will recycle liquidity back into the ecosystem and deepen $HYPE’s role. This evolution from just a DEX into a broader L1 platform could drive meaningful revaluation.

As with all investments, we deal in probabilities, not certainties. The hope for Hyperliquid is that when today’s turbulence subsides, it will emerge stronger, wiser, and still the leader in the market.

Dive into 'Narratives' that will be important in the next year