The value capture narrative in blockchain has moved from protocols to applications, and more recently to wallets that have absorbed functions such as swaps and bridges and now sit directly on the user touchpoint. This evolution has even produced the Fat Wallet thesis, which argues that wallets will lead ecosystem value capture. However, DApps can still build defenses that wallets cannot easily breach by leveraging temporal depth, meaning inertia rooted in user experience, and functional depth, meaning capabilities that cut to the essence of the market. These two forms of depth can give DApps durable, independent competitive advantages.

Solana uses a rent model in which accounts deposit a refundable reserve to cover data storage costs at creation. Even after users sell their tokens, accounts whose token balance is zero are not automatically closed, which has led to the accumulation of about 607 million potentially stranded accounts. Liquidity locked inside truly abandoned "zombie ATAs" is estimated at at least 110,000 SOL, creating a large rent recovery market

Sol Incinerator captured this market by offering a utility that finds and returns rent users did not realize they had locked up. As of November 2025, it had returned more than 470,000 SOL in total and recorded a reuse rate close to 80%, establishing clear category leadership. This shows that even when later entrants introduced additional incentives such as referrals or gamification, users still chose an intuitive workflow focused on the core outcome, asset recovery, along with trust that had already been validated in the market.

Wallets, leveraging their advantage as the starting point for user transactions and often promoting a zero fee policy, embedded rent recovery features directly into the wallet. However, due to inherent constraints around security risk management and maintaining a general purpose UX, they could not implement DApp level sophisticated filtering or mass burn logic. As a result, they were unable to surpass the DApp's functional depth, which maximizes both expertise and convenience.

While Anza's announced plan to reduce rent suggests the market's size may change, the value capture battle that played out inside this niche is still instructive. Even if wallets control the Web3 "on-ramp," DApps can survive independently in the Fat Wallet era if they differentiate themselves as the "destination" that solves user problems completely and with specialized expertise.

The blockchain industry's discourse has, over time, shifted around a central question: where is value captured? In the early days, the conversation was dominated by the protocol layer, with debate centered on consensus algorithms, throughput, and security. The Fat Protocol view, which argued that protocols providing foundational technology would absorb ecosystem value, became widely accepted. As Ethereum gained traction, alternative L1s such as Solana, as well as various L2s, rose to prominence and a competitive landscape among protocols took shape.

As performance across major L1s and L2s converged and multi chain environments became common, the center of gravity for value capture moved from infrastructure to services. From 2017 to 2018, killer apps such as OpenSea and Uniswap emerged and began capturing user touchpoints and fee revenue, reinforcing the Fat Application thesis that applications would become the primary locus of value capture. DApps became core components of the ecosystem, not merely interfaces, but systems that generate transactions and fees. This is also why base layer protocols increasingly focus on onboarding DApps via grant programs and hackathons.

Source: imgflip.com

That said, in Web3 it is difficult for the application layer to monopolize value in the persistent way that Web2 platforms often do. Many blockchain based DApps publish core logic on chain to earn trust, which structurally lowers the difficulty of forks and composability. Once a successful example appears, copycat DApps with similar functionality can spread quickly, not only within the same chain but also across different execution environments. In other words, applications may have risen as a center of value capture, but competition has become correspondingly intense.

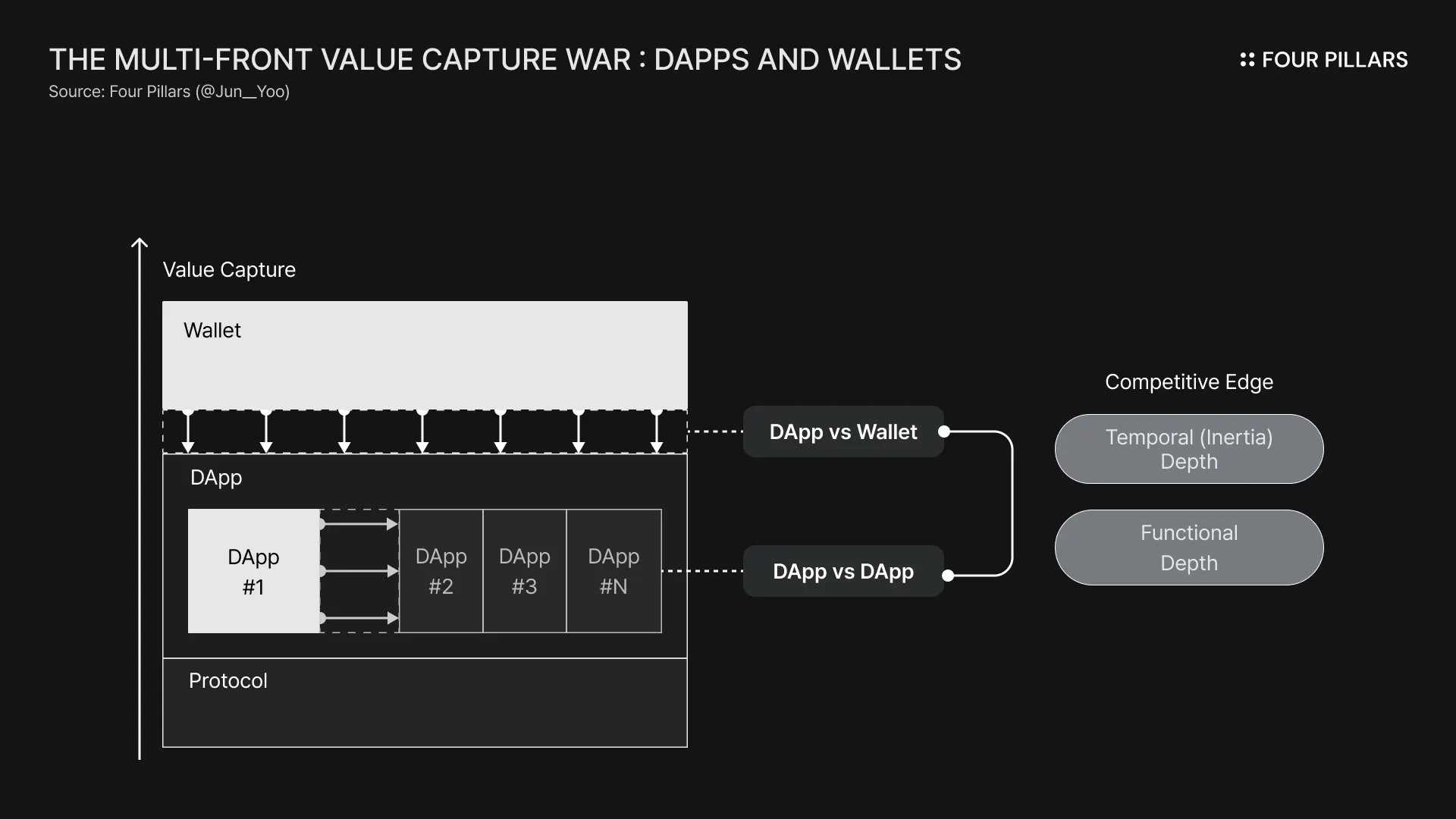

Against this backdrop, the renewed question becomes: who controls the entry point of user transactions? This question has recently evolved into the Fat Wallet thesis. Wallets sit on the front line connecting users to chains, controlling transaction creation and signatures. They are also evolving into super apps by absorbing DApp functionality such as swaps, bridges, and staking. Wallets already capture value through on and off ramp fees and by controlling order flow. In particular, as blockchain expands into retail finance closely tied to the real economy, including real world assets (RWA) and payments, the center of value capture is shifting beyond applications toward wallets that reshape distribution and flows.

The rise of the Fat Wallet thesis does not mean the role of DApps will immediately shrink. What is clear, however, is that the competitive axis facing DApps has expanded from DApp versus DApp to DApp versus wallet. In a market already crowded with DApps offering similar functionality, wallets embedding those core features forces DApps to prove competitiveness in an even narrower space for differentiation.

In this environment, where boundaries across layers have blurred, the key variables that determine competitive advantage are as follows.

First is temporal depth, meaning inertia rooted in user experience. Unless there is an exceptional situation such as an overwhelming performance gap in infrastructure or an unusually aggressive incentive, users do not easily change familiar workflows. This is not mere preference, but the result of repeated experience and accumulated trust. A wallet offering convenience at a similar level is not enough to replace entrenched usage patterns. Especially in a copycat environment where technical replication is easy, this kind of time based depth becomes one of the strongest defensive moats for DApps.

Second is functional depth. At one time, the ability to capture value depended on the simple accumulation of features. But as countless protocols, DApps, and wallets have entered the market, feature lists have lost their power to differentiate. What matters now is whether each layer understands the essence of the market it targets and builds the kind of functional depth that directly hits that essence. Advanced trading options, robust exception handling, and sophisticated automation in perpetual futures DEXs are representative examples. This is not about stacking features, but about creating depth that penetrates the core needs of a specific market.

Ultimately, competitiveness in value capture is moving away from feature checklists and toward either temporal depth, which keeps users anchored, or functional depth, which solves the market's true problems. This article analyzes Solana's rent recovery market as a case study that makes this competitive structure especially clear. The market is small and its function appears simple, but it is a near-perfect example of how DApps can maintain advantage, and why wallet-led value capture attempts run into structural limits.

In simplified terms, Solana's execution environment can be understood as a system that stores state at the account level. Much of the on chain information, including program code, program state, user data, and token balances, is separated and managed as accounts. The execution environment that runs on top of this structure is the Solana Virtual Machine (SVM).

When data is managed at the account level, increased network activity also implies an increase in the number of accounts that must be created and maintained. If accounts could be created and kept forever at zero cost, the amount of state every node must store would grow without bound, wasting network resources.

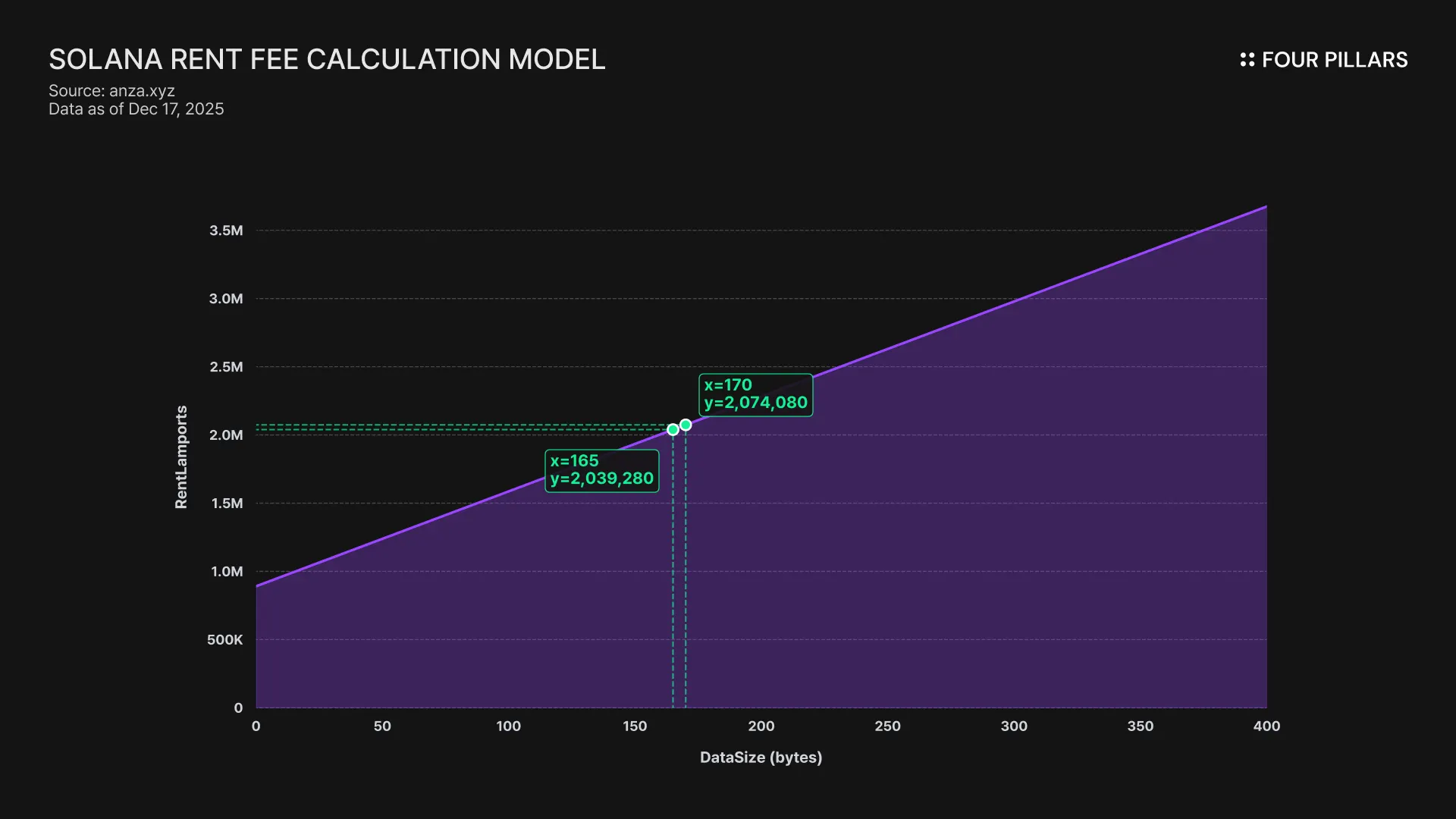

To mitigate this, Solana introduced rent as an economic opportunity cost model. The principle is that occupying storage, a public good, should require paying a cost proportional to the amount of data stored. In the past, there was a mechanism that deducted rent from an account's balance each epoch. Today, however, most newly created accounts operate under a model where a refundable deposit is paid at creation to make the account rent exempt. This deposit stays locked as long as the account remains open.

The deposit required for rent exemption is calculated roughly as follows.

Source: Solana Labs GitHub repository

In short, the larger the account's data size, the larger the required deposit. For example, holding an SPL token requires a dedicated account associated with a wallet address and a token mint. This is called an Associated Token Account (ATA). An ATA is a dedicated account bound to a wallet address and token mint, and it records the token balance for that wallet. An ATA typically uses 165 bytes of space, and creating it requires a rent exempt deposit of about 0.00204 SOL.

For convenience, this report refers to the rent exempt deposit as “rent" as well.

The problem is that even if a user sells or transfers all tokens and the balance becomes zero, the ATA is not automatically removed. Without explicit cleanup, the zero balance account remains on chain and the deposit continues to stay locked. In this report, we will refer to an ATA whose utility is gone, with a token balance of zero but a stranded deposit, as a "zombie ATA."

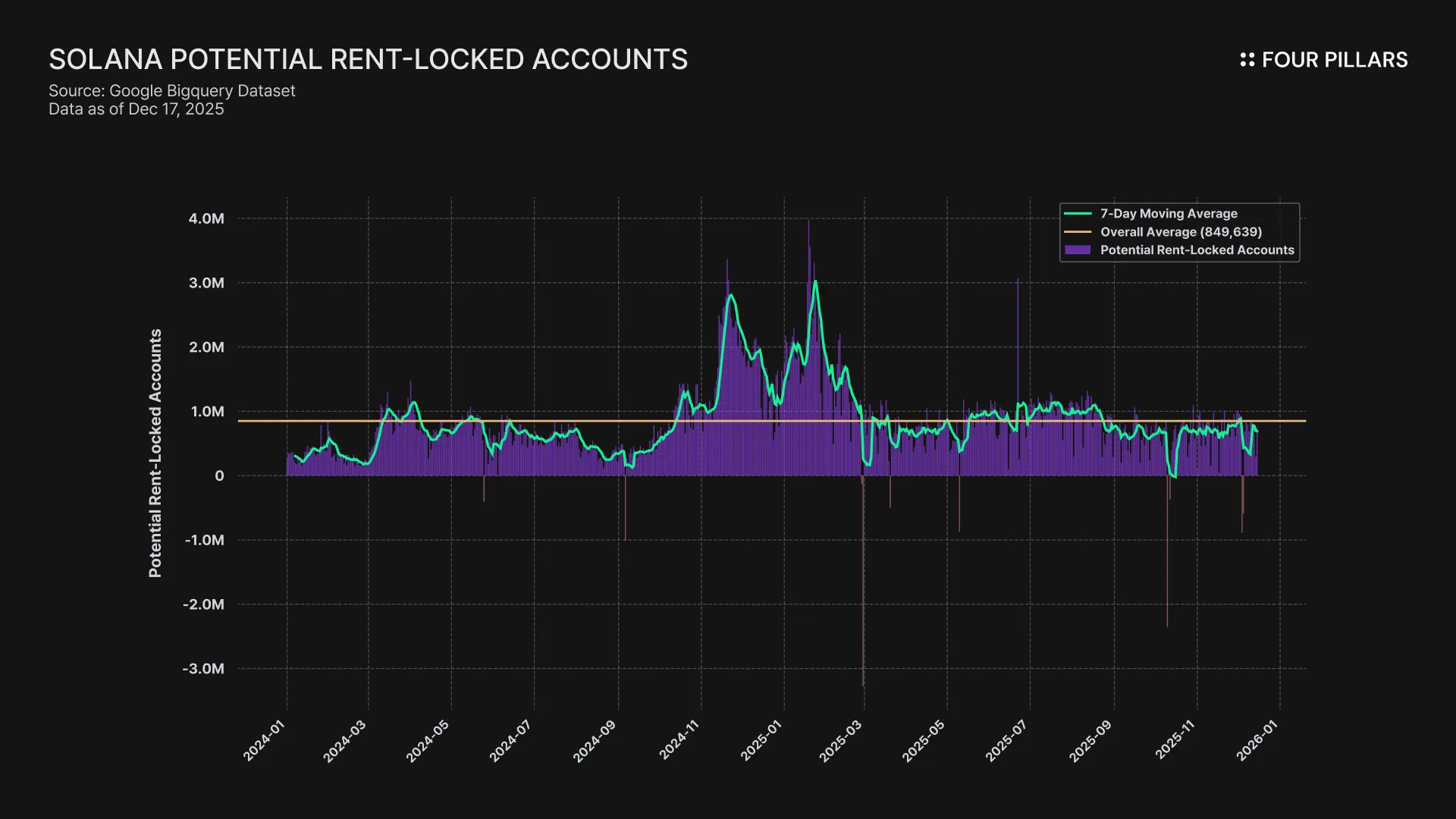

To understand the accumulation of zombie ATAs on Solana and the market potential implied by rent recovery, we analyzed the period from January 1, 2024 to December 15, 2025, roughly 715 days, and tracked 191.5 billion transactions using Solana's public dataset provided by Google BigQuery.

Given Solana's data scale, it is practically infeasible to conduct a full census of real time balances for every ATA. Instead, this analysis tracks account creation and closure events that occur during major token activities such as minting, burning, and swapping. Rather than matching each account state one to one, we estimate the scale of "potentially stranded accounts" by comparing net changes in event counts and identifying accounts that were created but not closed.

The results of this analysis are as follows.

Analysis start date: January 1, 2024

Cumulative accounts with observed state changes (opened or closed): 3.11 billion

Average daily unclosed accounts: 850,000

Cumulative unclosed accounts since the start date: 607 million

Considering common user inertia, meaning users often do not immediately close accounts even after selling all tokens, the "potentially stranded accounts" metric serves as a key indicator for estimating the scale of zombie ATAs. In particular, as meme coin activity accelerated in the second half of 2024, driven by platforms such as Pump.fun, about 850,000 accounts per day have been newly entering the stranded state. As a result, at least 607 million accounts have been counted as remaining unclosed since January 1, 2024.

To estimate the actual proportion of zombie ATAs within this large universe, we sampled 100,000 accounts that conform to the standard ATA size (165 bytes) and had no activity for at least 30 days. To ensure objectivity, we performed random sampling and repeated validation ten times. The results converged to an abandoned rate of about 8% to 10% in which the token balance remained at zero.

Of course, not all 607 million unclosed accounts are immediately zombie ATAs. However, given that many meme coin trading accounts have extremely short lifecycles, effectively "create, trade briefly, abandon," it is highly likely that many currently active accounts will rapidly converge toward the sampled characteristics over time. Under this logical assumption, applying the estimated ratio to the full population implies that roughly 54 million accounts are in a zombie state.

Converted using the standard SPL rent deposit (0.00204 SOL), this implies that at least 110,000 SOL is locked up. Importantly, this figure is a conservative lower bound. The estimate only considers accounts with a completely zero balance. In practice, a key target for rent recovery also includes "worthless balance" accounts, meaning accounts that still hold tokens but whose market value has effectively disappeared. Given the surge in abandoned, value less tokens after the meme coin wave, the real market size is likely to exceed 110,000 SOL. This supports the idea that Solana's growth has created a large pool of idle capital and that rent recovery services have a meaningful addressable market.

This estimate is a simulation intended to understand the market's potential total addressable market (TAM). The realistically monetizable size may be adjusted by external variables such as whether bot operators self recover, user friction during burn and closure flows, and future rent policy changes by the Solana Foundation.

Rent recovery is possible by invoking the CloseAccount instruction. CloseAccount permanently closes an account that is no longer needed and refunds the rent exempt deposit to a designated wallet. This mechanism can be used not only to clean up zero balance ATAs, but also to close many other types of accounts: NFT metadata accounts, OpenBook market related accounts that remain idle due to unfilled orders, empty staking accounts, domain accounts, and more. As noted earlier, rent is priced proportional to the account's data footprint, so closing complex, large on chain accounts such as OpenBook market accounts can sometimes return much larger amounts than closing standard ATAs.

The issue is that most everyday users do not understand the rent model or how to recover it. Many users do not even realize that small amounts of SOL were deducted as rent during transactions. If they sell all of a token and their wallet balance for that token becomes zero, it is natural to assume the account has effectively ended its life. As a result, users often remain unaware that part of their assets is still sitting on the network as a deposit. Unless CloseAccount is executed, that value is effectively stranded indefinitely.

Paradoxically, this lack of awareness and the friction in manual recovery became a business opportunity for new services within the Solana ecosystem.

One common pattern for DApp success within a protocol is the emergence of applications that remove painful UX. Solana's rent model created exactly this kind of opportunity. Users can recover their deposited SOL by closing accounts, but many were unaware of the rent concept in the first place, and even those who knew often found the claiming process inconvenient.

Source: Sol Incinerator

The Sol Slug team launched Sol Incinerator in 2021, enabling users to recover locked up SOL deposits by simply connecting a wallet and cleaning up unnecessary accounts. The app offers two main functions depending on whether the target token account has a remaining balance.

Zombie ATA cleanup: It identifies zombie ATAs that remain active even though their utility is gone and their balance is zero. By closing these accounts and freeing storage, it executes immediate rent recovery.

Malicious asset burn and account cleanup: It handles spam tokens or rug pull NFTs that still have a balance but no market value. It permanently burns these assets to reduce the balance to zero, then closes the ATA in a single flow to recover rent.

There is at least one case where a user suffered losses after accidentally burning 10 million PUMP tokens worth roughly $75,000 while performing malicious asset burning and ATA cleanup. Always double check tokens before burning.

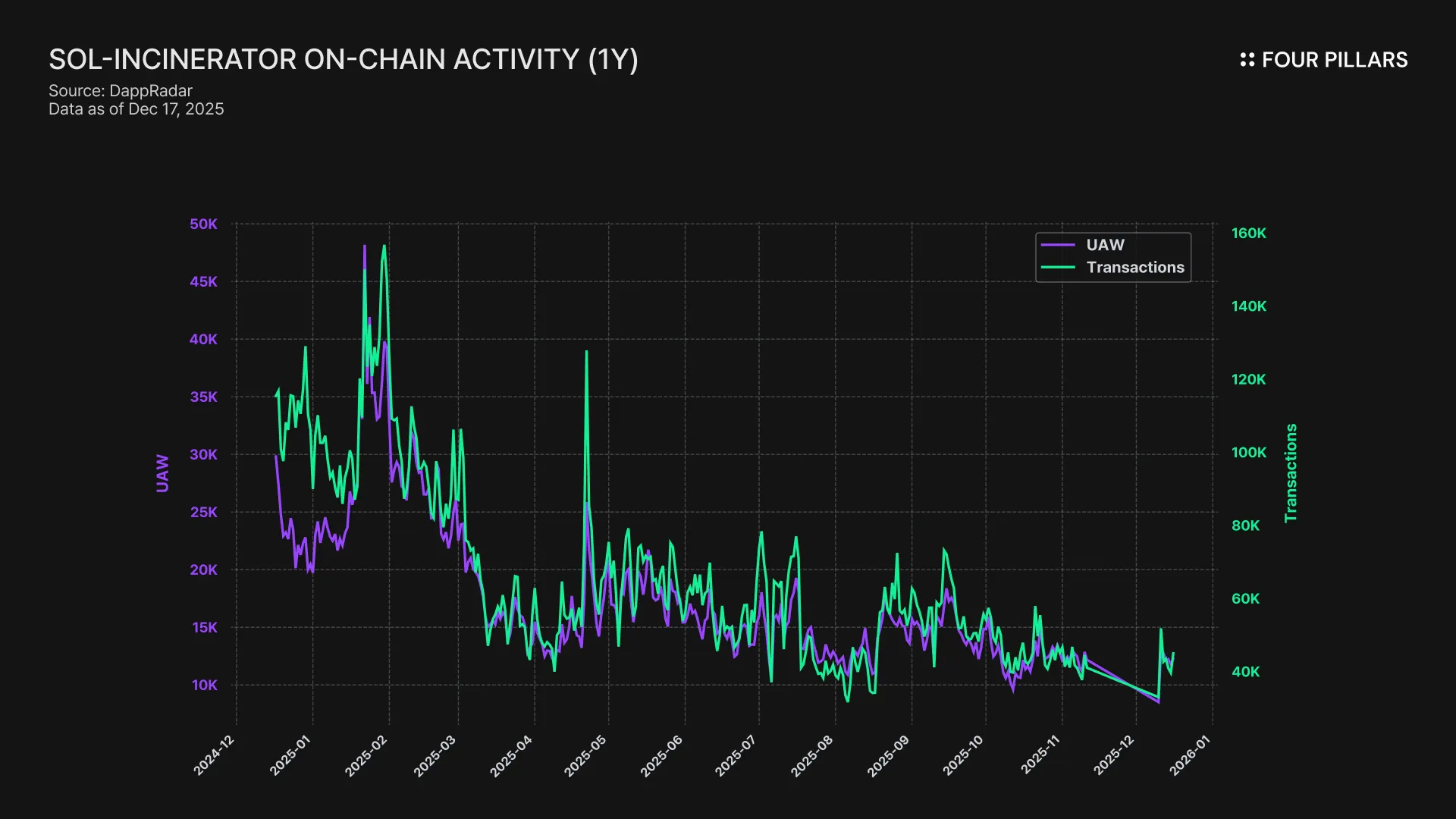

Sol Incinerator gained attention amid explosive on chain activity in the Solana ecosystem, from the 2021 NFT boom to the 2024 and 2025 meme coin frenzy. As a natural byproduct, large volumes of zombie ATAs and accounts with ambiguous residual balances accumulated, creating a clear need for cleanup. At that moment, Sol Incinerator was not merely a cleaning tool. It served as the first catalyst that helped users recognize the hidden balance, rent locked inside their wallets. The feeling of getting your own money back, rather than "making money," is a much stronger behavioral trigger. This market did not grow because demand always existed, but because invisible demand became visible.

Looking at data from late 2024, three years after launch, Sol Incinerator's daily active wallets (UAW) reached around 48,000 as meme coin activity drove a surge in demand for cleaning up accounts left behind after full liquidation. As the frenzy cooled, the metric declined, but it remains notable that more than 10,000 unique wallet addresses still use the app daily, maintaining meaningful transaction volume. Rent recovery has become not a seasonal fad, but a routine for asset management among Solana users, while also taking on a public good character by reducing unnecessary accounts and cleaning network state. Individuals recover small amounts, the ecosystem reduces state bloat, and the service earns fees. This structure translated directly into dramatic performance in the data.

Key milestones Sol Incinerator reached by November 2025 include:

Cumulative SOL returned: 472,384.98 SOL

Wallets that generated transactions: 3 million

Monthly active users (MAU): 500,000 wallets

Return and reuse rate: 80%

Cumulative transactions: more than 49 million

Sol Incinerator has effectively captured the rent recovery market. Applying its fee rate (about 2.3% to 5.0%) to the cumulative returned amount suggests estimated revenue of roughly 10,000 to 24,000 SOL. This implies that even with a simple feature set, combining clear user perceived value with a strong reason to return can produce a meaningful revenue model. The near 80% reuse rate is particularly notable. Given the industry reality that 90% of DApps see users churn within the first week and average one month retention is under 10%, this indicates the app has built a durable user base.

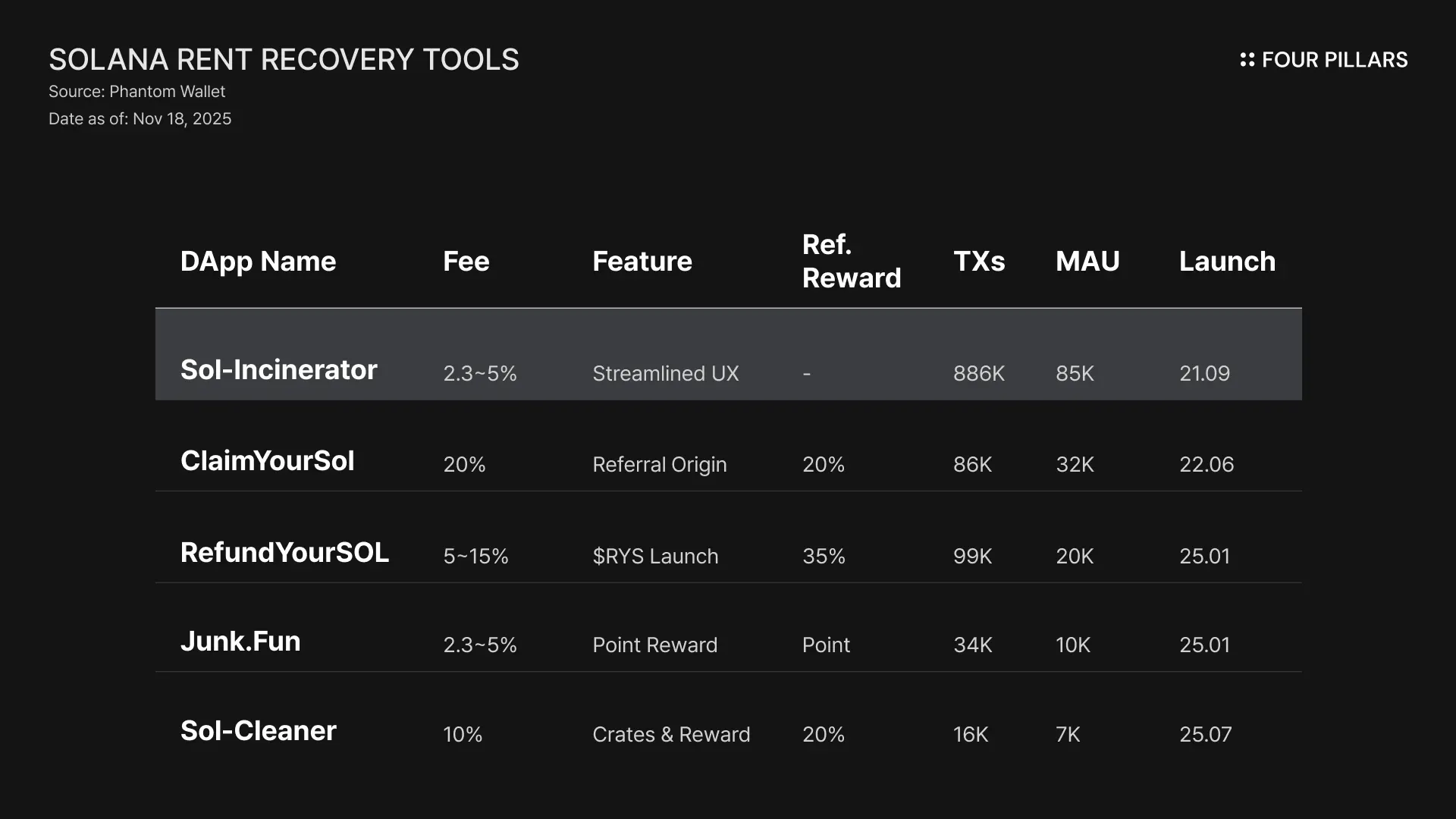

The rent recovery logic itself does not have a high technical barrier to entry. As a result, DApps offering similar functions quickly appeared after the leader. But as more competitors entered, latecomers realized they could not win with feature replication alone, so they adopted common Web3 mechanisms such as referrals, token economics, and gamification.

Below are a few rent recovery DApps that introduced particularly notable mechanisms.

3.2.1. Differentiation Tactics of Late DApps: Referrals, Tokens, and Even Gamification

ClaimYourSol is a case that aggressively introduced a referral system into the rent recovery market. It charges higher fees than competing services, then redistributes a meaningful portion of those fees as referral rewards to strengthen promotion incentives for key opinion leaders (KOLs) and community leaders. For users, fee resistance is lower because the emotional payoff is "recovering forgotten money." For influencers, referral income fuels organic distribution. In other words, fees become the marketing budget.

RefundYourSOL went a step further by issuing its own token and attempting to combine DeFi elements. After launching a native token called RYS, it proposed an expansion from a one time utility into a sustainable investment like platform by offering fee discounts to token holders and revenue sharing to staking participants.

Services such as Junk.Fun and Sol Cleaner added points, rewards, and gamification on top of referrals, aiming to make users visit more frequently by showing additional incentives beyond rent recovery.

3.2.2. The Market's Essence: People Want Simplicity and Familiarity

Did these feature rich latecomers actually take over the rent recovery market? Over the most recent one month period from November 18, 2025 to December 18, 2025, Sol Incinerator recorded at least 10 times the transaction count and at least 2.5 times the monthly active users compared with its peer set, demonstrating overwhelming market leadership. Why?

If fees were the only driver, it would be hard to rationally explain why Junk.Fun, which charges similar fees but adds referrals and gamification, holds a lower share than Sol Incinerator. The distribution makes sense once you consider the essence of this market.

Rent recovery is a task where decision complexity, and an abundance of options, make users more uncomfortable. What users want is not extra rewards, but fast, safe recovery. Referrals, token utility, and rewards may help acquisition, but they do not inherently deliver the functional depth users actually need, and can even detract from it. A clean UI and a highly intuitive, recovery first workflow can deliver more depth than a bundle of extras. In that sense, Sol Incinerator provides stronger functional depth than many later DApps.

In addition, the temporal depth accumulated since 2021 is a powerful barrier to entry. Rent recovery is not an exploratory domain for discovering new value, but an execution domain for cleaning up residual assets. Users prefer to avoid the risk of validating a new service and instead choose a tool that is already widely proven and familiar. The fact that Sol Incinerator's reuse rate approaches 80% shows how large a moat trust and familiarity can be in this market. Once inertia sets in, latecomers cannot easily redirect that orbit just by adding a few more features.

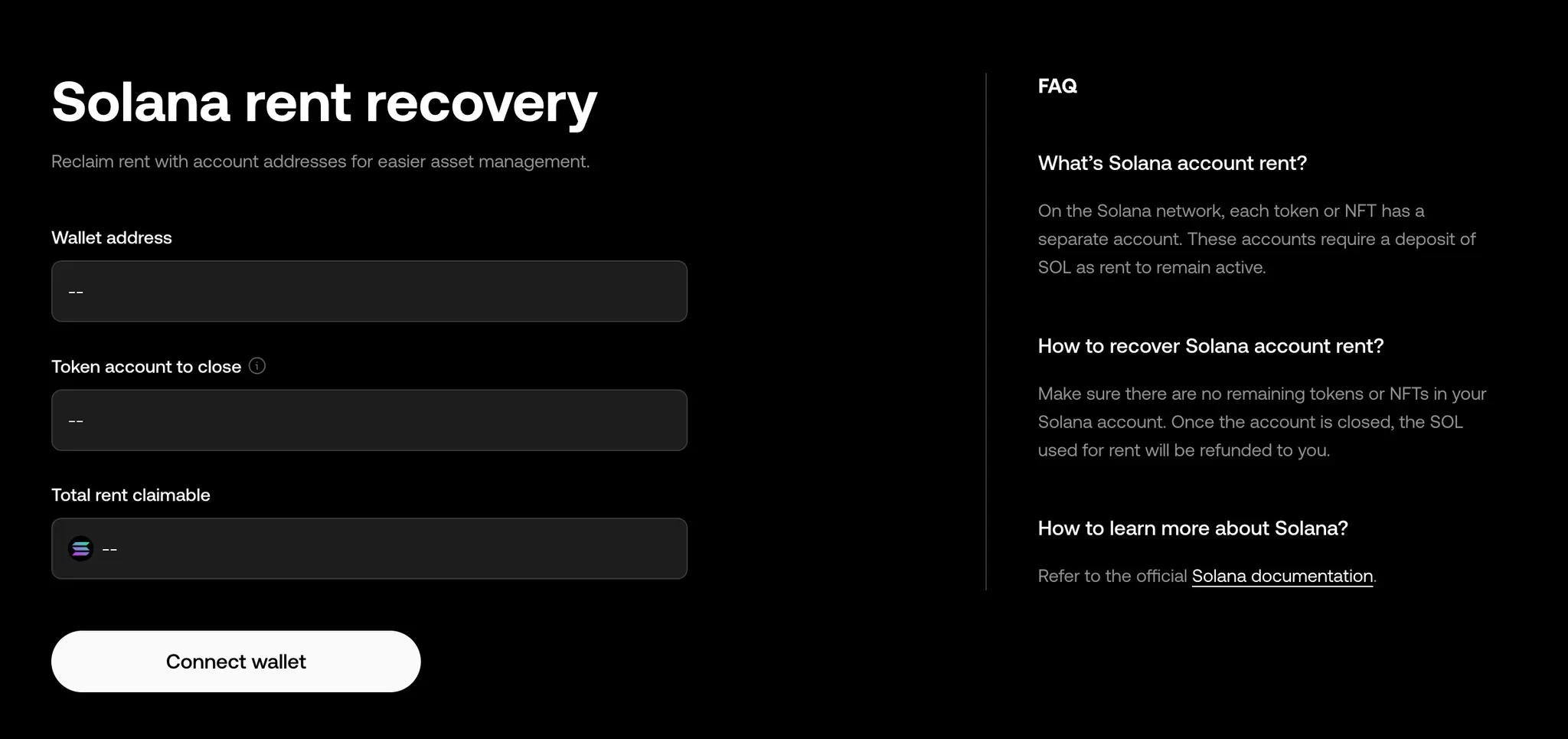

Wallets naturally moved into the rent recovery market as well. Wallets are the starting point for transactions and they control signatures and distribution. Some wallets embedded rent recovery as a default feature, aiming to create a flow where users can clean up accounts inside the wallet without connecting to an external DApp. OKX Wallet and Solflare are representative cases.

Source: OKX Wallet

Source: Solflare Wallet

An interesting detail is that these wallets effectively charge no fees for the feature. At first glance, this may look like "giving up revenue to improve user benefits," but from a wallet's perspective it is not necessarily uneconomic. A wallet's revenue does not come from one feature alone. If users spend more time in the wallet and transact more often, revenue can be generated elsewhere through swaps, on ramps, bridges, and other touchpoints. In that sense, rent recovery can be seen as a retention and trust mechanism rather than a directly monetized product.

So why did wallets fail to overturn a DApp led market structure despite the clear price advantage of zero fees? The answer lies in the paradox created by the wallet's biggest strength, workflow simplification. For the sake of generality, wallets sacrifice functional depth, and in a domain where detail matters, this becomes a structural limit they cannot overcome.

First, wallets are constrained by a standardized UX. Wallets are closer to financial infrastructure serving a broad audience, so their UI tends to be standardized and it is difficult to aggressively expose advanced options or extensive exception handling. In the cases described above, OKX Wallet often looks less like a fully in wallet flow and more like a handoff to an external site for account cleanup. Solflare focuses primarily on cleaning up zombie ATAs with a zero balance, which limits its ability to provide a full workflow that includes burning spam tokens, meaning assets that still have a residual balance. By contrast, a DApp can optimize the entire interface for the single job of account cleanup, pushing detail as a core advantage through filtering, batch processing, visualization, result summaries, and more.

Second, wallets must minimize risk. A wallet is the starting point for all of a user's on chain activity, so any incident immediately translates into wallet brand risk. Rent recovery does not necessarily end at closing accounts. It can expand into flows that burn worthless tokens and then close accounts. Burning is risky for users who do not understand the concept precisely. As the accidental burn case above illustrates, deeply embedding this feature increases the chance of novice misuse and expands questions of responsibility. Wallets are structurally forced into a conservative posture, which makes it difficult to expand beyond a basic feature set into the deep workflows DApps can offer. That is the functional depth boundary that wallets cannot realistically cross.

The rent recovery market has grown alongside the expansion of the Solana ecosystem, but this growth cannot last forever. Instead, the market is now approaching a structural inflection point that could push it toward contraction.

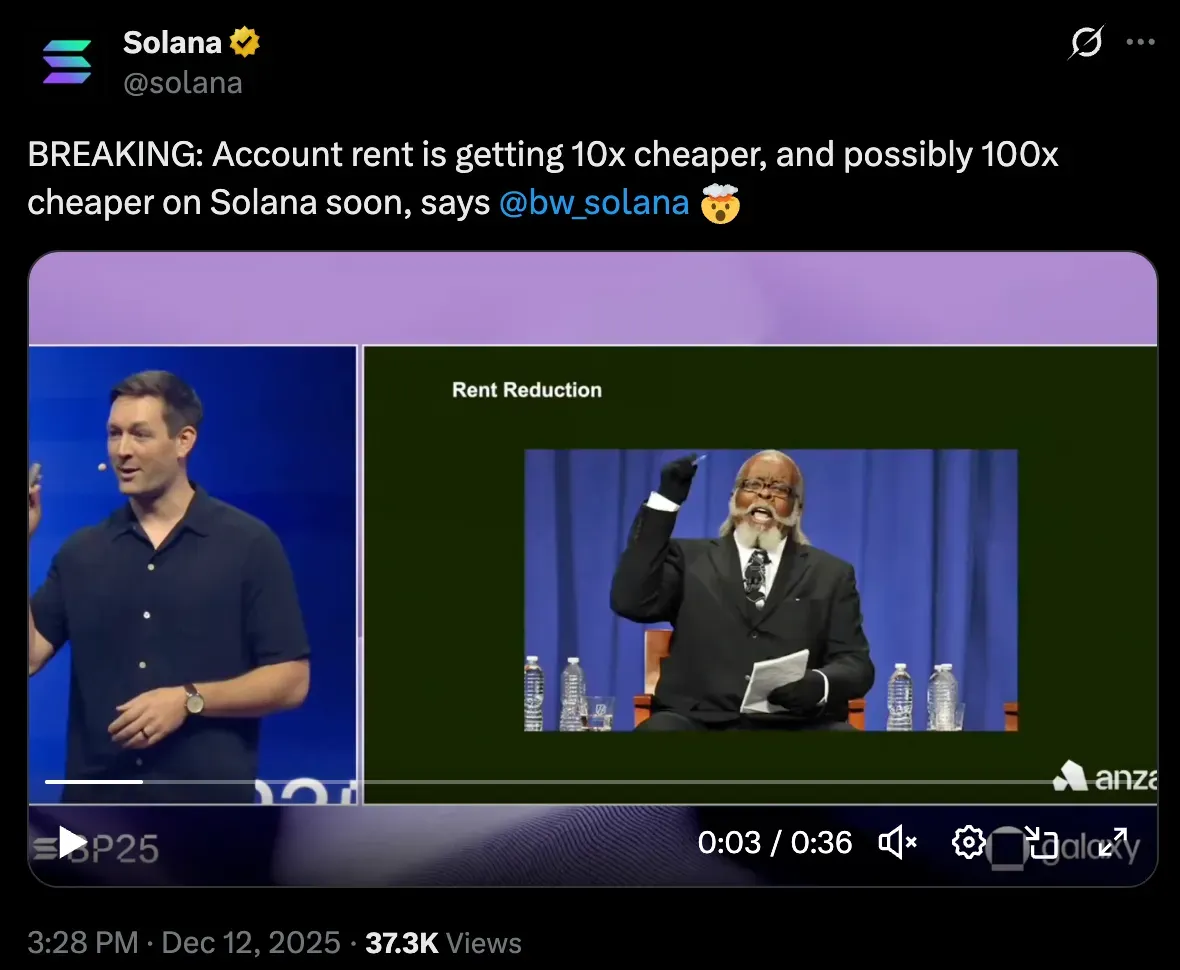

Source: X(@solana)

At Solana Breakpoint 2025, held on December 12, 2025, Solana development company Anza argued that "The rent is too damn high," and announced a major plan to cut on chain storage costs. The roadmap aims to let projects build large accounts without heavy burden by reducing rent to one tenth of the current level, and potentially as low as one hundredth.

This is clearly positive for ecosystem builders, but for the rent recovery market it opens two opposing scenarios. On one hand, reducing the rent recovered per account could shrink the total recoverable pie. On the other hand, if lower rent triggers a flywheel effect that encourages explosive account creation, especially when combined with trends such as meme coins, the sheer increase in quantity could offset the lower unit economics, maintaining or even expanding the total value stranded. In short, both contraction via lower unit values and expansion via higher volumes remain plausible.

Regardless of how the market size changes, this battle demonstrates a structural reality: wallets that aim for generality will struggle to outpace DApps across every domain in value capture. Consider rent recovery again.

Wallets benefit from broad distribution as the first point of contact for users. But in markets that demand specialization, that breadth can become a shackle that limits depth. As mainstream infrastructure, wallets must standardize UX conservatively to minimize risk, and they are forced to exclude sharp, potentially dangerous features that could put user assets at risk. This is why wallet based rent recovery tends to stop at basic zombie ATA cleanup.

By contrast, the functional depth a DApp can deliver is free from those constraints. This is not about piling on features, but about optimization that penetrates the essence of the user's problem in a specific market. In rent recovery terms, users want more than simply closing accounts. They want to visualize wallet state, filter risky assets, and clean everything up with one click.

If the wallet's "safe standard" is to calmly say, "You have 0.002 SOL available," the DApp positions itself as the fixer who says, "We can burn 50 spam tokens in one second and recover 0.1 SOL for you." It is not that the wallet cannot do it. It is that these sharp details are hard to prioritize when you must cover everything. Those details are exactly where DApps can win, and where they can capture value.

The rise of Fat Wallets does not eliminate the space for DApps. It is inevitable that wallets will expand by absorbing repetitive, universal functions such as swaps and transfers. But the idea that wallets will become super apps that monopolize every user experience does not hold across all markets, because each market demands a different level and type of depth.

For this reason, the future value capture battle can be summarized as coexistence and conflict between wallet accessibility and DApp specialization. The strategy for survival is clear: avoid the battlefield of accessibility, where wallets already have the advantage, and instead go deeper into domains wallets cannot reach due to efficiency tradeoffs and structural constraints. Even if shallow markets where accessibility matters most are ceded to wallets, markets that require advanced specialization will remain DApp territory.

In other words, the narrative of DApp decline applies only to generic services that fail to differentiate. Paradoxically, this also means that for undifferentiated DApps, competition against wallets that already dominate accessibility does not even begin.

Wallets control the entrance to Web3. But the destination users ultimately want to reach is the specialized DApp that solves their problems completely. No matter how large wallets become, the value of a DApp with a sharp, essential purpose will not be diluted. That sharpness is where the future of DApps lives.

Dive into 'Narratives' that will be important in the next year