Power in exchanges is shifting from asset custody to liquidity coordination.

HIP-3 turns exchange creation into an on-chain primitive, standardizing matching, margin, and settlement.

Modular design now splits into CEX “compliance modularity” and Hyperliquid “sovereign modularity.”

Hyperliquid captures value through network effects of staked HYPE, builder incentives, and composable markets.

Markets learn more from failure than calm. Events like Mt. Gox, FTX, and Binance’s Oct 10 incident (where a pricing flaw valuing collateral with its own order-book data cascaded into network-wide API failures, latency spikes, halted deposits, and downtime) show how centralized systems repeatedly fracture under stress.

It’s easy to call this the end of CEXs. It isn’t. Custodial exchanges remain essential for fiat rails and regulatory access. But the source of power is changing. What once depended on holding deposits now depends on managing liquidity flow.

Hyperliquid showed why. During the same stress, its markets cleared and liquidations executed transparently on-chain. That resilience signaled a structural shift. Moreover, with the rise of HIP-3, market creation itself is becoming permissionless and programmable.

The conversation is no longer CEX vs DEX, but Empires vs Networks—compliance and custody on one side, composability and routing on the other. This report examines how those two architectures diverge and how they will coexist.

For the past decade, centralized exchanges have acted as the sovereigns of digital liquidity. Binance, Coinbase, Bybit, and Upbit became self-contained economies: tokens as fiscal policy, KYC as border control, fees as taxation, custody as authority. Whoever held user assets controlled the market.

The model worked because it solved three problems simultaneously. Users needed stability and speed, regulators demanded identifiable intermediaries, and market makers required deep, predictable liquidity.

By 2024, the top 10 perp CEXes in 2024 had $58.5T total perp volume across the year, and the open interest (OI) on those perp CEXes crossed $100B. For most participants, trusting an exchange was faster and cheaper than rebuilding financial infrastructure from scratch.

But scale bred opacity. As exchanges absorbed more functions (custody, trading, clearing, and staking), they began to resemble banks with private ledgers. Most operate internalized clearing systems, off-chain balance sheets, and settlement processes that outsiders cannot verify.

This is not moral judgment. Regulation remains the most reliable coordination layer for global finance, and custodial hubs are still needed for fiat conversion. But their structural dominance is clearly weakening. On-chain systems that can self-clear under stress are eroding the monopoly on trust.

On-chain derivatives volumes rising relative to centralized venues, Source: The Block

Empires will not disappear, but their rule will be balanced by networks that trade control for transparency and speed for composability.

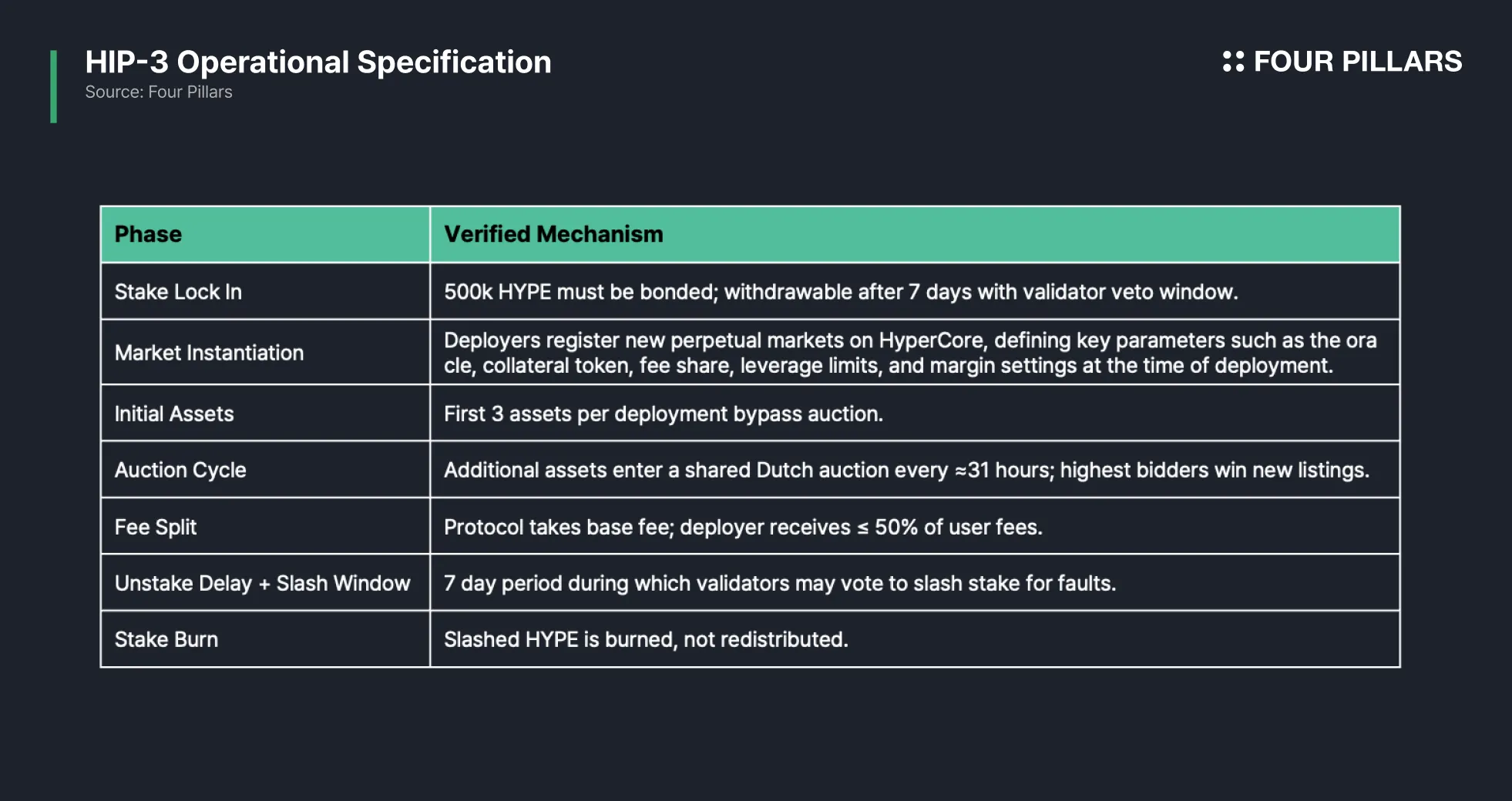

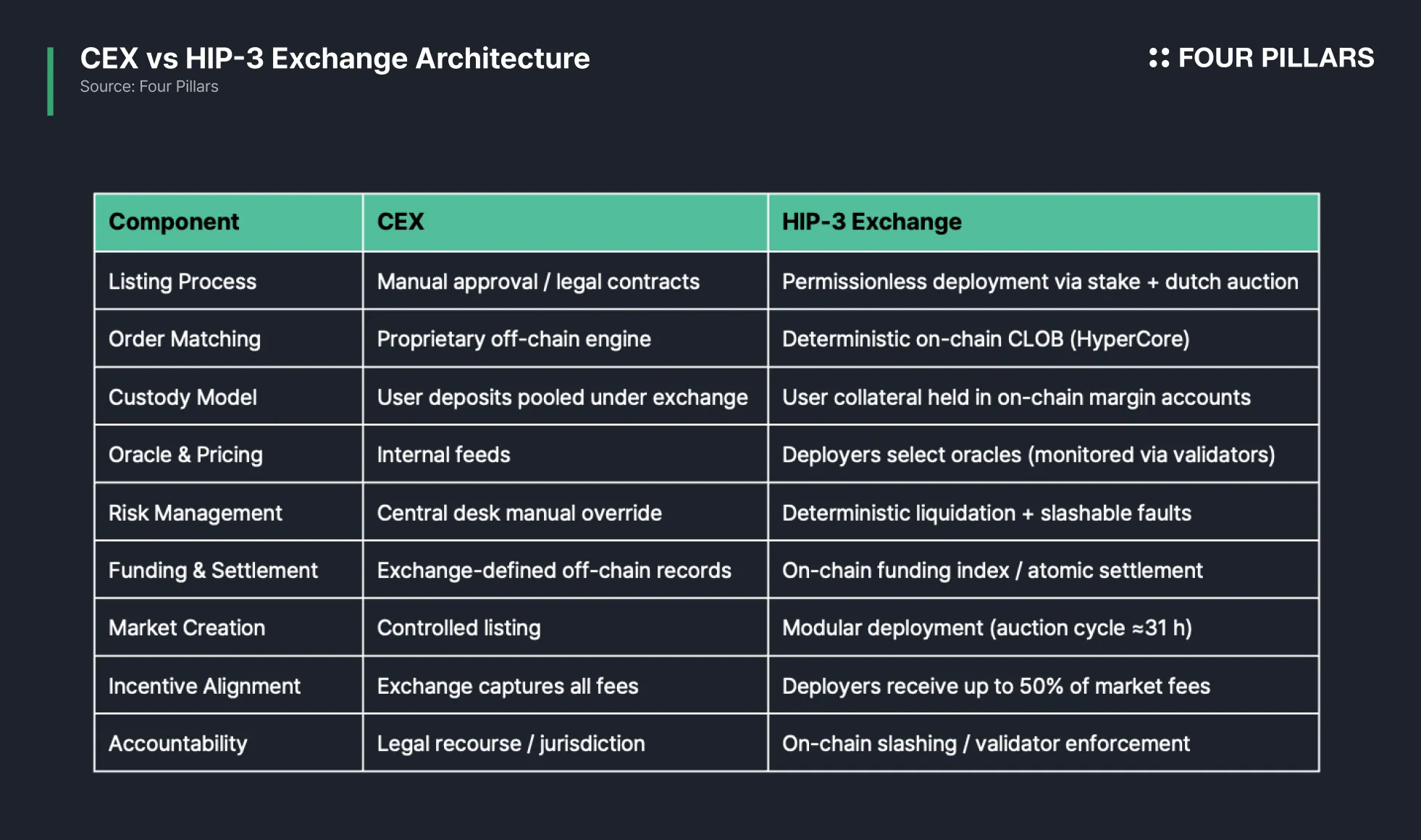

HIP-3 marks the moment when exchange architecture stopped being a corporate product and became a programmable network. It moves the listing process from approval to execution, transforming exchange creation into an on-chain primitive. Under HIP-3, any builder who stakes 500k HYPE can deploy their own perpetual DEX on HyperCore, complete with independent order books, collateral settings, oracle feeds, and fee structures. Each deployment inherits Hyperliquid’s deterministic CLOB engine, real-time margin logic, and settlement layer—the same infrastructure that powers the main exchange.

This permissionless design replaces bureaucracy with code. HIP-3 replaces vertical integration with horizontal replication. Each deployment becomes a sovereign market that shares a unified state layer. Liquidity no longer scales by accumulation, but by replication. Builders compete on design, not access, and Hyperliquid’s core infrastructure guarantees identical execution quality across every market.

Naturally, the backend becomes a commodity; differentiation shifts to how builders attract users and liquidity.

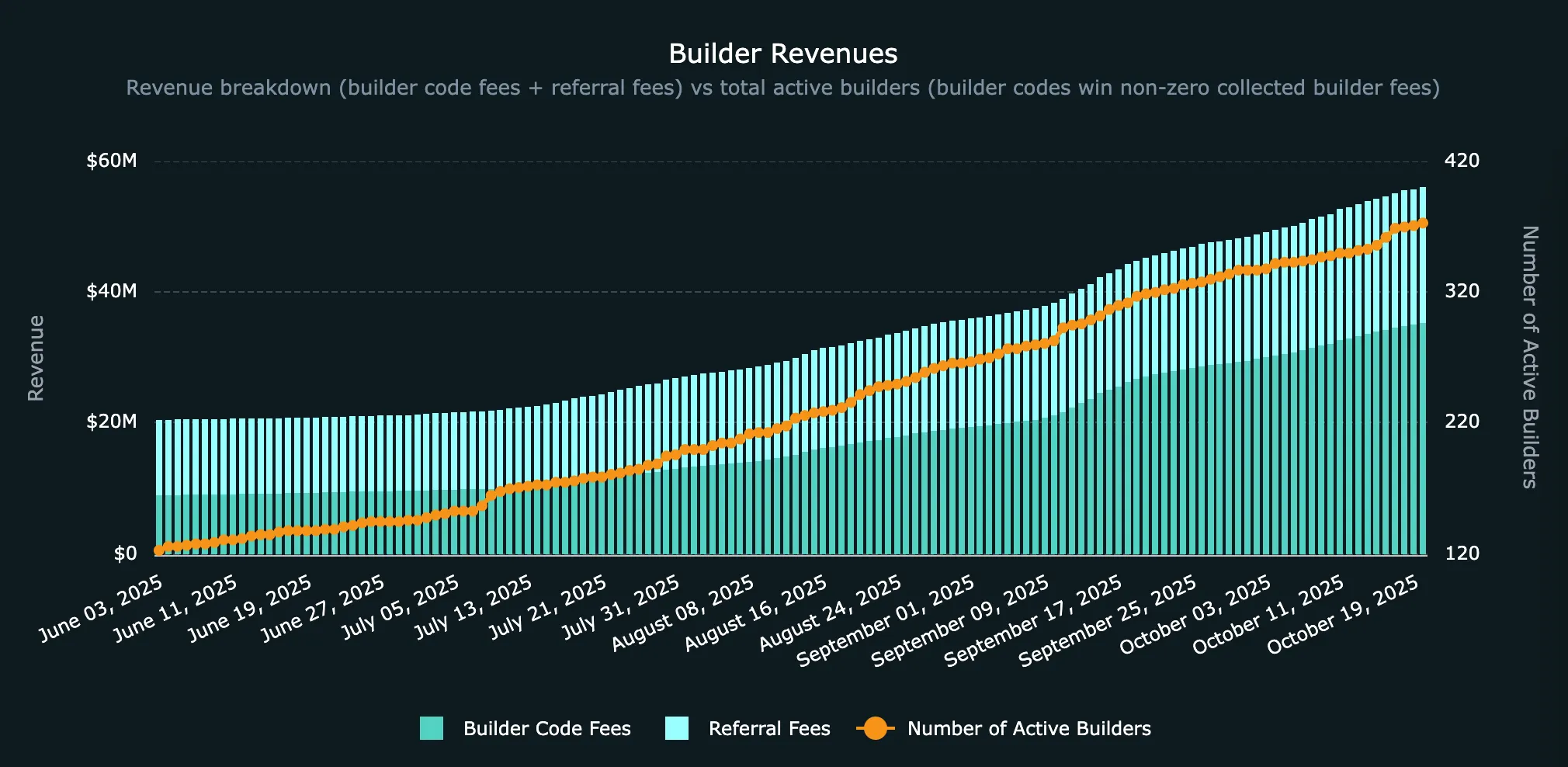

The same modular logic is now appearing at the incentive layer. Through Builder Codes, Hyperliquid allows routing agents and front-ends to earn on-chain fees from orders executed on the main exchange. While separate from HIP-3, these mechanisms share its philosophy: transforming what used to be internal, opaque exchange economics into open, verifiable participation. In both cases, value creation migrates from centralized operators to a distributed network of builders.

For market makers, this standardization compresses friction. They can quote and hedge across dozens of HIP-3 markets through the same API and margin account, treating the entire network as one extended trading surface. This plug-and-play participation results in a federation of markets connected by shared infrastructure rather than corporate ownership.

Understanding how this new architecture actually operates requires a closer look at its internal mechanics.

As mentioned above, each HIP-3 deployment runs its own independent orderbook but inherits the same HyperCore execution engine, settlement layer, and margin logic. This shared architecture guarantees determinism across markets. Builders act as deployers, routers act as coordinators, and validators enforce solvency and correctness at the protocol level.

The exchange ceases to be a fortress of deposits and becomes a network of liquidity endpoints. The old model captured value by storing assets; the new one captures it by orchestrating motion.

Hyperliquid’s liquidity is fully on-chain. Users deposit USDT/ USDC through Router Protocol’s Nitro bridge, which connects more than 30 chains to HyperCore. Once funds enter, they’re held in on-chain margin accounts, enabling traders and market makers to provide depth across all perpetual markets with the same capital base.

All HIP-3 markets share the same HyperCore matching and settlement layer. Capital remains inside the same margin system, allowing liquidity to be reallocated between HIP-3 and core markets without off-chain transfers or custodial friction.

HIP-3 is already attracting a set of launch partners that illustrate how the model scales:

Kinetiq Launch: EaaS (“Exchange-as-a-Service”) infrastructure helping projects bootstrap HIP-3 markets collectively, using pooled HYPE stakes.

Ventuals: building pre-IPO perpetuals, bringing private-market exposure on-chain.

trade.xyz (HyperUnit): creating synthetic equity perps integrated with HyperEVM spot trading.

Matching Engine: All HIP-3 markets inherit the same deterministic CLOB engine used by Hyperliquid’s primary exchange. Matching occurs with on-chain sequencing and sub-second finality.

Market Makers: Liquidity providers connect via a unified API and shared margin account, allowing strategies to extend across multiple HIP-3 markets. Cross-market netting is conceptually supported but may remain isolated until governance formalizes margin-sharing standards.

Oracles: Deployers choose oracle sources from either Hyperliquid’s native feeds or external data providers. The current spec defines this process at a high level; exact oracle-validation parameters remain under design review.

Margin & Liquidation: HIP-3 uses isolated margin per market. Liquidations execute automatically when maintenance thresholds are breached, with outcomes recorded on-chain. Cross-margining may be active in the future.

Funding Mechanics & Event Perps: Funding rates follow the base protocol formula. HIP-4 is intended to introduce event-driven perps (contracts that settle on binary or continuous real-world outcomes) but these remain pre-launch/speculative.

A builder first bonds 500k HYPE, which remains locked and slashable for 7 days after unstaking begins. Once staked, the deployer registers new perps market on Hypercore, specifying key parameters such as oracle, collateral token, fee share, and margin tiers.

According to HIP-3, the first 3 assets listed under a new builder-deployed perpetual DEX bypass the shared Dutch auction. From the 4th asset onward, listings compete in a pool wide Dutch auction held approximately every 31 hours. Trading fees are split between the protocol and deployer, while validators oversee performance and can initiate slashing for faults—a mechanism explained in the next section.

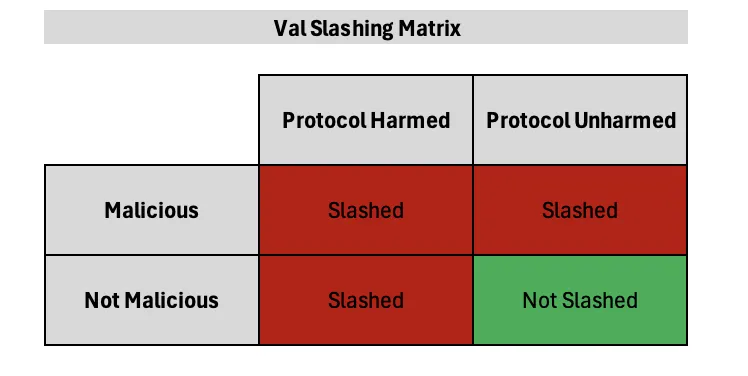

HIP-3 introduces one of the first functional slashing frameworks in exchange architecture. The validator set votes to slash deployer stakes when markets behave in ways that jeopardize network correctness, uptime, or user solvency.

Source: X (@Guthix)

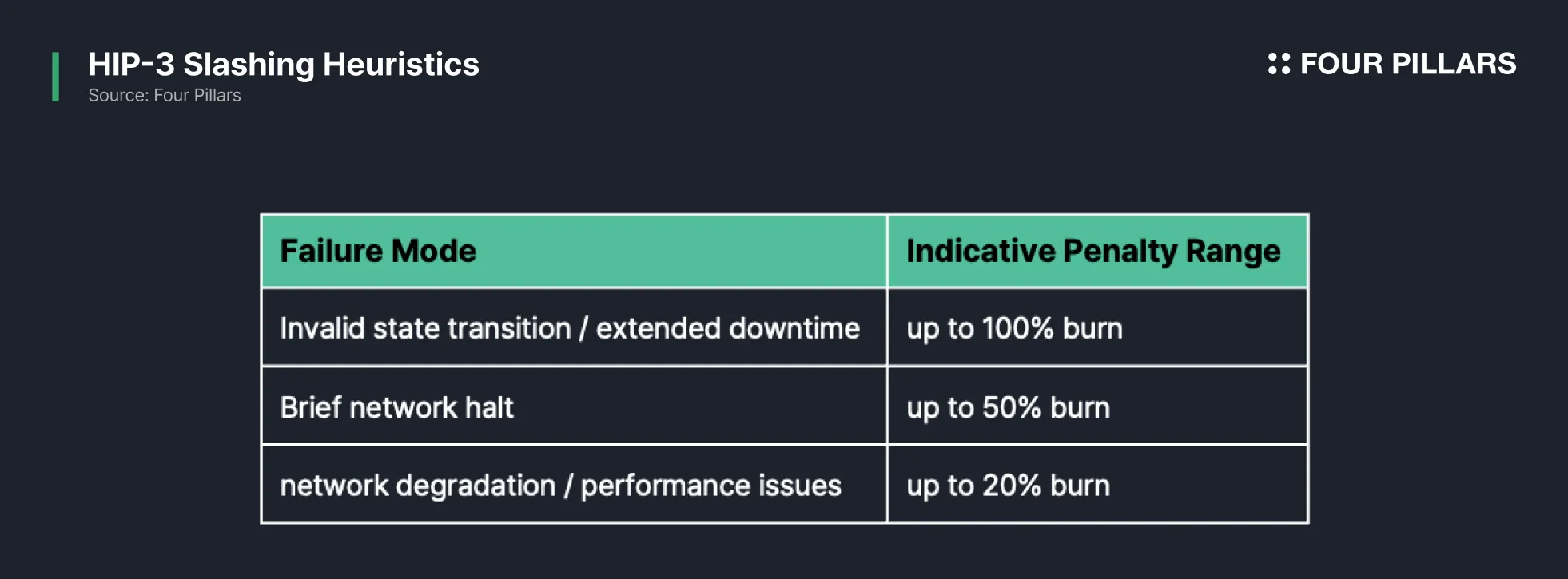

As @GuthixHL summarized: “Slashed stake does not compensate user losses; it is burned. This prevents HIP-3 stake looting and incentive misalignment.” Penalties are proportional to fault severity and may include:

Any slashable behavior should be accompanied by a bug fix in the protocol implementation. Slashed HYPE is burned, not redistributed, removing incentive for validator coalitions to exploit operator mistakes. This converts what used to be reputation risk into on-chain accountability.

As deployments scale, validator decisions are expected to establish a de facto precedent layer—a form of technical “case law” defining operational standards for permissionless exchanges. While this structure strengthens correctness and accountability, it also introduces the need for standardized incident response.

Under HIP-3, every core mechanism (matching, margining, liquidation, funding, routing) is standardized, verifiable, and modular. The system remains under active iteration.

As modularization spreads, we are witnessing exchanges diverging (for now) into two design paths. Both are modular approaches, but they modularize different things.

CEX-chains such as Base, BNB Chain, Mantle, and Giwa (Upbit) represent what can be called compliance modularity. They don’t decentralize their core businesses or migrate matching engines on-chain. Instead, they build public blockchains that act as brand satellites and extend the exchange’s reach into the on-chain economy while keeping custody, listings, and risk management centralized. It is a strategy of controlled openness (public infrastructure orbiting around private governance).

Networks like Hyperliquid pursue the opposite logic—sovereign modularity. Since HIP-3 makes market creation itself permissionless, deployers replicate exchange functionality horizontally, each running sovereign orderbooks.

In this environment, capital (to bootstrap initial liquidity and incentives), frontend design, and user relationships define who wins.

Even within the core exchange, Builder Codes distribute a share of fees directly to the interfaces and algorithms that generate order flow, showing how Hyperliquid’s modular approach extends from market creation to incentive design.

Empires modularize control to persist; networks modularize creation to expand.

Empires anchor fiat and institutional trust; networks generate velocity, experimentation, and innovation.

Both paths are rational responses to their constraints.

At its core, Hyperliquid is attempting to redistribute how power and responsibility are structured. Through HIP-3, it aims to spread liquidity formation across many actors instead of concentrating it within a single operator. Market deployers, oracle providers, and validators share responsibilities once monopolized by centralized risk desks. Authority becomes modular. Each participant governs a narrow slice of the system (risk parameters, oracles, settlement), but none possess the full stack.

In theory, this is what an on-chain exchange environment could look like when scaled: specialization replaces hierarchy, and coordination replaces custody as the organizing principle.

The transition will appear messy at first. Dozens of HIP-3 markets will launch, fragmenting depth and widening spreads. Yet fragmentation is the precondition for network density. Once standards, tooling, and arbitrage mature, liquidity reconverges through competition and replication.

Crucially, its value ultimately converges on Hyperliquid itself. Every new HIP-3 market channels trading activity, fees, and validator participation back through HyperCore, compounding the protocol’s economic gravity.

Each deployment requires a 500k $HYPE stake, effectively locking that amount out of circulation for the life of the market and creating a recurring supply sink as more builders join. Demand for deployer stakes and validator collateral reinforces the monetary loop of $HYPE, whose role spans governance, staking security, and network coordination.

As the number of markets expands, Hyperliquid’s network effect strengthens. Liquidity begets liquidity, and protocol value compounds through usage. The result is that technical capability alone no longer determines value capture.

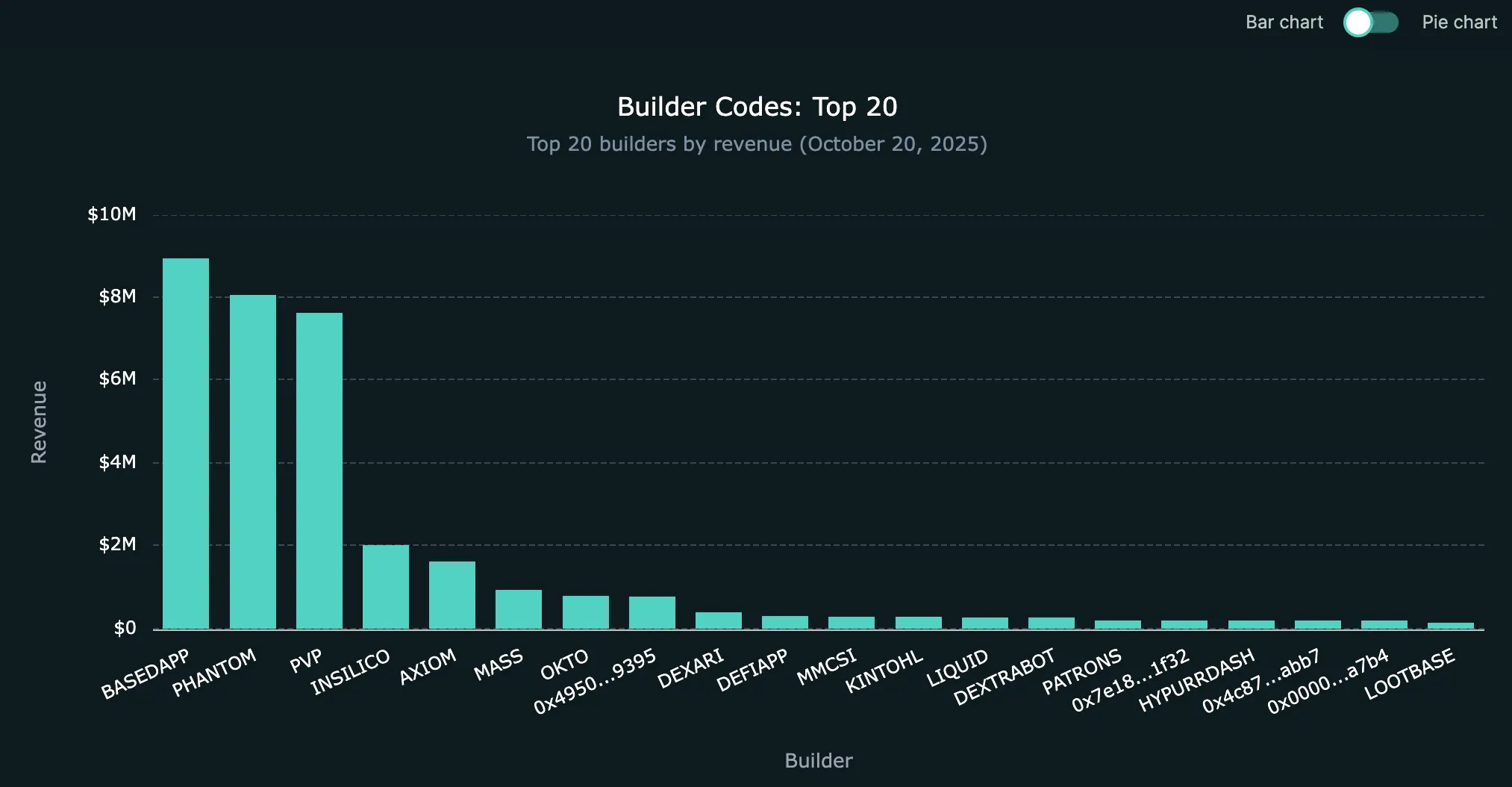

Beyond HIP-3’s market deployments, Hyperliquid’s core exchange is already showing what a modular incentive system looks like in practice. Since mid-2024, Builder Codes have distributed over $60 million in on-chain fees to more than 400 active builders. The revenue flow is concentrated but increasingly competitive. The top earners (BasedApp, Phantom, PVP Trading, and Insilico) have each generated between $3 million and $6 million USDC in cumulative fees by routing order flow through their own frontends and APIs.

Builder-level fee distribution illustrates how liquidity incentives are now protocol-native, Source: hypeburn.fun

These numbers are hard coded into Hyperliquid’s fee logic and settled entirely on-chain. Every time a user trades through a builder’s interface, a fraction of the trading fee (up to 0.1% on perps, 1% on spot) is streamed directly to that builder’s wallet. As trading volume compounds, so does this distributed revenue base, turning what used to be a centralized fee monopoly into an open income layer for infrastructure contributors.

The second-order effect is expansion. New markets bring new users, from equities and commodities to pre-IPO shares and prediction markets. When liquidity ceases to cannibalize itself and starts absorbing new surfaces of value, the market dynamic shifts from pure PvP competition to a PvE-like expansion phase here capital creation becomes the dominant game.

The contest ahead is not between CEXs and DEXs; it’s between two models of financial governance. Empires rule liquidity through regulatory durability while networks coordinate it through code. Both exist to manufacture trust, yet they express it differently.

Empires built walls; networks built links.

Empires own infrastructure. Networks ARE infrastructure.

In this new paradigm, the backend of exchange infrastructure becomes commoditized. Matching, margining, and liquidation are open primitives anyone can deploy through HIP-3. The only real bottlenecks left are capital and user attention. Competitiveness no longer comes from building engines but from giving users differentiated value on top of a shared liquidity fabric.

Dive into 'Narratives' that will be important in the next year