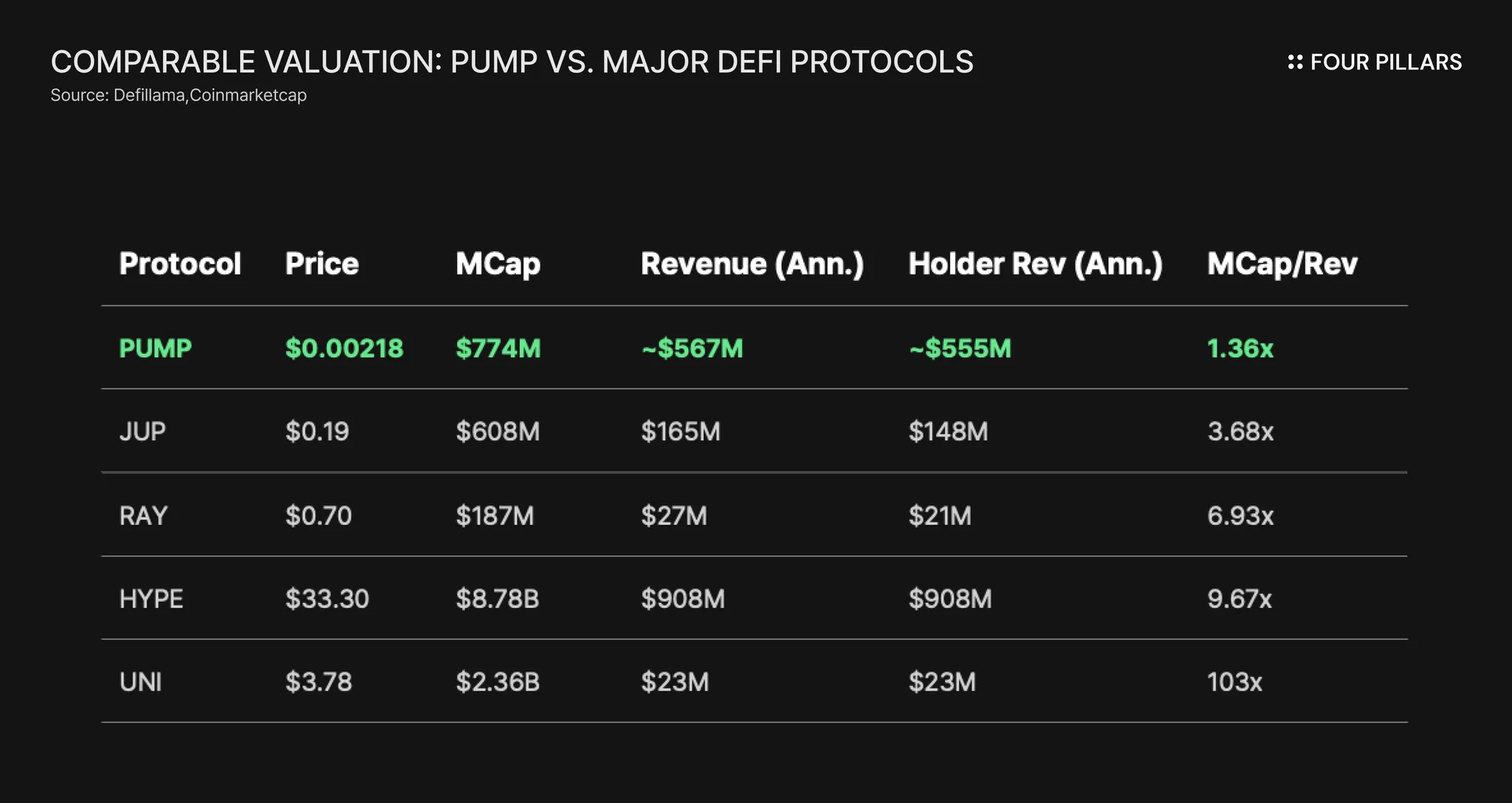

pump.fun generates $567M in annualized revenue at a 1.36x P/E — on a platform doing $1.29B in fees, more than every DeFi protocol except Hyperliquid. Hyperliquid trades at 9.67x, Uniswap at 103x.

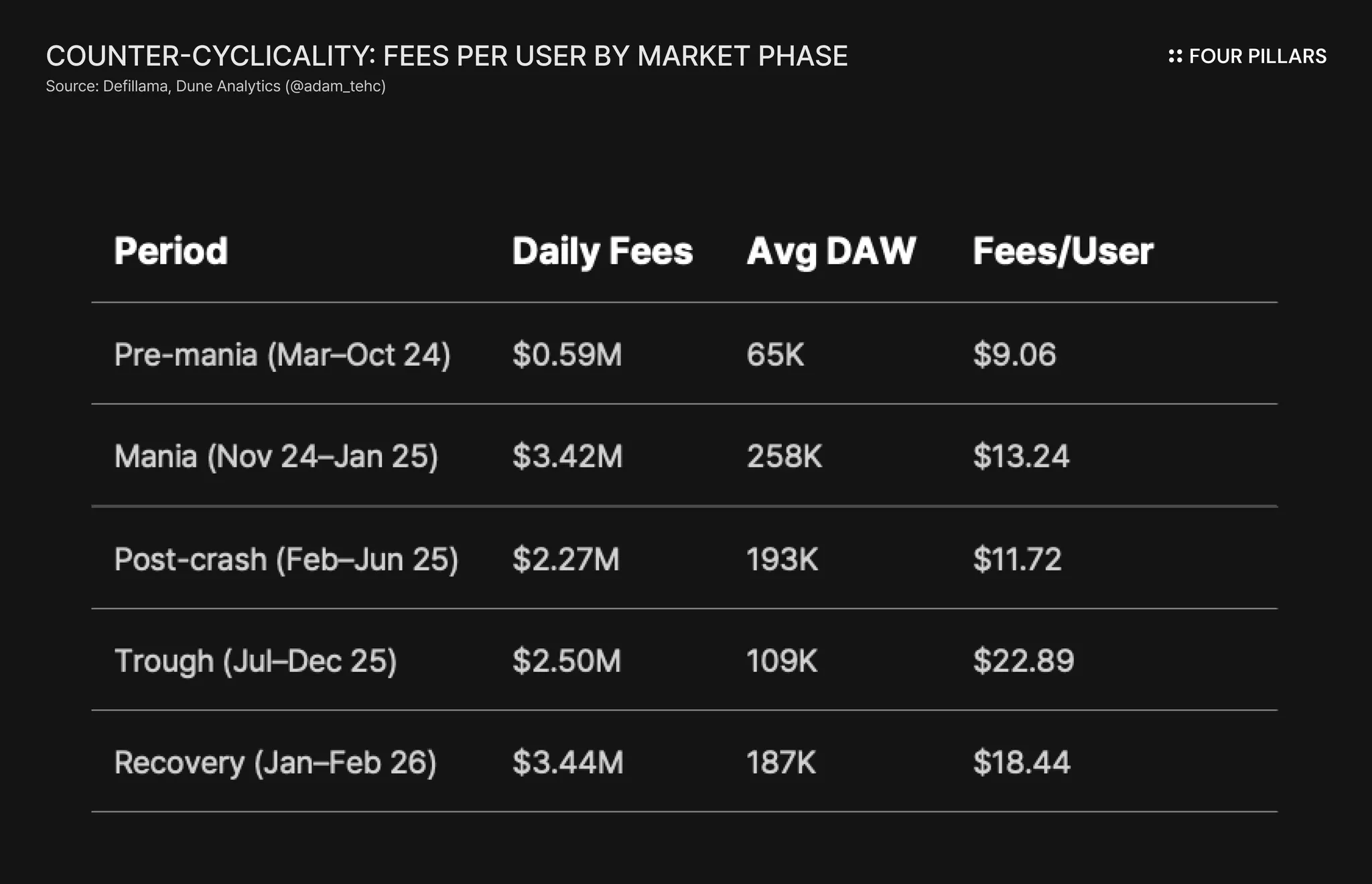

When users halved during the 2025 trough, fees per user doubled. Thirteen consecutive months above $1M/day through the worst macro since 2022, $1.52B in ICO dilution, and active litigation. That's addiction infrastructure, not tourism.

Buybacks absorb ~2x all new token supply at current prices, and that ratio improves when team unlocks begin in August — Phase 2 emissions (~9.2B PUMP/month) are actually lower than Phase 1 (~10B).

The downside requires revenue to fall below where it's ever been. The upside only requires the multiple to normalize. At a garbage-tier 4x on current revenue, FDV is $2.2B, a 3x from here.

Every cyclical business has its off-season. The tourists leave, revenue dips, the town looks half-dead, but the regulars keep playing, spending more per hand without the crowds, and the house still takes its cut. Every month, without fail.

The smart money doesn't wait for summer. It buys during the off-season, when the price reflects winter and the business keeps printing. pump.fun just came through its worst off-season imaginable (disgusting macro, $1.52B in ICO supply hitting the market, active RICO litigation, memecoin sentiment at bottom with no runners clearing $1B since last cycle's AI szn) yet revenue never broke below $1M/day in fees. Trough average: $2.50M/day, with everything working against it.

DEX volume just hit all-time highs (weekly and daily), higher than the January 2025 mania, higher than the September 2025 spike. Users doubled off the trough and are still climbing, fees are back above $3.4M/day, and the off-season is over. Yet the price looks like it's going to die any moment.

That doesn't automatically mean cheap, and I'm not going to pretend the discount is irrational; real reasons exist, and I'll walk through every one honestly. But the gap deserves some work.

Bear case first.

This is the deepest critique, and it's the one I can't fully dismiss. Hyperliquid scales into new asset classes multiplicatively (crypto perps today, equity perps through HIP-3, commodities and prediction markets through HIP-4) and each addition expands the ceiling. Global derivatives are hundreds of trillions, and the ceiling keeps rising every time a new asset class plugs in.

pump.fun's next asset class is…more memecoins? There's no HIP-3 equivalent and no mechanism that opens an adjacent market, which means growth requires either more gamblers showing up or existing gamblers gambling harder, both of which work during bulls and pull back during bears, exactly the way you'd expect a cyclical business with a bounded TAM to behave. Casino revenue is a function of gamblers times appetite, while exchange revenue is a function of global financial activity, which is effectively unbounded.

PUMP is a casino and HYPE is an exchange. Both are profitable, but only one compounds.

Governance is a checkbox that doesn't move cash flows, and nobody is buying PUMP to vote on proposals. EVM expansion sounds ambitious, but the moat is Solana-native — the brand doesn't transfer cross-chain, the bonding curve is trivially forkable, and competing on Base or Ethereum means fighting incumbents on their own turf while fragmenting team attention away from the business that's actually generating all the revenue.

Pump Fund and the hackathon are $3M in marketing dressed as ecosystem building, and I'd note that $WIF and all the previous $1b runners didn't need a hackathon to become the biggest memecoin of its cycle.

No second act is being built, and the roadmap reads like the standard crypto playbook where projects announce things that sound good on CT without changing unit economics.

ATH volume should mean ATH revenue, and the fact that it doesn't tells you exactly how much the fee restructuring is already biting.

Old structure was ~1% flat fee, protocol keeps almost everything, nearly all flows to buybacks. The new structure is more complex, with dynamic fees ranging from 0.05% to 0.95% via Project Ascend with revenue redirected toward creators, and PumpSwap taking 0.25% on post-graduation trades split 0.20% to LPs and only 0.05% to protocol.

Each change is individually defensible because you need to retain creators and fight off competitors, but collectively they're corrosive to the buyback thesis because every dollar redirected is a dollar that doesn't flow to PUMP holders.

And the proof is already in the numbers. DEX volume hit all-time highs in late January and early February ($6.27B weekly for Jan 19–25, $1.36B daily on Feb 3) higher than both the January 2025 mania and the September 2025 spike. ATH volume should mean ATH revenue, and the fact that it doesn't tells you exactly how much the restructuring is already biting (e.g: Feb 3 snapshot - $1.36B in volume produces $3.47M in fees but only $1.55M in protocol revenue).

The team is choosing platform growth over token value accrual, which is rational for the business and explicitly corrosive for holders.

Legal: Aguilar v. Baton Corp is a RICO plus securities class action with motions to dismiss filed January 23. Jito already got dropped, defense filed motions to dismiss in January arguing "non-actionable puffery," and recent precedent in Ripple and Coinbase hasn't been kind to these claims. The wildcard is 15,000 leaked internal chat messages — if those show real coordination between Solana Labs and pump.fun, the calculus changes. But the market has barely flinched at any legal development in twelve months, and honestly neither have I.

Founders: Pseudonymous team led by Alon with Dylan's 2017 rugpull history, and buybacks are entirely discretionary rather than protocol-enforced. The team holds hundreds of millions of dollars in PUMP so stopping buybacks would destroy their own wealth, but that's greed alignment rather than contractual obligation. I'm trusting The Block Co-founder and 6th Man Ventures GP Mike Dudas's seed-stage diligence and Alliance DAO's vetting on this one.

Macro: Needless to say crypto is in deep shit right now.

Everything in this section is real. These problems justify a discount.

pump.fun holds 89.9% market share in memecoin issuance on Solana, and that monopoly has already been stress-tested — LetsBonk breached share briefly and pump recaptured it without subsidies or incentive campaigns. "Launch on pump" is a verb now. The platform doesn't care which tokens win or lose, it just needs people to keep launching them.

What surprised me most when I dug into the numbers is how the revenue behaves when users leave:

Users halved during the trough and fees per user doubled. Tourists left and degens intensified, spending more per hand without the crowds the way a casino floor works when the conventions go home. Thirteen out of thirteen months above $1M/day, through the worst macro since 2022, through $1.52B in ICO dilution, through active litigation.

Then January hit: users flooded back (+95% MoM) but per-user spend stayed elevated at $18.44 instead of dropping back to the mania-era $13.24. Both engines running simultaneously now, which is the combination that produced every prior fee peak.

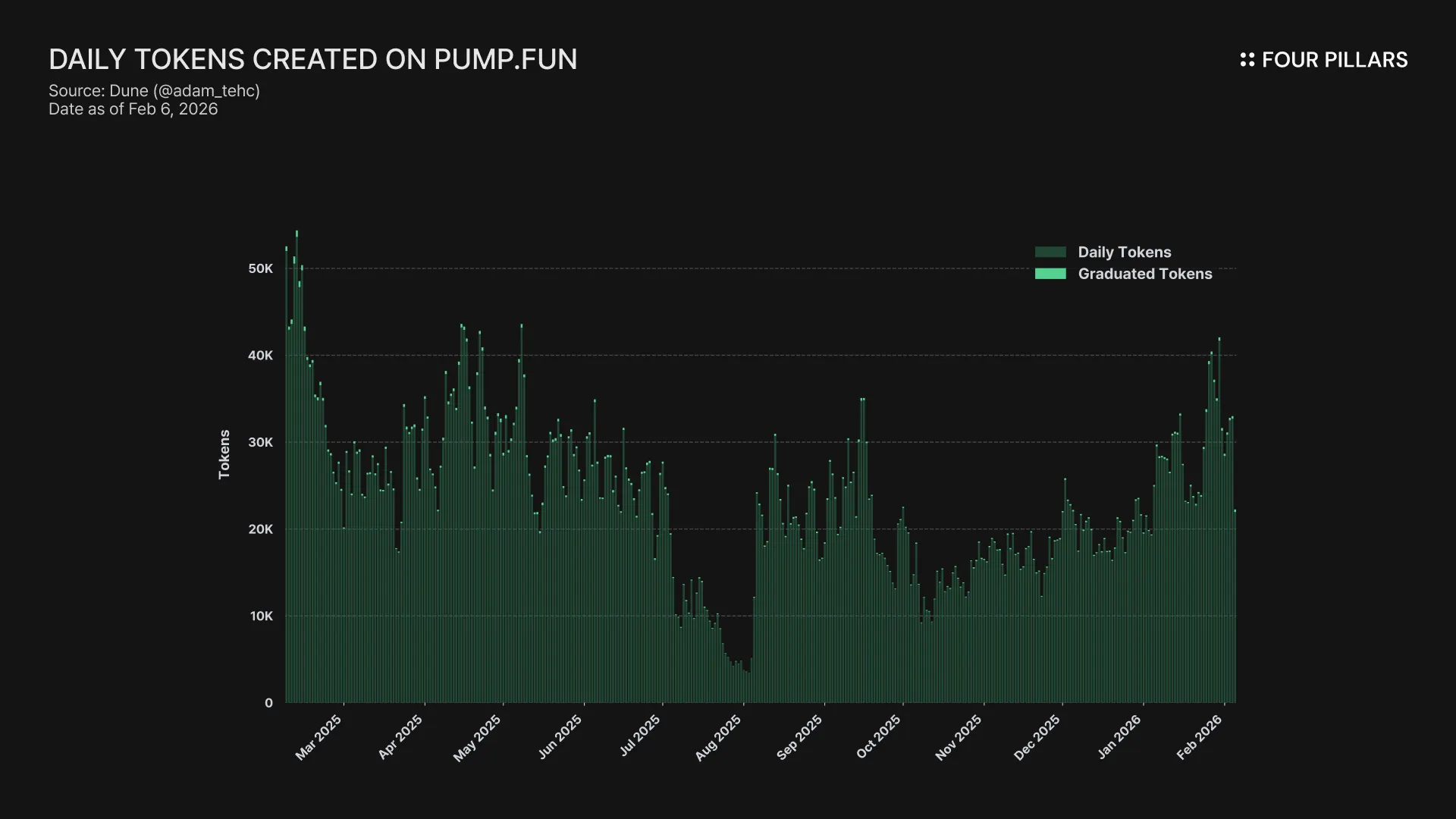

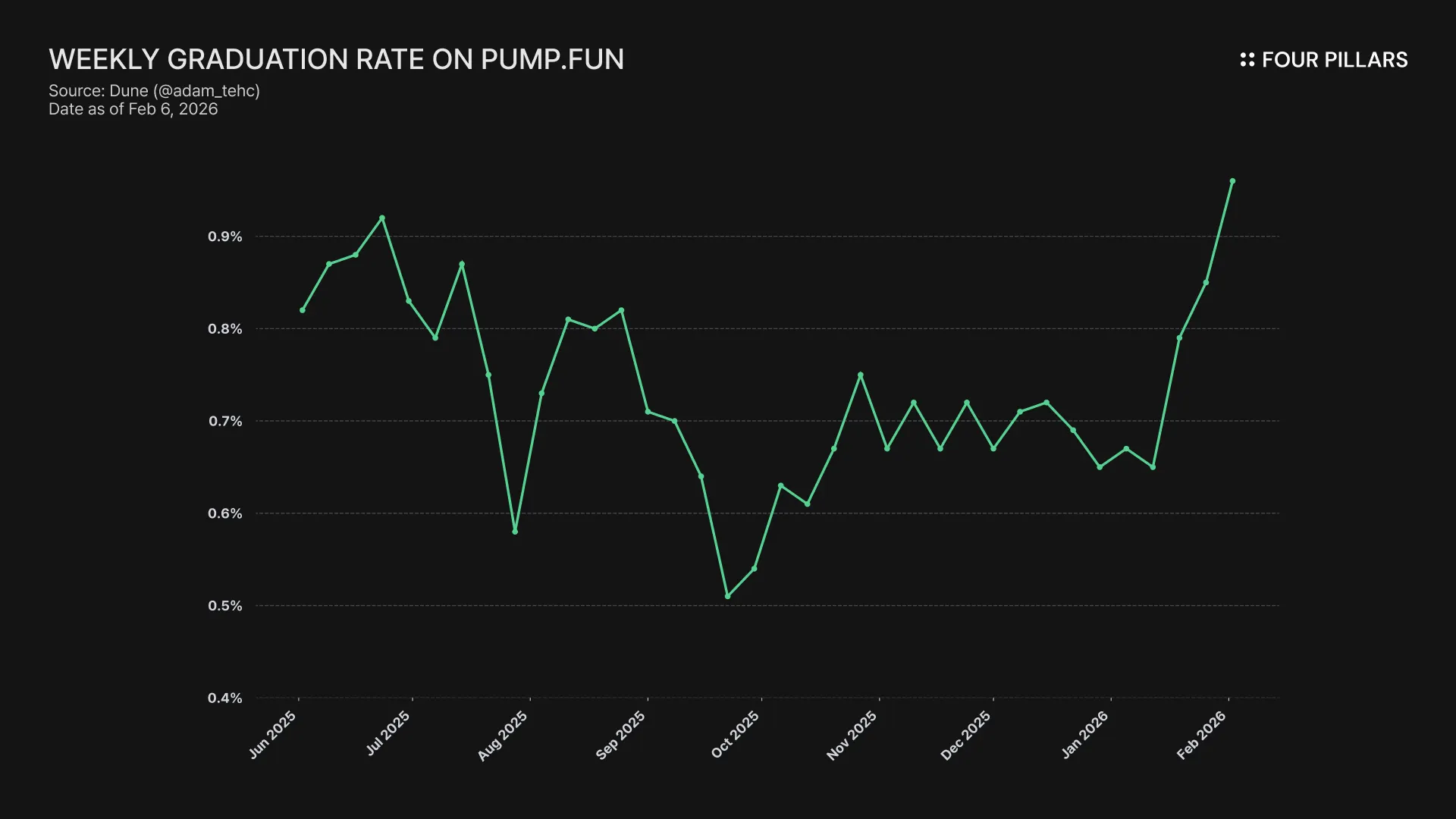

The token factory tells the same story from a different angle. 8.6 million tokens created, 71,000 graduated, and the graduation rate is worth lingering on. It bottomed at 0.51% in October 2025 before climbing to 1.06% ATH, a move that started four to six weeks before the January revenue surge.

That timing isn't coincidental: graduation rate is a leading indicator. When more tokens survive the bonding curve, it means the quality of speculative demand is improving: traders are picking better, or more capital is flowing per token, or both. The factory starts producing more viable tokens before the fees show up in the aggregate numbers. Right now, the graduation rate is still climbing, which suggests the revenue recovery has more room to run.

On the retention side, January recurring users averaged 96,979 per day, which actually exceeded December's total average DAW of 96,274. The recurring base is expanding faster than churn, and late-January spike days hit 297–300K approaching mania levels.

Coal miners with terminal demand trade at 4–5x earnings. Mature casino operators with zero growth get 7–10x. Tobacco companies with a literally dying customer base: 8–9x. These are businesses where the TAM is shrinking, regulation is tightening, and the entire investment case is "it throws off cash while it declines." pump.fun trades at 1.36x with revenue that just proved it survives the worst conditions thrown at it. Even if you think memecoins are terminal (and I don't) the multiple is wrong.

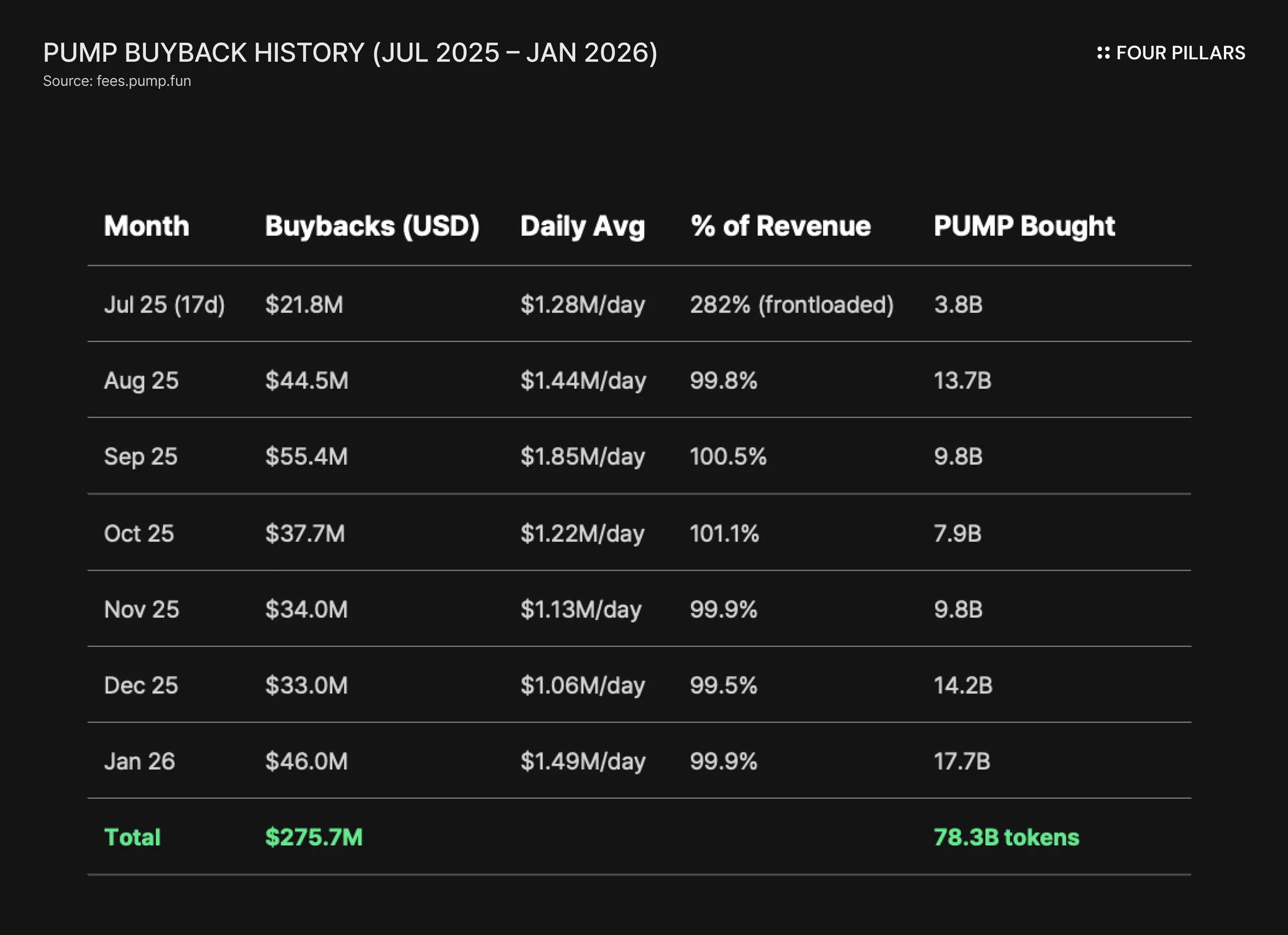

Since July 15, 2025, roughly 100% of protocol revenue has gone to open-market PUMP buybacks, verifiable daily on fees.pump.fun:

Every single month at 100% allocation, verified on-chain. And the buybacks accelerate as price drops. January removed nearly 2x the tokens September did for less money, which means float compression intensifies exactly when the business looks weakest.

I want to be clear about what buybacks are and aren't. They're not a catalyst; price is where it is with $46M/month already flowing in. Instead, they're a consistent bid pressure that compresses float while you wait for the things that reprice the token.

390B tokens remain locked, and they come in two sequential phases that don't overlap. Phase 1 runs from now through July 13 (Community & Ecosystem only), roughly 10B tokens per month, and at current revenue and price buybacks absorb about 197% of that new supply.

Then there's a one-month gap from July 13 to August 12 where community is fully vested, nothing new is unlocking, and buybacks run unopposed.

Phase 2 starts August 13 with Team (~5.6B/month) and Investors (~3.6B/month) beginning linear vesting, totaling roughly 9.2B tokens per month, actually less than Phase 1. Buybacks absorb about 215% of Phase 2 supply at current price, and even at the $0.0045 base case target absorption holds above 100% (see section 3).

Memecoins are the only asset class where something goes from $0 to $100M in less than a month, and that lottery-ticket impulse survived 2018, survived 2022, survived 2025, each cycle bringing a new cohort who discover the dopamine hit for the first time. The counter-cyclicality table already proved that the revenue floor holds between cycles while the ceiling expands when they arrive.

This isn't a dying customer base. It's a casino in a tourist town where the tourists change every season but they keep coming. One catalyst worth flagging: thiccy mentioned on threadguy's spaces that every crypto mania requires a new cohort of unsophisticated money discovering the casino for the first time. The AI crowd is sitting right there, filthy rich from lab equity, terminally online, no idea how to spend it, and exactly the kind of people who will discover that launching a memecoin at 3am is the most fun you can have with money. I'm not pricing this in, but I'd rather be positioned before it might materialize than scramble after. When they show up, pump.fun is where they land.

The operating leverage is what makes the setup asymmetric. January 2025 mania hit ~$7.1M/day in fees under the old structure with a ~100% take rate, and the September 2025 spike reached $8.72M/day in fees with $3.57M/day in revenue under post-Ascend rates. Both temporary, both with the platform currently sustaining $3.4M+/day at only 56% of peak users.

If users return toward mania levels on top of today's already-ATH volume base, fees should comfortably exceed the September peak, which at post-Ascend rates translates to $3.5M+ per day in revenue or $1.3B+ annualized on a $774M market cap. The marginal cost of serving those users is near zero, which is why bounded TAM doesn't matter when the leverage between floor and peak is this large relative to the price.

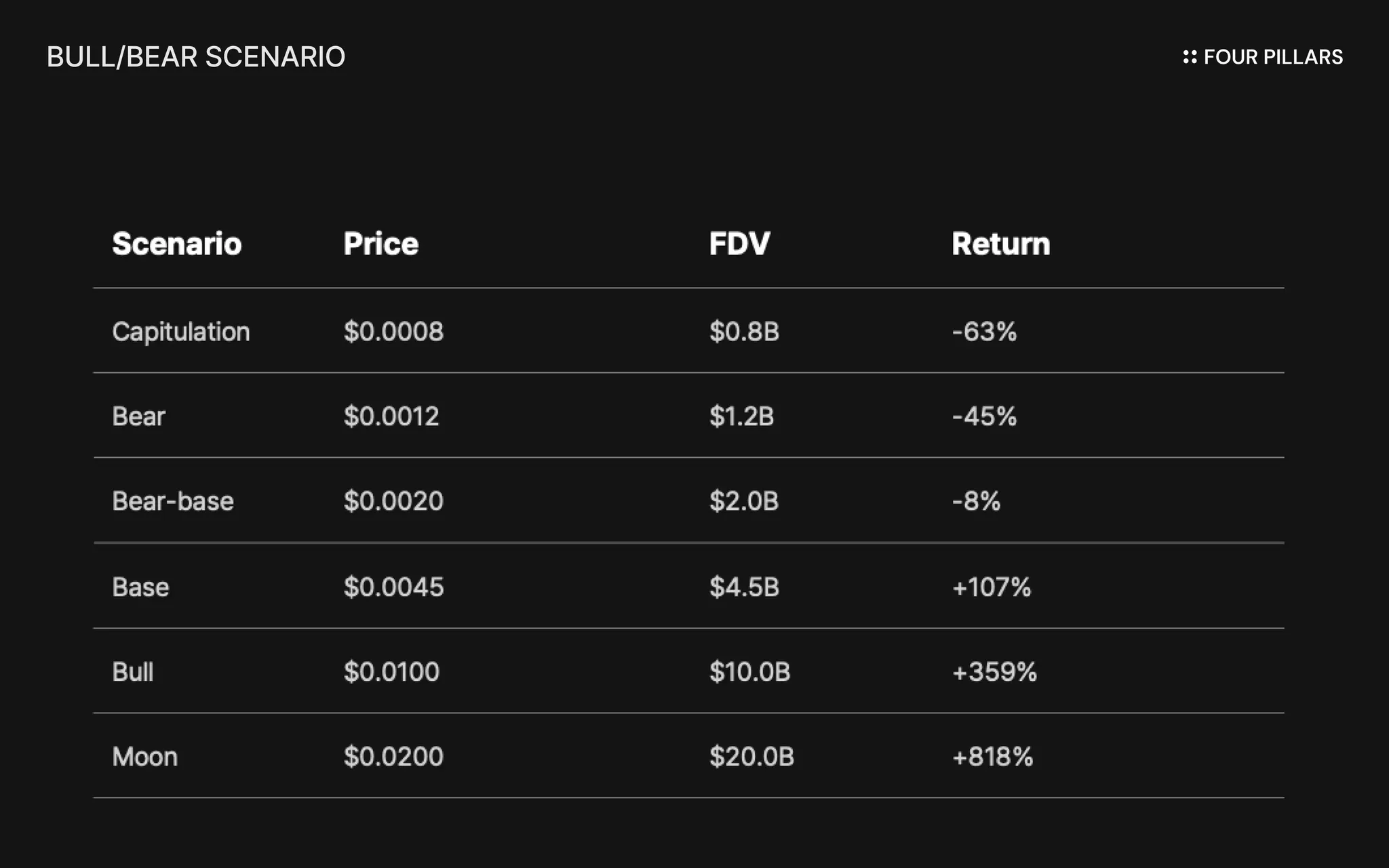

Capitulation at $0.0008 requires securities enforcement forcing a shutdown or delisting, or revenue collapsing below $200K/day (Q1 2024 levels) or the team abandoning buybacks entirely.

Bear at $0.0012 requires the current environment to not just persist but deepen. We're already in what feels like the coldest crypto winter since 2022, and the question is whether it gets materially worse from here or whether this is the trough. If you think there's another leg down that takes fees below $1M/day sustained, this is your price target.

Bear-base at $0.0020 is the nothing-happens scenario where crypto stays in the gutter, no liquidity injection, no narrative, token drifts sideways while buybacks grind. Most likely downside outcome—you bleed slowly, but float keeps compressing and time works for you.

Base at $0.0045 is what happens when crypto macro conditions improve and liquidity starts getting injected back into the market—nothing extraordinary, just the environment shifting from "deep shit" to "cautiously risk-on." Users trend toward 250–300K, revenue stabilizes above $1.5~2M/day, and the market starts pricing PUMP closer to where structurally challenged but cash-flowing businesses actually trade. You don't need mania for this, you just need the macro headwind to stop.

Bull at $0.0100 requires the memecoin cycle to return (users sustaining 300K+, fees pushing $6–10M/day, which has happened twice already) combined with improving macro and legal clarity, though I don't think legal alone moves the price much. $10B FDV on September-level revenue of $1.3B+ annualized is 7.7x earnings, and the business is objectively stronger now than it was in September with supply exhausted, float compressed, and the volume base higher.

Moon at $0.0200 requires full mania — fees exceeding $15M/day, a new user cohort stacking onto the ATH volume base, and macro conditions that let risk assets rip. ~10x on $2B peak earnings. September proved $8.72M/day in fees was achievable, and the next cycle on a compressed float could overshoot 50–70%.

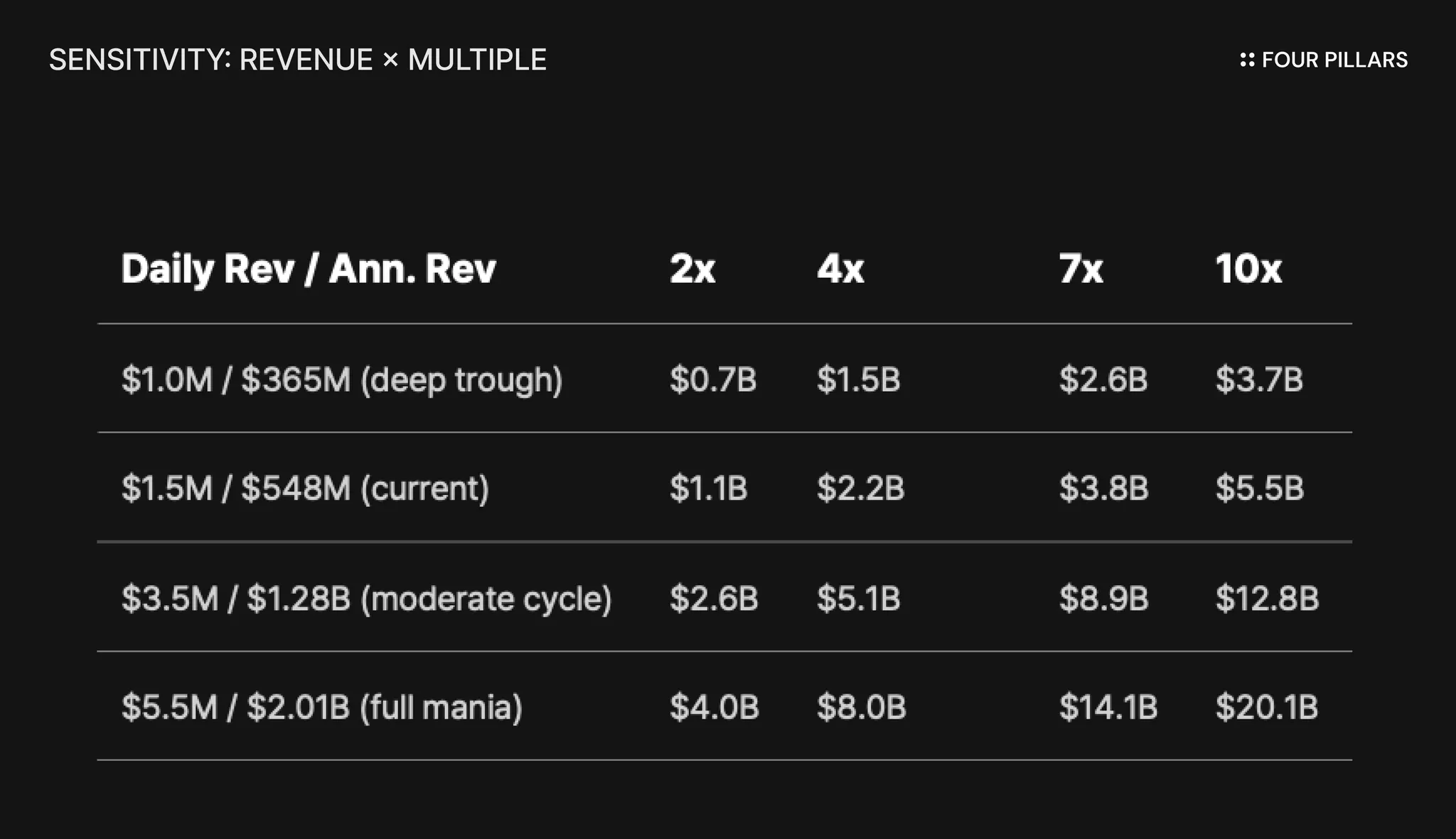

This table lets you pick your own assumptions. Find where you land on revenue and what multiple you think this business deserves, and the market cap falls out:

Two things stand out. Even at a 2x multiple (which is a meaningful re-rating from where PUMP trades right now at 1.37x) the downside from current levels requires revenue to fall below where it's ever been. And at a 4x multiple, current revenue levels imply $2.2B, which is roughly 3x from here. The asymmetry isn't dependent on anyone giving pump.fun a generous valuation but instead dependent on revenue not collapsing below its proven floor while the multiple normalizes even slightly.

Feb 13/20: Legal oppositions and replies due

Q1 2026: First full quarter of dynamic fee data

Jul 13: Community & Ecosystem fully vested, one-month gap before next unlock phase

Aug 13: Team + investor unlocks begin

Q4 2026: Legal resolution window

PUMP is cheap right now because crypto is in deep shit and everything is cheap. That's 80% of it, and I'm not going to pretend otherwise. But what makes this interesting is what you're getting at the current price: a business that never broke below $1M/day in fees through the worst conditions thrown at it, that's currently processing more volume than it ever has, and that's buying back 2x its own dilution every month while nobody's watching.

Do you believe pump.fun's revenue will fall below the worst it's ever done, while daily volume is at all-time highs and users are climbing back toward mania levels? If no, this is a really good spot to start building a position.

I’m long PUMP. NFA.

Dive into 'Narratives' that will be important in the next year