Currently, various L1 projects the market with specialized missions, such as high-performance EVM, optimized rollup execution environments, or IP tokenization, proposing and advocating for new L1 solutions. Among these, which projects can achieve sustainable growth and establish themselves as the next generation of L1 blockchain? This article examines tokenomics, which is as crucial as technical prowess or community in Layer 1 projects.

The key considerations for designing the L1 tokenomics can be based on 1) mechanism design, 2) alignment with architecture, and 3) value capture. According to these, ecosystem participants should prioritize their own interests while their collective economic actions promote network growth. The economic model should be designed to align with the unique technical architecture of the L1, and the token should inherently have a mechanism to gain value as the network becomes more active.

L1 tokenomics that meet these key points include Berachain (PoL), Initia (VIP), and Injective (Burn Auction). These all directly intervene in tokenomics at the network level, adjusting the interests between participating entities or devising new economic models specialized for the technical architecture, and propose unique tokenomics by regulating token supply and demand.

Recent projects garnering significant attention and substantial investments, such as Berachain, Monad, Story Protocol, Initia, and Movement, share a common thread: they are all Layer 1 (L1) blockchains on the verge of launching. These projects opt for their own L1 solutions instead of developing Layer 2 (L2) on Ethereum or creating single protocols. This approach allows them to build unique ecosystems by leveraging specific functionalities and economic models. Each project enters the market with specialized missions, such as high-performance EVM, optimized rollup execution environments, or IP tokenization, proposing and advocating for new L1 solutions.

The question arises: which of these projects will achieve sustainable growth and establish themselves as the next generation of L1 blockchains? A critical factor in this evaluation, on par with technical prowess and community engagement, is the robustness of their tokenomics.

Source: Foundation of Cryptoeconomic Systems

To draw an analogy, a L1 blockchain operates much like a nation. The L1 network serves as the country, with ecosystem protocols forming local economies, and users or communities acting as participating entities. In this framework, tokens function as both economic incentives and the reserve currency, linking various economic units organically.

In this context, what role does tokenomics play in the "nation" of a L1 blockchain? Tokenomics serves as the economic system that incentivizes network participants to engage in activities that ensure active network operations. It also regulates token supply and demand to maintain a stable value.

The design of tokenomics, therefore, mirrors the economic system of a nation. Just as countries design their economic systems considering geographical conditions, industrial structures, political systems, and culture, L1 blockchain tokenomics must reflect the technical architecture, Dapp ecosystem, governance, and community characteristics.

However, many L1 blockchains that emerged during the ICO boom of 2017-2019 adopted cookie-cutter tokenomics without considering their unique network characteristics. This approach has led to the creation of 'Billion-Dollar Zombie Blockchains' that maintain high valuations without significant achievements.

In contrast, recent tokenomics trends show a shift towards more sophisticated approaches. These include direct regulation of token supply and demand at the network level, introduction of tokenomics optimized for technical architecture, and clearer role assignments to align the interests of validators, protocols, and users. This article will examine Berachain, Initia, and Injective as examples of this trend, focusing on three key aspects that address the limitations of existing tokenomics and contribute to sustainable design.

2.1.1 The Role of Layer 1 Tokens

"Why do they need a token?" While tokens are undoubtedly effective tools for blockchain-based projects, this question can be challenging to answer. L1 networks, however, have a clearer justification for tokens, as they are utilized at the core level for validator rewards and network fees. L1 native tokens serve three primary functions:

Reserve Currency: Users pay network fees in native tokens when using block space. In blockchains with embedded L2, the native token is used for storage costs when L2 uses the main chain as a DA (Data Availability) layer.

Incentive Tool: Block rewards for validators who honestly validate transaction legitimacy are provided in native tokens. And, for unique L1 features like Unified Liquidity, native tokens are offered as rewards to encourage liquidity provision.

Value Unit: The native token issued by a L1 directly or indirectly embodies the value created by the L1. Market participants trade tokens like $ETH based on their valuation of Ethereum's business performance and market position.

2.1.2 The Role of Layer 1 Tokenomics

While tokens have specific roles, the function of tokenomics, which controls token flow, is distinct. The term 'Tokenomics' is often narrowly defined as burn mechanisms to adjust supply or token distribution methods (maximum supply, allocation ratios, unlock schedules, etc.). However, for our discussion, tokenomics encompasses not only burn mechanisms and distribution methods but also incentive systems that align participant interests, token utilities, and revenue distribution models - essentially, the entire economic system based on tokens.

In this context, the fundamental role of tokenomics is to create a system that incentivizes desired behaviors from participants, ensuring the smooth operation of a L1 network. Specifically, it designs reward structures to encourage network-beneficial actions like enhancing security or providing liquidity. For this reward system to be effective, the rewards must hold sufficient value to be meaningful to contributors. Thus, tokenomics must also include mechanisms to regulate token supply and demand to maintain reward value.

Source: X(@alive_eth)

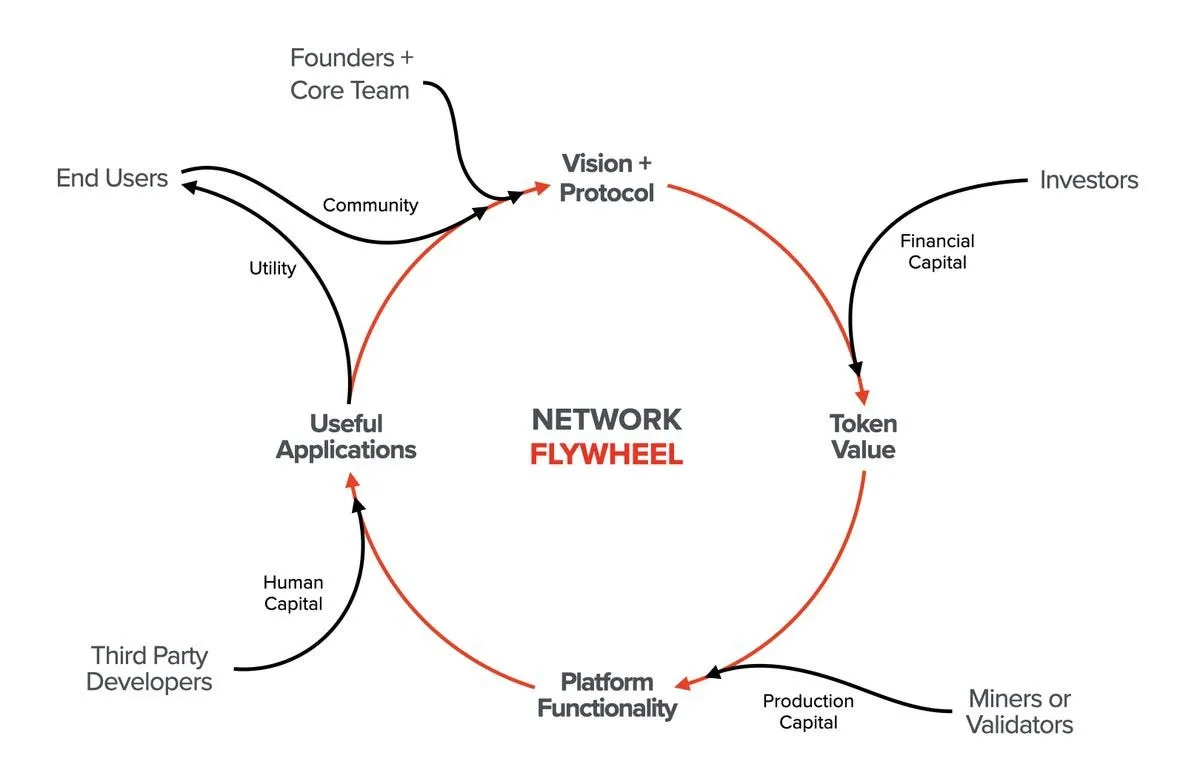

Well-designed tokenomics has the potential to create a flywheel effect, where value circulates to foster organic network growth. This model assumes that the interactions between validators (responsible for blockchain security), developers (creating applications), and users (forming the community) create a circular growth structure. Through the 'network effect', this leads to economies of scale, accelerating network growth. Let's trace the process of the flywheel, from the bottom up:

After the core team suggests a new vision to the market, initial capital completes the basic infrastructure of the L1 network, and token value is generated (in private or public markets).

As token value generates, validators contribute to bootstrapping the supply side of the network in exchange for token rewards. For instance, validators earn block rewards for validating a transaction, providing security and functionality to the network.

Once the L1 network establishes stable functionality and security, developers join to build useful applications on the network.

These applications provide real value to end users, who drive token demand. During this process, a community forms around the users as supporters of the L1 network.

As the network becomes more active and the community grows, demand for tokens increases, both as a reserve currency for network fees and as a value unit embodying the network's worth. Consequently, market demand for tokens rises.

As token demand rises, validators have stronger incentives to support the network's security and functionality → This leads to improved network safety and development environment, encouraging developers to build more useful applications, providing more value to users → Token demand rises → Incentives are strengthened → Network security and functionality improve → Applications develop → Community becomes more active → Flywheel

Once this flywheel starts moving, the L1 network gains momentum for self-sustaining growth. The network no longer needs to be driven solely by the core team; instead, growth accelerates autonomously through token incentives. This flywheel maximizes the potential of tokenomics and is often viewed as the endgame that all tokenomics should ultimately aim for.

Source: X(@alive_eth)

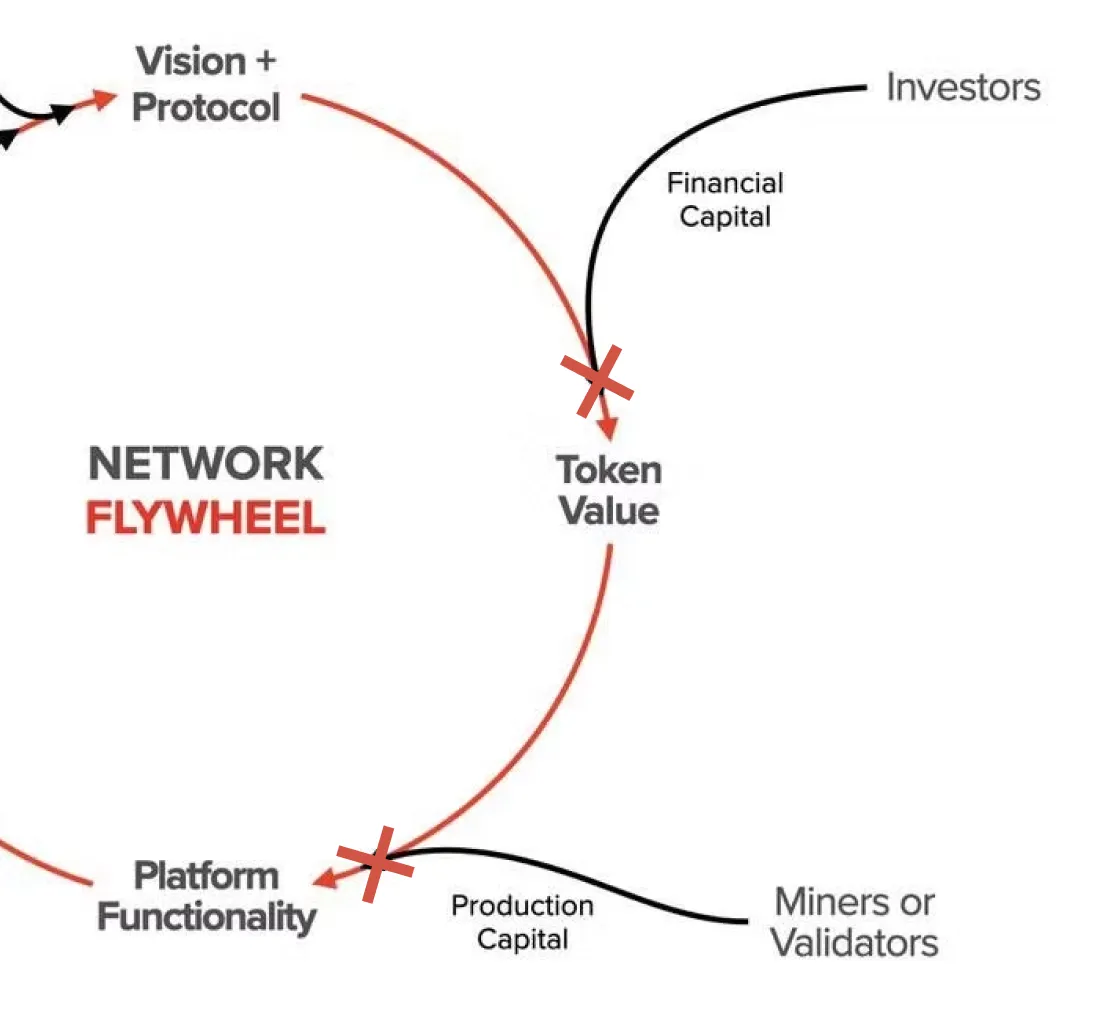

The flywheel model assumes certain facts in creating a circular growth structure. It posits that as network activity increases, token demand grows alongside it, providing a basis for strengthening incentives for ecosystem contributors. It also assumes that enhanced incentives lead validators to contribute to the ecosystem in any ways, fostering an environment for more useful applications. We need to question these seemingly obvious assumptions. Many existing L1 networks appear to struggle with creating sustainable tokenomics, often missing key elements in three aspects:

2.3.1 Are the incentives of all participants truly aligned?

L1 networks involve various types of participants with different interests in the ecosystem. If the structure aligning these complex interests towards growth breaks down, the flywheel stops moving. Particularly, we should question whether validators necessarily contribute to the ecosystem in other ways when token demand increases and their interests are strengthened, as suggested in the flywheel model above.

Validators' interests are not unrelated to ecosystem growth. Their block rewards are given in the L1’s native tokens, so an increase in token demand and value benefits them. Additionally, as the application ecosystem attracts users and generates more transactions, network congestion increases, potentially strengthening validator incentives. Most L1 networks, like Ethereum's PoS network, adopt a gas fee mechanism where validators receive higher fees as network congestion increases.

However, there is no direct mechanism at the network level requiring validators to contribute to the ecosystem, making the relationship between validators and protocols or users weak. The lack of a direct link between strengthened validator incentives and ecosystem activation means there's little motivation for ecosystem contribution. Conversely, in conditions where solo stakers can't earn significant rewards, there's no clear method or incentive for users or protocols to contribute to economic security. The low governance participation rates seen in all L1 ecosystems illustrate the lack of clear motivation for individual users to contribute to network consensus. In other words, the interests of validators are not directly connected to those of other ecosystem participants.

2.3.2 Does network activity increase lead to increased token demand?

It's difficult to assert that token demand necessarily increases as applications emerge and users join, increasing network activity. If there's no inherent structure or only a weak one that correlates network activity with native token demand, network activity and token demand may not align. As will be discussed in detail later, Ethereum is currently experiencing a situation where L2 activity is increasing, but factors driving demand for $ETH are very low. Like Ethereum, each blockchain network will have its unique technical architecture. Therefore, tokenomics should reflect this architecture well.

2.3.3 How do tokens capture value?

Although similar to the previous question, we can pose it differently: how do tokens capture value? Let's assume the flywheel ideally unfolds, and token demand increases with network activation. Does this necessarily lead to an increase in token value? Obviously, increased token demand doesn't automatically mean increased token value. Putting aside market speculation (which operates independently of fundamental ecosystem growth), a simple calculation shows that token demand must exceed newly created token supply for value to increase. Therefore, a mechanism that increases token demand or reduces supply as the network activates should operate in between. This is sometimes overlooked or doesn't work effectively, failing to achieve the feedback loop of network activation → token demand → token value increase.

Summarizing the content so far, L1 tokens function as the network's reserve currency, an incentive tool to encourage contributions, and a value unit embodying the value created by the network. L1 can build tokenomics as an economic system that aligns the interests of ecosystem participants and ensures active network operation through tokens and incentive mechanisms. Well-designed tokenomics has the potential to foster self-sustaining network growth by circulating the value created in the network through token incentives.

However, the token flywheel we often idealize often shows discrepancies with phenomena observed in actual L1 networks. This is because positive feedback loops in the process of inducing participant behavior or connecting value don't work effectively. Specifically, it's because sufficient consideration hasn't been given to whether the incentives of all participants are truly aligned, whether network activity leads to increased token demand, and whether value is accumulating in tokens.

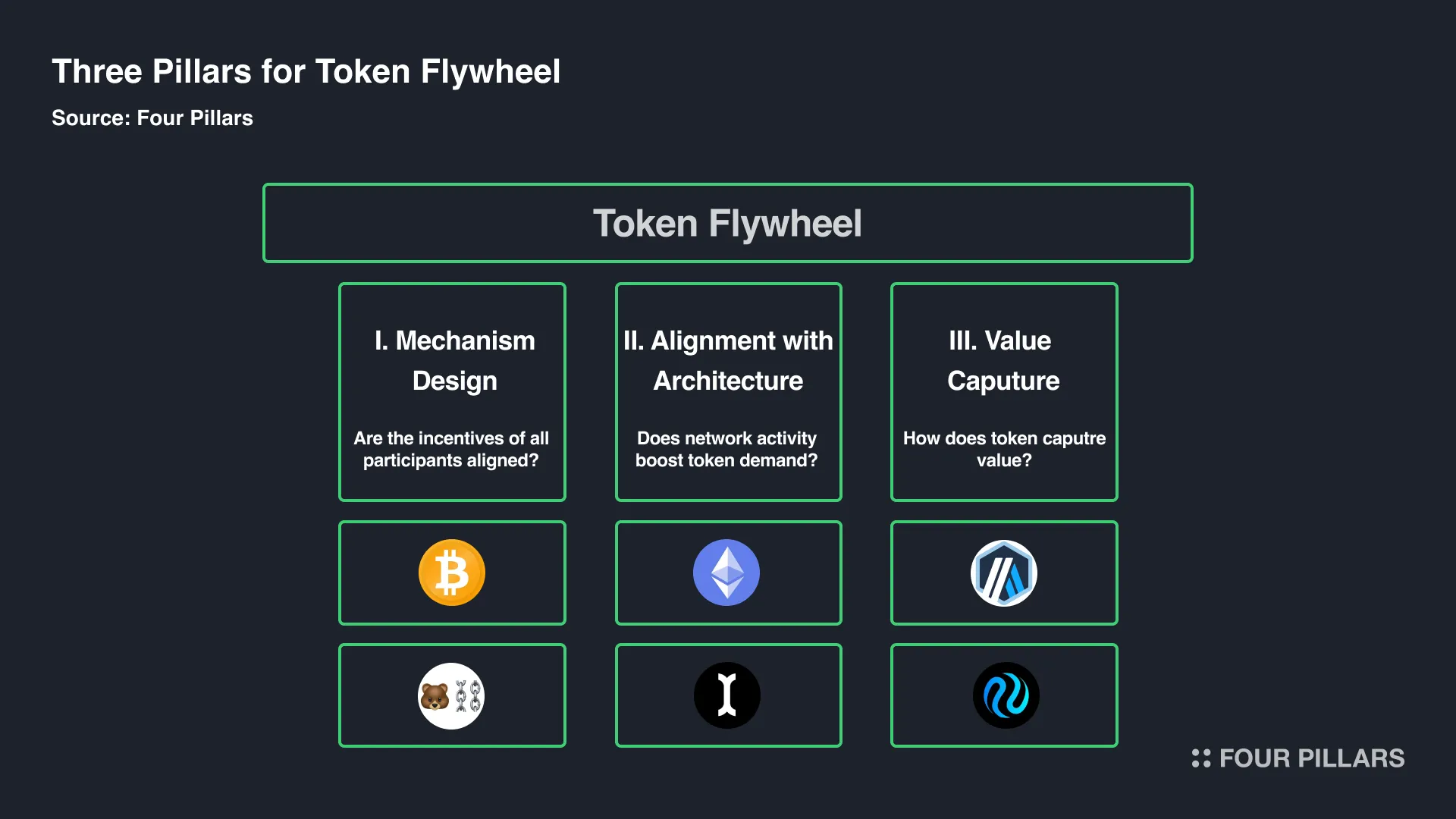

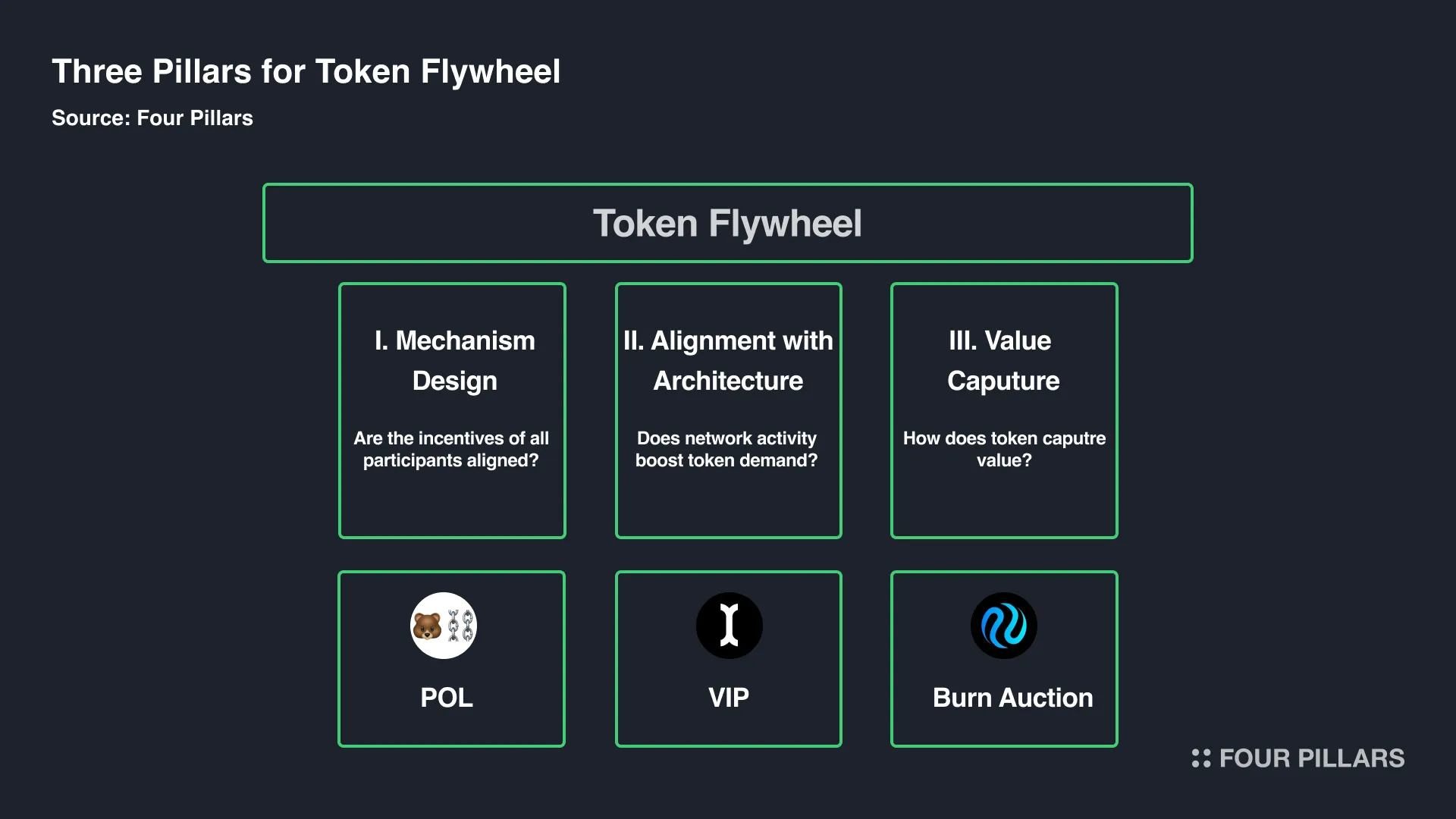

These limitations often cause existing L1 networks to lose tokenomics sustainability in many cases. Therefore, in the process of identifying the direction that the next generation of L1 tokenomics should take, we need to examine these previous limitations more closely by concretizing them. To do this, let's take the questions raised about the token flywheel and convert them into key points for L1 tokenomics design: I. Mechanism Design, II. Alignment with Architecture, III. Value Capture. In the next section, we'll continue our discussion by observing the limitations shown by existing tokenomics and their causes through case studies, while clarifying the above-mentioned key points.

I. Are the incentives of all participants truly aligned? → Mechanism Design

II. Does network activity increase lead to increased token demand? → Alignment with Architecture

III. How do tokens capture value? → Value Capture

Given the complexity of tokenomics, judging tokenomics cases based on a single factor might lead to the error of interpreting the phenomenon fragmentarily. Nevertheless, as one method of finding sustainable tokenomics, attempting to define the limitations encountered by existing cases and derive lessons can be a good approach. Let's examine 1) the limitations faced by Bitcoin in terms of mechanism design, 2) the alignment problem between architecture and tokenomics revealed in Ethereum, and 3) the structural limitations of Arbitrum's token in not capturing value from the network, to concretize the three pillars of tokenomics that support the flywheel.

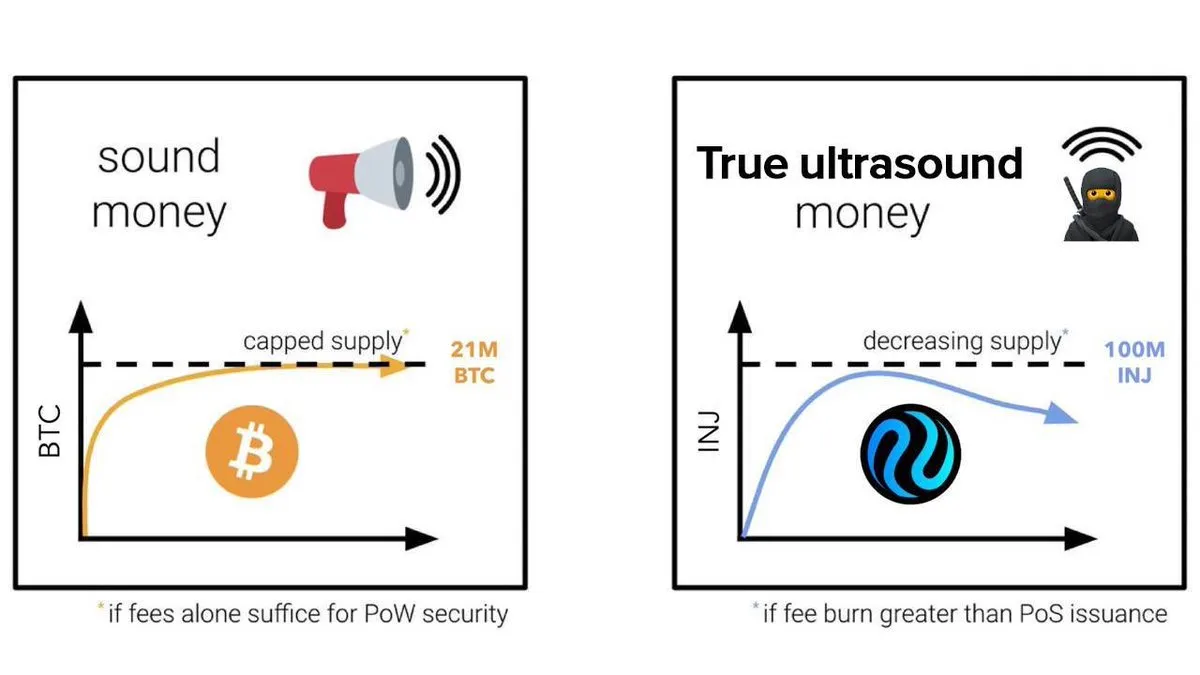

Bitcoin is one of the most innovative inventions since the emergence of blockchain and has now become an important asset even in traditional financial markets. However, there is a significant gap between Bitcoin's intended function at its inception and its current role. As Bitcoin's asset role has evolved, the initial incentive mechanism design no longer aligns with its current function, leading to concerns about the lack of incentives to maintain Bitcoin's security in the future. This reality is reshaping Bitcoin's development roadmap. Let's take a closer look at Bitcoin's case, focusing on mechanism design, which can be summarized as "how much reward to provide, how to provide it, and what behavior to induce from participants."

3.1.1 Bitcoin Tokenomics: The Premise of Halving

To summarize Bitcoin's mechanism, it aligns network security with node incentives by rewarding mining nodes that generate valid blocks while adhering to rules under the PoW (Proof of Work) consensus algorithm. Nodes participating in the network compete to compute hashes, expending computing power to earn block rewards for adding valid blocks to the longest chain. For a malicious node to attack the network, it would need to control over half of the computing power dedicated to PoW. This is practically difficult, and even if achieved, the attacker would lose motivation as the attack would decrease Bitcoin's value, resulting in their own loss. Through this dynamic, Bitcoin achieves Byzantine Fault Tolerance (BFT), operating as a decentralized monetary system through node consensus without requiring third party trust.

Source: Bitocoin Wiki

Therefore, the block reward received by mining nodes is crucial for maintaining Bitcoin's decentralization and security, as it serves as an incentive for nodes to act honestly and participate competitively in the Proof of Work process. However, a closer look at Bitcoin's reward mechanism reveals that to limit inflation, block rewards are halved approximately every four years and will eventually cease to be emitted. Consequently, miners will increasingly rely on transaction fees rather than inflationary block rewards.

This halving reward mechanism was designed with the assumption that Bitcoin would eventually settle as a payment currency, with transaction fees fully replacing mining rewards. Unlike its current perception as a 'Store of Value' (SoV), Bitcoin's inception was driven by a mission to replace centralized electronic payment systems. However, as is well known, Bitcoin faces scalability issues for use as a payment currency, and solutions like USDC or USDT are already sufficient alternatives for payment currencies.

In response, suggestions have been made that Bitcoin needs to modify its strategy, and solutions for Bitcoin's mining incentives can be summarized as follows. One scenario is that as Bitcoin's supply becomes increasingly limited, its scarcity naturally increases, potentially resolving the issue. Ultimately, as Bitcoin evolves into a true store of value, its value could rise significantly, providing sufficient incentive for block generation even without mining rewards. Another solution involves developing Bitcoin as a programmable asset and network through initiatives like BTCFi or Bitcoin L2. This approach aims to make Bitcoin a more productive asset rather than 'lazy digital gold', increasing transaction fees generated within the Bitcoin network.

3.1.2 The Importance of Mechanism Design as Highlighted by Bitcoin

While discussions about Bitcoin's scalability are ongoing, the possibility that future miner incentives might be absent, contrary to the initial tokenomics design, raises crucial questions about Bitcoin's sustainability. If mining rewards eventually cease, no one would expend computing power to gain block generation rights, potentially leading to a situation where Bitcoin transactions are no longer recorded on the blockchain. Consequently, the market has developed a new mission to gradually increase transaction fees to replace mining rewards by making Bitcoin a more productive asset. This has become an important task, driving the influx of developers and the expansion of the Bitcoin ecosystem.

Bitcoin's case underscores the importance of mechanism design in tokenomics - "how much reward to provide, how to provide it, and what behavior to induce from participants." Here, mechanism design refers to the approach of setting up situations and incentives so that tokenomics participants act to maximize their own returns. Mechanism design is also called 'Reverse-Game Theory'. While game theory predicts how individuals will make strategic decisions to act in their best interests, reverse-game theory designs optimal mechanisms where individuals pursuing their own interests collectively achieve an arbitrary goal. In other words, it ensures that validators responsible for network security, protocols, and users achieve smooth operation and sustainable growth of the L1 network, even as they pursue their maximum benefits while participating in the ecosystem.

Alignment with architecture can be defined as whether the blockchain's technical structure and the economic model supporting it are compatible. L1 networks adopt different structures in their technical architecture, from consensus algorithms to transaction computation structures and the presence of L2. For example, L1 networks with specific goals, such as Monad blockchain aiming for high-performance EVM networks through parallel transaction processing, or Story network specialized in IP tokenization, require unique technical architectures. However, is adjusting the architecture alone sufficient? As the architecture changes, the types of participants in the network and their interests also change, necessitating the optimization of the economic model to match the architecture. From this perspective, we can examine whether the architecture and tokenomics are align, and Ethereum's recent challenges in tokenomics sustainability provide a case study for multi-faceted consideration of this topic.

3.2.1 Ethereum Tokenomics: Layer2s are parasitic to Ethereum

Source: X(@glxyresearch)

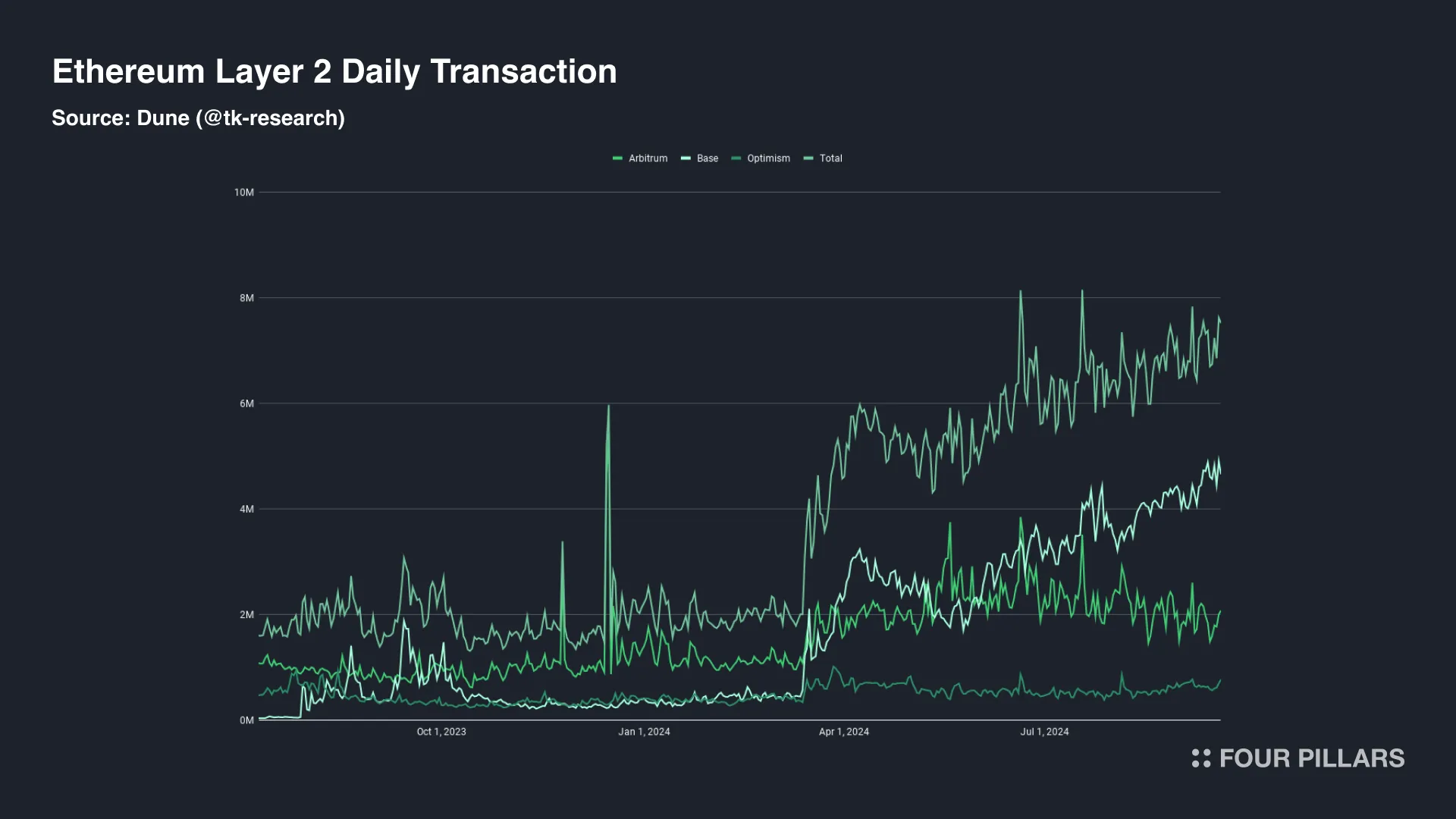

Ethereum has built the largest ecosystem among all blockchain networks, based on its rich liquidity and developer community. However, recently, Ethereum has faced concerns about its economic model, where the value of L2 does not accrue to the Ethereum main chain and $ETH. The issue stems from the significant reduction in DA (Data Availability) fees paid by L2 when sequencing transaction data to Ethereum following the EIP-4844 update. This has led to a corresponding decrease in demand for $ETH as a gas token. In other words, as L2 pays less to Ethereum, Ethereum's revenue decreases, and simultaneously, a fundamental demand factor for $ETH disappears, leading to the opinion that "L2 is economically parasitic to Ethereum."

Source: Dune(@blockworks_research)

To examine the background in more detail, Ethereum distinguishes gas fees into a base fee determined by network congestion and a priority fee set arbitrarily by users. Of these, the priority fee is provided as a reward to validators, while the base fee is burned. As a result, when the total base fees generated in Ethereum exceeded the amount of newly emitted block rewards, sufficient $ETH was burned, maintaining the total $ETH supply in a deflationary state. The fact that the absolute amount of $ETH circulating in the market was continuously decreasing has been recognized in the market as supporting the fundamental demand for $ETH as an asset.

Source: Dune(@tk-research)

However, Ethereum aims for a L2-centric roadmap in the long term, leading to the EIP-4844 update to lower sequencing costs and increase L2 scalability. Changes have occurred since this update. As evident from the significant increase in L2 transactions and unique active addresses, end users can now use L2 applications with lower network fees instead of Ethereum. On the other hand, Ethereum has gained a structurally 'disadvantageous' position compared to L2. Despite L2 activation, Ethereum's average gas fee has dropped to 1 Gwei, leading to an inflationary state in $ETH supply. This has led to criticism that L2 is economically parasitic to Ethereum.

3.2.2 The Need for Alignment Between Architecture and Economic Model as Demonstrated by Ethereum

Ethereum continues to upgrade its architecture to complement the main chain's lack of scalability through L2. This raises a question: Isn't Ethereum achieving its goals well, given that its scalability has significantly improved and L2 activity has indeed increased? Ethereum has declared a rollup-centric roadmap and aims for a blockchain environment with high scalability while maintaining sufficient decentralization. Therefore, the situation where L2 operating costs have been reduced and end-user convenience has improved since EIP-4844 might align with Ethereum's architectural upgrade goals.

However, Ethereum's case shows the problems that arise when technical architecture and economic models do not align, even considering this as a transitional phase in Ethereum's development towards a L2-centric roadmap. While the L1 has improved its architecture to address its mission, and usability and activity have increased accordingly, the link between the value generated from this activity and the economic model is broken. The connection between L2's expanded scalability and Ethereum's economic benefits is missing. Proposals like EIP-7762 to increase blob fees paid by L2 suggest a potential regression in L2 scalability, indicating that Ethereum has hit a situation where the growth curves of architecture and economic model do not align.

This demonstrates that tokenomics cannot be considered separately from the architecture that L1 has built. If a L1 has a clear problem to solve and a mission to achieve, its technical architecture would have been constructed as a methodology for this. Then, tokenomics design optimized for that architecture should accompany it. This issue is more likely to occur in modular blockchains with a risk of economic fragmentation. Beyond Ethereum, the Cosmos IBC ecosystem has also given rise to various app chains based on its unique technical architecture, but it maintains a fragmented ecosystem without a value chain that economically links the app chains into a single economic system. In other words, if there are uniquely formed interests of ecosystem participants as the architecture is developed, an optimized economic model for that is also required.

Value Capture refers to the mechanism by which tokens capture value from the network. Even if the network becomes highly active, a mechanism that directly adjusts token supply and demand is needed to increase the fundamental demand for tokens. The phenomenon where Arbitrum and $ARB lack a connection, resulting in the token not capturing value, well illustrates the importance of a value capture mechanism.

3.3.1 Arbitrum Tokenomics: Layer 2 Tokens are Meme Tokens

Arbitrum currently shows the highest activity among all L2 networks, with about 700 protocols in its ecosystem and generating about 5 million transactions weekly. However, compared to its high network activity, $ARB faces criticism for being no different from a meme token, lacking utility beyond governance functions. Consequently, it lacks factors for fundamental demand recognized in the market. While various market variables complexly affect token prices, making it difficult to interpret price fluctuations simplistically, token mechanisms that create willingness to buy or hold tokens long-term play an important role in market participants' assessment of token value. In fact, $ARB's price has not escaped a downward trend, showing a YTD -66% down, and according to IntoTheBlock, 95% of current $ARB holders are recording losses.

In response, Arbitrum DAO recently passed a proposal to introduce staking functionality for $ARB. The proposal's core is to allow delegation of governance rights through ARB token staking and strengthen the staking reward system. First, staking $ARB will enable earning interest from various revenue sources such as sequencer fees, MEV fees, and validator fees. Moreover, by introducing liquid staking, $ARB depositors can interoperate $stARB with other DeFi protocols while maintaining their staking status.

This tokenomics update allows for various expected effects. Arbitrum DAO's treasury has accumulated $45 million worth of $ETH, but less than 10% of the circulating supply of $ARB is used in governance. Therefore, strengthening the motivation for governance delegation through $ARB staking provides an opportunity to improve governance security. Another important effect is creating a willingness for token holders to hold $ARB long-term.

3.3.2 The Importance of Value capture Mechanisms as Highlighted by Arbitrum

Value capture involves accumulating network value in tokens, either by distributing network-generated revenue to ecosystem contributors through tokens or by adjusting token supply directly or indirectly. Value capture is important not only for L2 or DeFi protocols, as seen in the Arbitrum case, but also in L1 tokenomics. Particularly for L1 native tokens, which serve as incentives to induce ecosystem participants to act beneficially for the network, the token must be perceived as a reward of appropriate value to expect sufficient contributions from participants.

The method for tokens to capture value is implemented through mechanisms that align network demand with token supply and demand dynamics. For example, if network revenue is used to buy tokens from the market and burn them, the absolute quantity of tokens supplied to the market decreases. Alternatively, there's also a method of directly redistributing network-generated revenue to stakers. Such value capture mechanisms, which create fundamental demand factors for tokens or adjust the quantity of tokens circulating in the market, can create a virtuous cycle. This cycle can lead to L1 activation resulting in token value increase, which strengthens incentives for contributions, further increasing L1 activity.

Up to this point, by examining existing tokenomics cases, we have been able to clarify three key points for creating a token flywheel. Of course, it will take a long time before Bitcoin's block rewards completely disappear, making it a distant concern for now. Ethereum and Arbitrum are engaged in heated discussions to address their current issues, leaving room for improvement in the future. Nevertheless, the limitations encountered by existing tokenomics offer valuable lessons. There is a risk of losing tokenomics sustainability when incentives for ecosystem contributions are absent, when economic models do not align with technical architecture, or when network activity fails to translate into token value growth.

However, meeting all these criteria is not as easy as it sounds. The common solution proposed by Berachain, Initia, and Injective is to directly engage at the network level to adjust the interests of participants or design tokenomics tailored to the technical architecture. Alternatively, they attempt to overcome the limitations shown earlier by adjusting token supply and demand through unique mechanisms. This strategy of deeply engaging in tokenomics at the network level has the potential to effectively complement the gaps in the flywheel that existing tokenomics have missed. From here on, let's examine how Berachain aims to solve problems through its sophisticated mechanism design of PoL, how Initia plans to economically connect the fragmented rollup ecosystem through VIP, and why Injective has been able to maintain a deflationary state of its token for an extended period.

Mechanism design involves designing a system where L1 participants, while pursuing their maximum benefits, ultimately contribute to the active operation and sustainable growth of L1. Berachain, specializing in this aspect, has newly proposed PoL (Proof of Liquidity) as a consensus algorithm that solves the problem of misaligned interests by tightly interweaving the interests and reward systems of ecosystem participants.

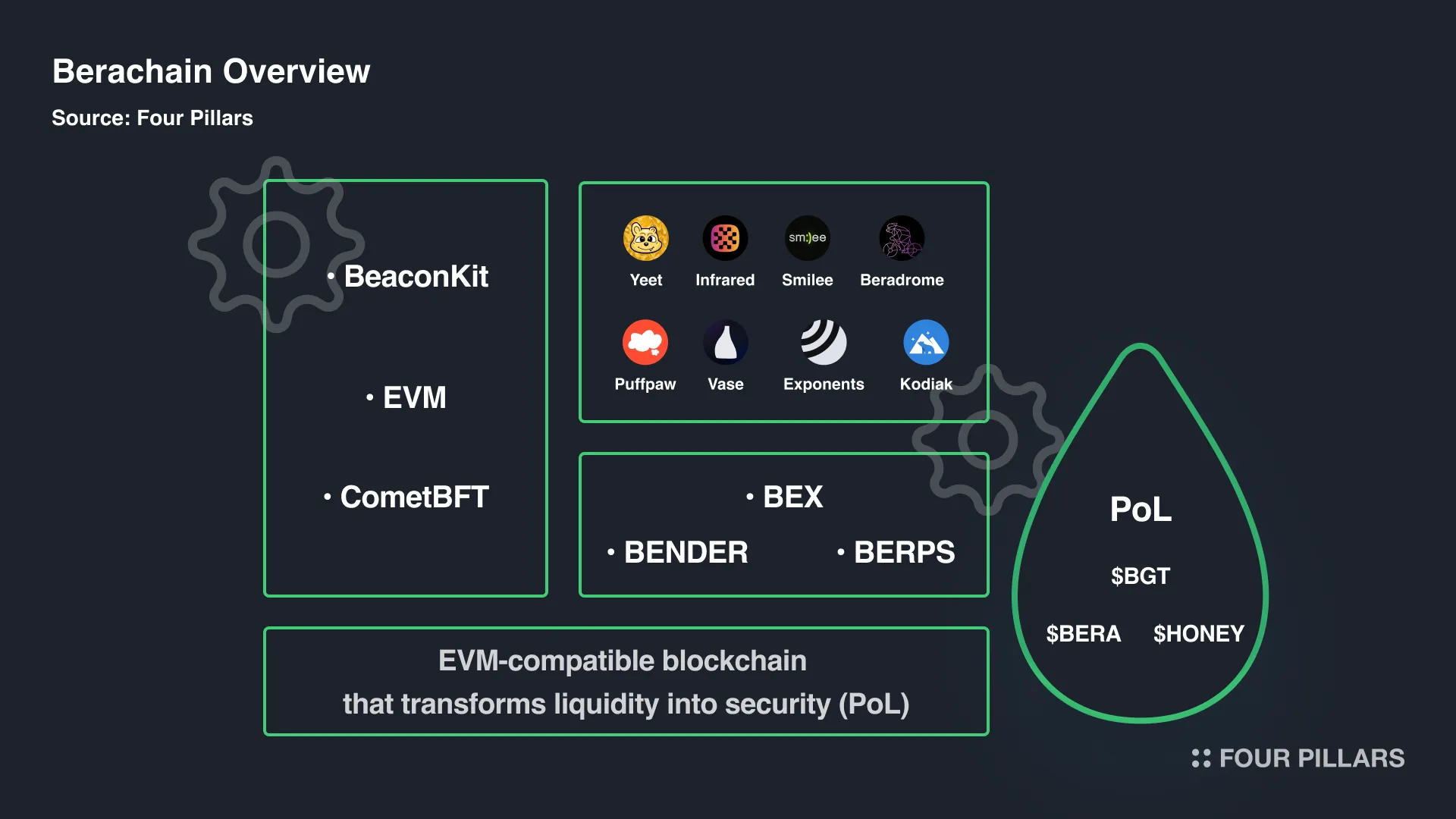

4.1.1 Berachain Overview

Berachain is constructed as an EVM-compatible L1 blockchain using BeaconKit, which is developed by modifying the Cosmos SDK. Similar to Ethereum's Beacon Chain structure, Berachain uses BeaconKit to separate the execution layer and consensus layer, utilizing ComtBFT for the consensus layer and EVM for the execution layer, ensuring high compatibility with the EVM execution environment. With its solid technical prowess, Berachain has been building up its community and development environment over an extended period, starting with the NFT project Bong Bears. As a result, despite still being in the testnet stage, various protocols have onboarded, and it shows high community engagement.

4.1.2 Berachain Tokenomics

Berachain's uniqueness can be found in PoL, which adjusts the interests of participants at the network level. PoL is a consensus algorithm specifically designed to secure both liquidity and security stably and strengthen the role of validators within the ecosystem. It specializes in mechanism design where each ecosystem participant prioritizes their own interests while promoting network growth under mutually dependent relationships. Let's examine how Berachain aligns the individual interests of 1) users, 2) validators, and 3) protocols to a single point of intersection for growth.

Source: Berachain Docs

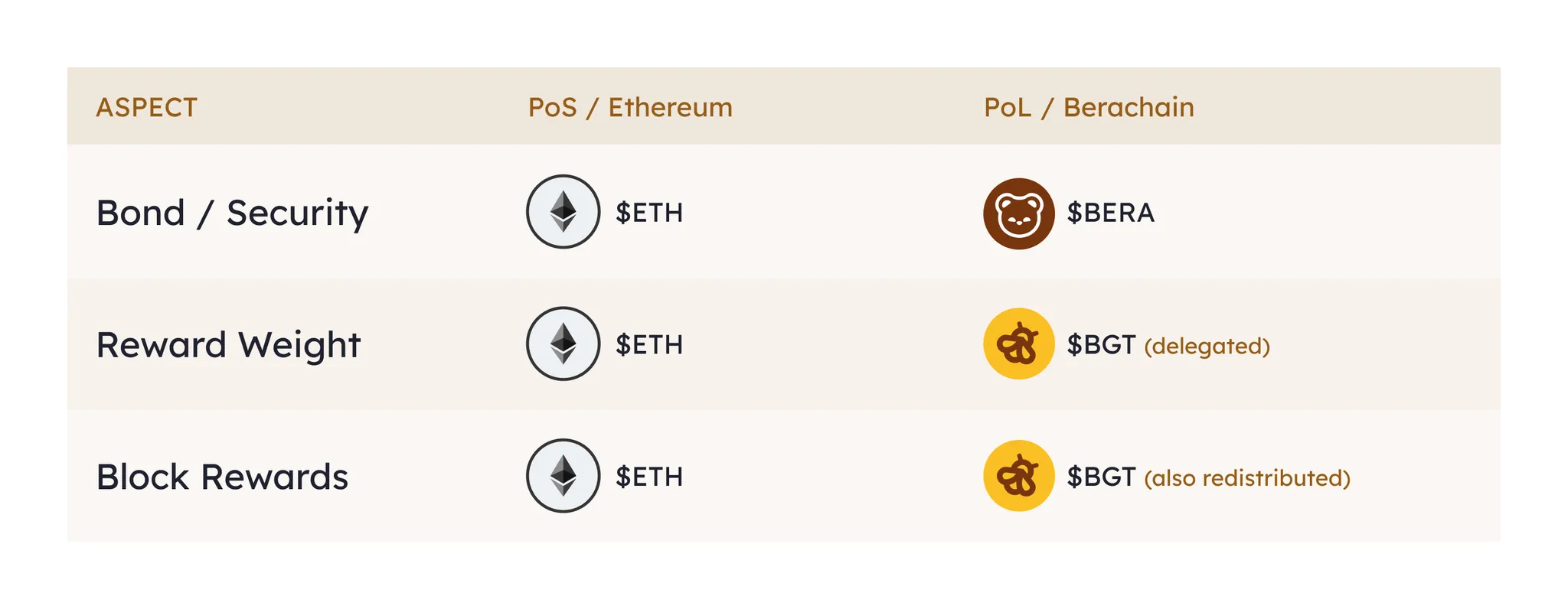

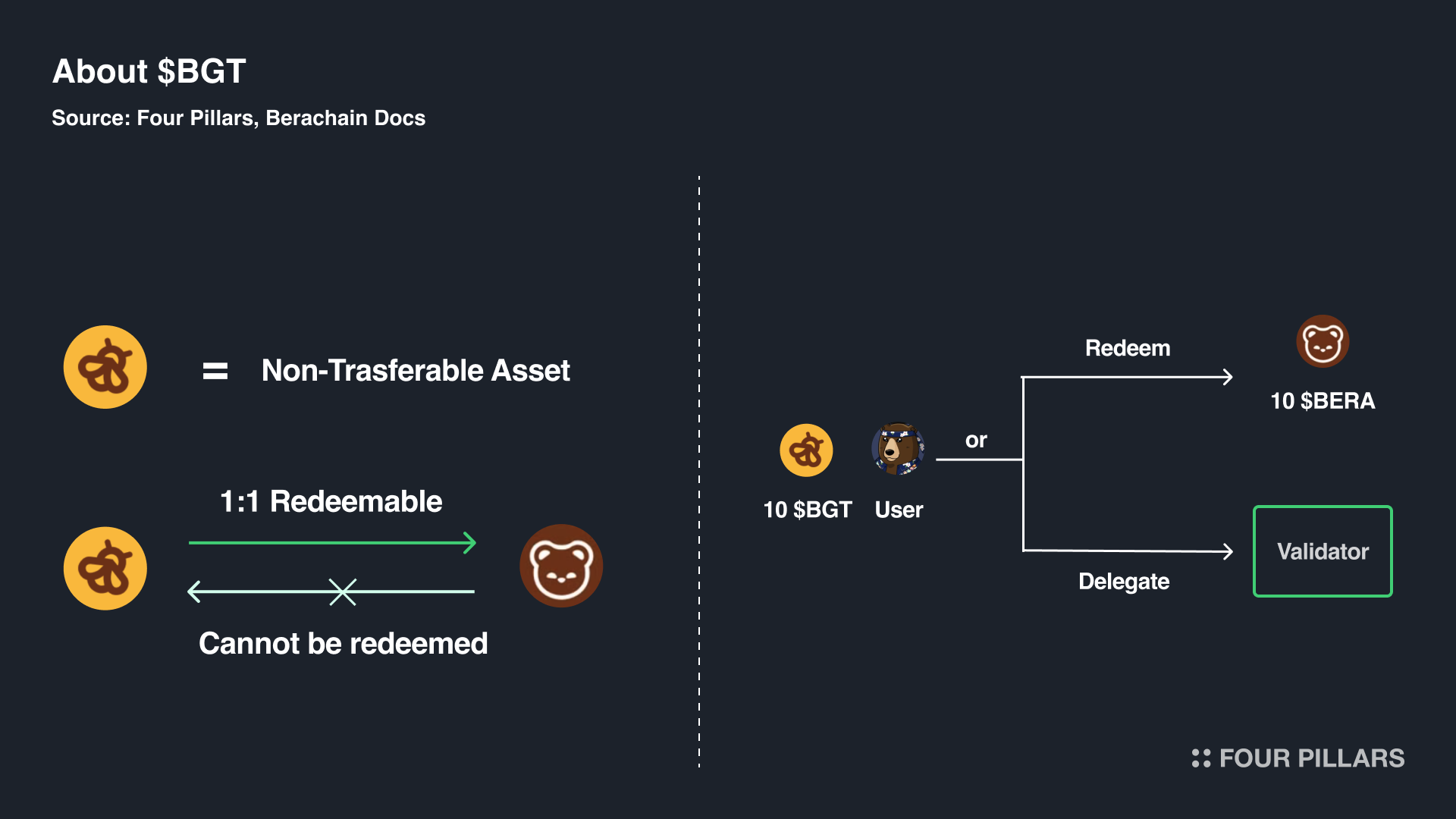

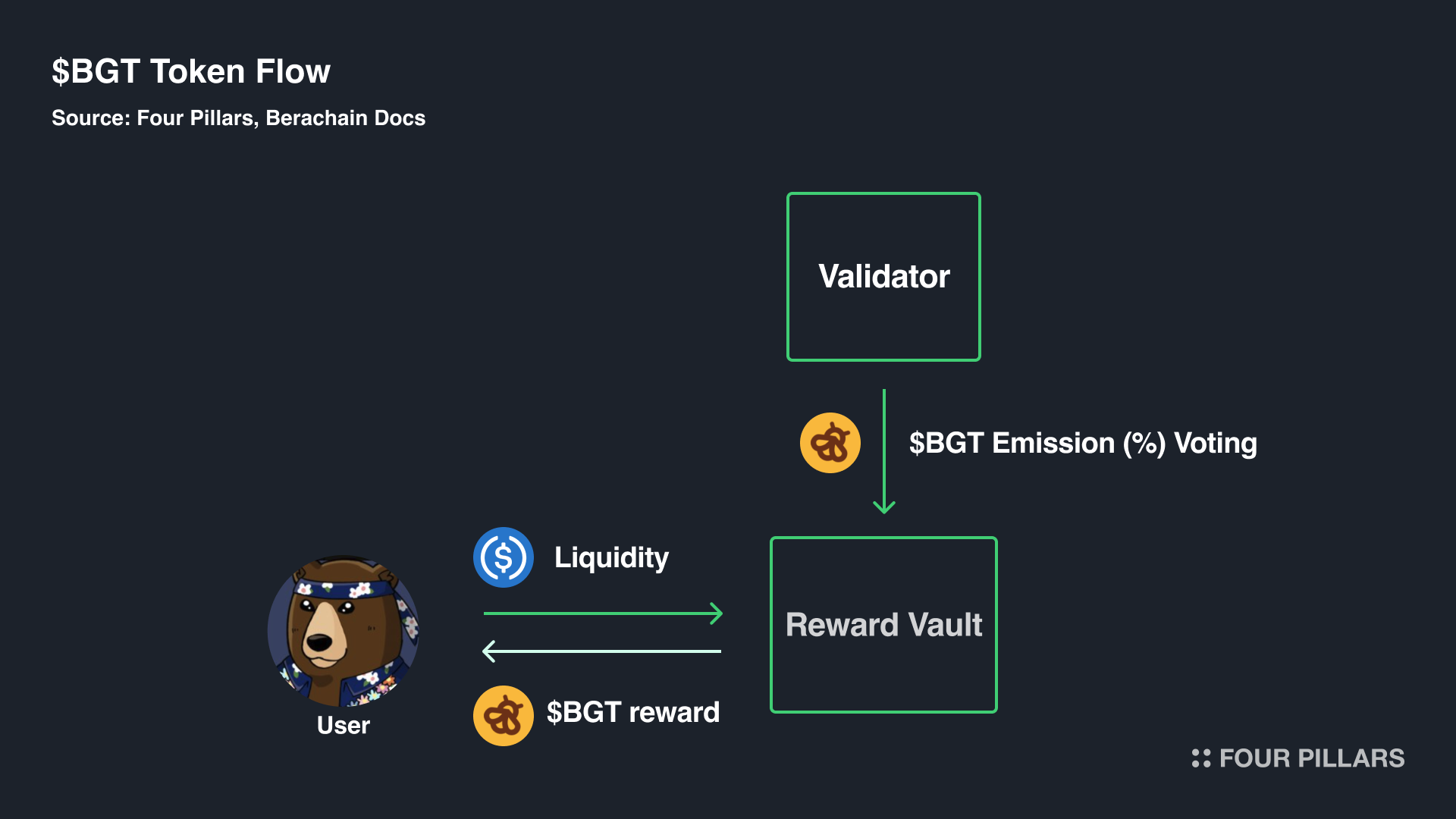

First, Berachain has three tokens - $BERA, $BGT, and $HONEY - each playing different roles to operate PoL. $BERA functions as the gas token used for network fees, $BGT (Bera Governance Token) serves as a reward for providing liquidity and as a governance token determining reward ratios. $HONEY is Berachain's native stablecoin pegged 1:1 to $USDC. While Berachain has this triple tokenomics, we'll focus on $BERA and $BGT for now to simplify our discussion of the PoL participant structure. To understand Berachain's mechanism design, we need to focus more on $BGT's special functions.

$BGT is a token that can be received as a reward for providing liquidity to whitelisted liquidity pools (Whitelisted Reward Vaults), as determined by governance. $BGT is provided in a non-tradable state tied to the account, and while the $BGT received as a reward can be exchanged 1:1 for $BERA, the reverse ($BERA → $BGT) is not possible. Therefore, providing liquidity is the only way to obtain $BGT.

The way $BGT is supplied is determined by validators voting on how much $BGT emission to allocate to which liquidity pool. Users who obtain $BGT have two options: one is to exchange $BGT for $BERA to liquidate it, and the other is to delegate it to validators for additional rewards. Here, additional rewards refer to bribes that flow from protocols through validators to users, which we'll detail later.

The reason Berachain separates the gas token and governance token into $BERA and $BGT is to secure both liquidity and security in the ecosystem. In L1 networks using a single token, staking tokens to increase PoS security limits the amount of tokens available as liquidity in the ecosystem. Therefore, by making it possible to obtain $BGT, which is used for security, only by providing liquidity, Berachain aims to solve the problem of inconsistency between network liquidity and security. Also, by allowing validators to allocate $BGT emission ratios, it strengthens the structure where ecosystem participants' interests are aligned by increasing the interdependence between validators and protocols and users.

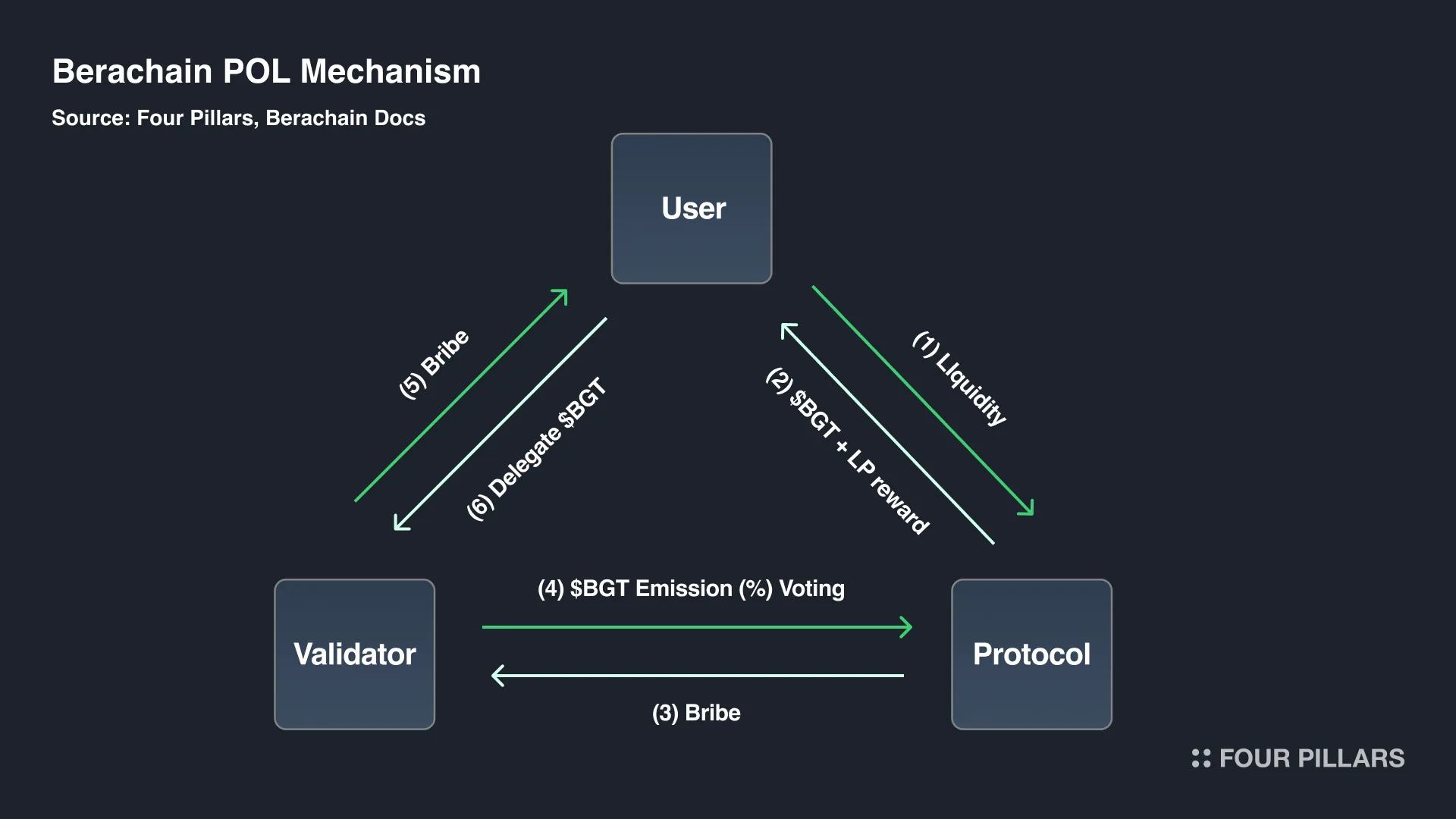

Now that we understand the basic principles of PoL and the roles of $BERA and $BGT, let's examine how ecosystem participants interact under this mechanism design. Follow the flow of $BGT, liquidity, and bribes from (1) to (6) in order to understand how ecosystem participants interact under certain interests.

User ↔ Protocol

(1) Liquidity: Users deposit liquidity into a whitelisted liquidity pool of their choice. The protocol uses this pool's liquidity to provide a smooth trading environment for protocol users.

(2) $BGT + LP reward: When users provide liquidity to a whitelisted pool, the protocol provides $BGT rewards and liquidity provision rewards for the pair deposit. Here, the protocol needs to secure as much $BGT emission ratio as possible to make users choose its liquidity pool.

Protocol ↔ Validator

(3) Bribe: Validators have the governance right to determine the $BGT emission ratio for liquidity pools. Therefore, protocols provide bribes to validators to vote for their liquidity pools.

(4) $BGT Emission Voting: Unlike other L1s, Berachain's validators don't directly receive L1 tokens supplied according to the inflation rate as network validation rewards. Instead, they earn incentives for network validation (excluding priority fees that may occur irregularly) through bribes provided by protocols. Therefore, to receive sufficient bribes from protocols, they need to secure more $BGT to have stronger governance rights.

Validator ↔ User

(5) Bribe: The way for validators to secure stronger governance rights is to receive delegation of $BGT that users obtained through liquidity provision. To do this, they need to provide bribes received from protocols back to users or provide separate incentives to increase the amount of $BGT delegated.

(6) Delegate $BGT: Users delegate $BGT to validators in exchange for bribes received from validators.

4.1.3 The Direction of Tokenomics Proposed by Berachain's Mechanism Design

In conclusion, Berachain aims to secure both ecosystem liquidity and security through PoL, and solve the problem of validators' separated interests. Moving beyond the existing approach where a single token serves all roles as the base currency, Berachain distinguishes between $BERA for liquidity and $BGT for governance, addressing the trade-off between liquidity and security. By structuring validators to receive rewards through bribes and giving them the authority to determine $BGT emission quantities, it strengthens the interdependence between validators, protocols, and users.

Of course, as the complexity of the mechanism increases, there's a drawback of a steeper learning curve for end users. Therefore, it's necessary to closely observe whether interactions centered on PoL will occur smoothly after the mainnet launch. Nevertheless, Berachain's tokenomics, which is sophisticated in terms of mechanism design, presents a significant direction for L1 tokenomics by addressing the issue where misaligned participant incentives were breaking the continuity of the flywheel.

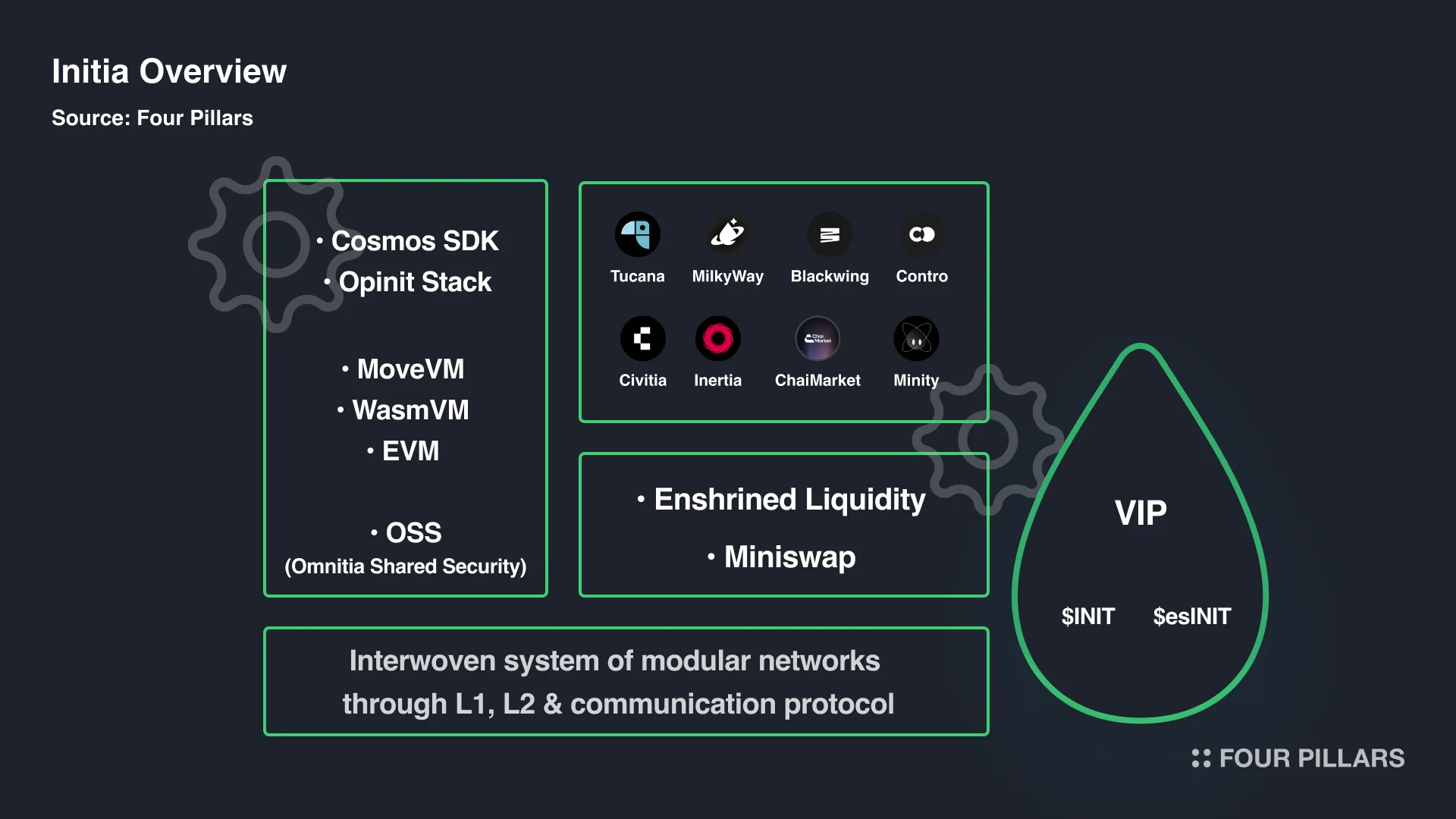

Initia is expected to complement the problem of misalignment between architecture and economic models that occurs when architecture is built to align with the network's direction. Initia focuses on the fragmentation problem faced by existing rollup ecosystems. In line with its mission of "Interwoven Rollup," it aims to build an ecosystem where L2 Minitias are distributed around Initia while being tightly interconnected economically and in terms of security. As part of this effort, it attempts to connect the potentially fragmented rollup ecosystem economy through its unique tokenomics called VIP.

4.2.1 Initia Overview

Initia is a Cosmos-based Layer 1 blockchain powered by MoveVM, specifically designed to serve as a settlement layer for Layer 2 rollups called Minitia. Initia (L1) and Minitia (L2) connect each other economically and in terms of security, forming an integrated ecosystem called Omnitia. Therefore, various functions of Initia are all created to strengthen connectivity with Minitia L2. For instance, in terms of security, If fraud occurs within Minitia, Initia's validator nodes intervene to resolve disputes along with Celestia, which rebuilds the last valid state. In terms of liquidity, it operates a liquidity hub called Enshrined Liquidity at the L1 network level, which Minitia can use to support smooth asset movement and swaps between Minitias for users through the router function of Enshrined Liquidity.

4.2.2 Initia Tokenomics

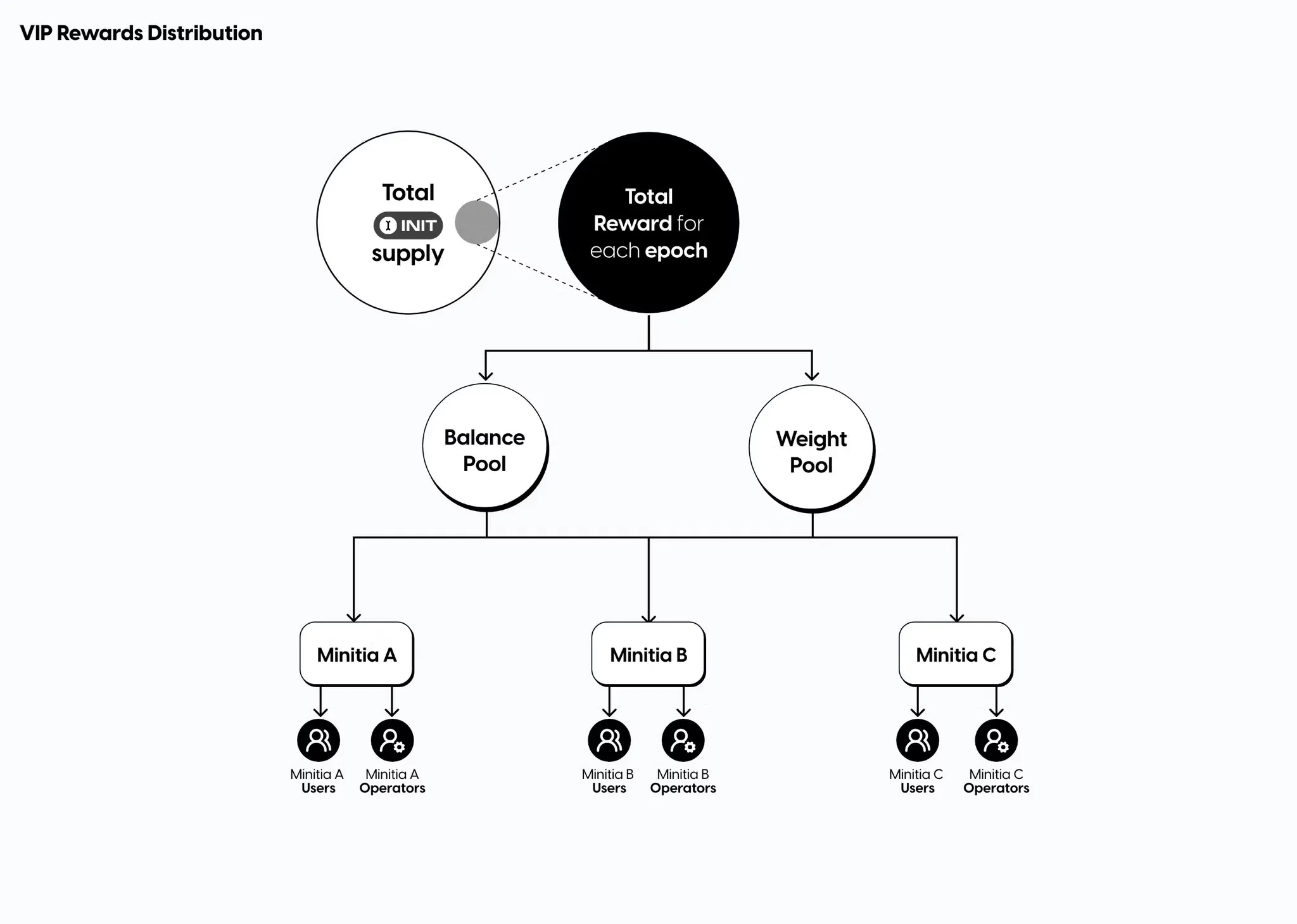

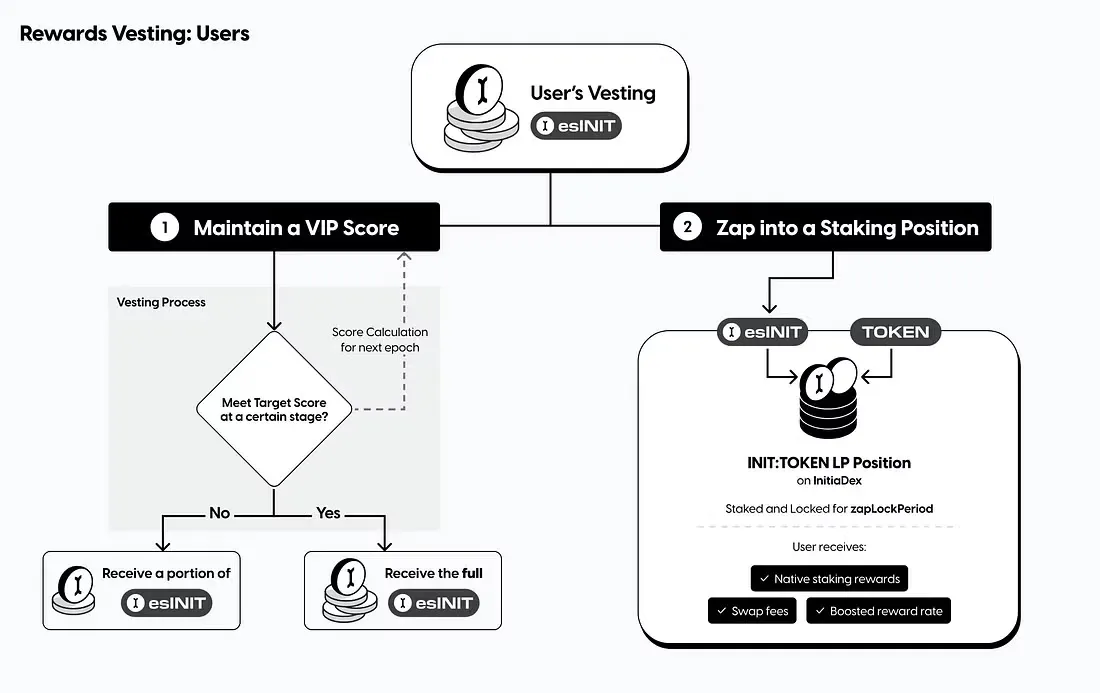

As Initia is designed with a focus on mutual connectivity with Minitia L2, it has devised a mechanism called VIP (Vested Interest Program) for economic connectivity with Minitia. VIP aims to make $INIT, the base currency of the Initia ecosystem, an essential part of all L2s. Through this, it uses $INIT as a method to economically connect Initia and Minitia and continuously create use cases for $INIT. The VIP process can be broadly divided into three parts: 1) allocation, 2) distribution, and 3) unlock.

1) Allocation

Source: Introducing VIP

First, 10% of $INIT's genesis supply is allocated as funds for VIP. These funds are distributed every two-week epoch to Minitias and users eligible for VIP rewards. Here, VIP rewards are distributed in a divided state according to two pools: the Balance Pool and the Weight Pool. Balance Pool rewards are allocated to Minitias in proportion to the amount of $INIT they hold. On the other hand, Weight Pool rewards are allocated to Minitias according to weights set through gauge voting in L1 governance. In other words, L1 stakers determine how much reward to allocate to each Minitia through gauge voting. Thus, the Balance Pool encourages Minitias to hold more $INIT and create use cases for $INIT in their applications, while the Weight Pool creates a use case for $INIT tokens through gauge voting and encourages validators, users, or bribe protocols like Votium or Hidden Hand to actively participate in L1 governance.

2) Distribution

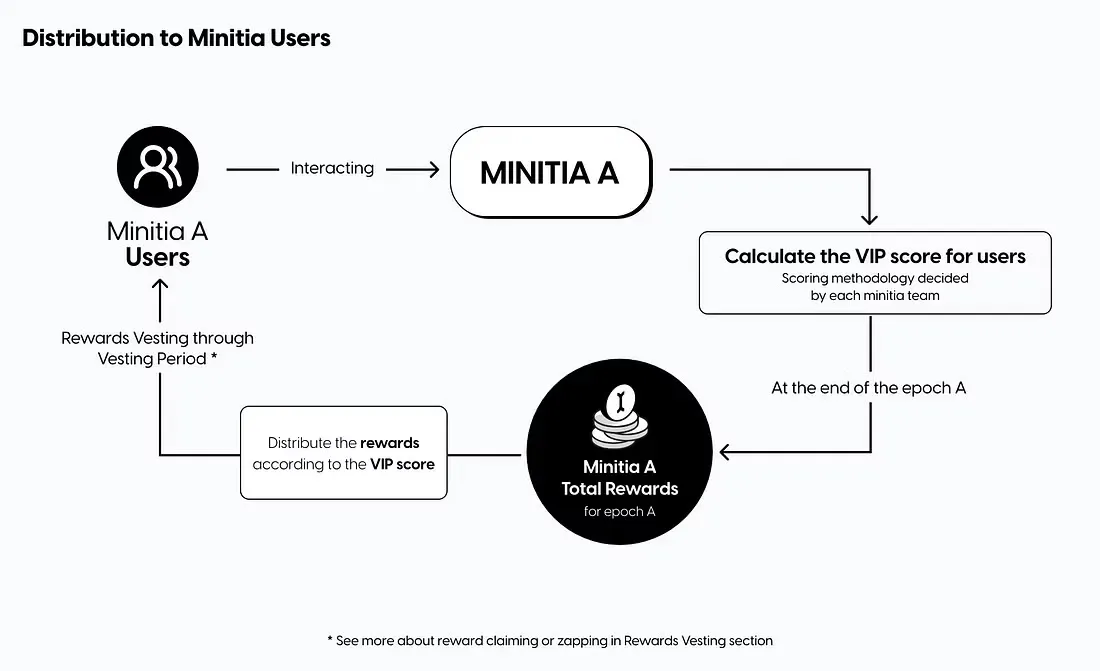

Source: Introducing VIP

Rewards allocated to Minitias are provided as $esINIT (escrowed INIT), which is non-transferable in its initial state. The recipients of $esINIT allocated to Minitias are divided into operators and users. Here, operators refer to the project teams operating Minitias. Project teams receiving operator rewards can utilize $esINIT in various ways. They can use it as development funds to complement Minitia, redistribute it to users active in Minitia, or stake it in Initia L1 for self-voting in future epoch gauge voting.

On the other hand, $esINIT distributed as user rewards is directly provided to users according to their VIP score. The VIP score is a figure calculated according to various KPIs set by Minitia to encourage user interaction in Minitia. For example, by setting criteria for VIP scores such as the number of transactions, trading volume, or borrowing scale that users generated through Minitia during a specific epoch, Minitia can provide motivation for users to perform specific actions.

3) Unlock

Source: Introducing VIP

As mentioned above, when rewards are distributed to users according to VIP scores, $esINIT is given as an escrow token that cannot be transferred. Therefore, users need to go through an unlocking process to liquidate the $esINIT received as a reward. At this point, users can choose one of two actions to maximize their benefits. One is to maintain their VIP score over multiple epochs to unlock $esINIT into liquid $INIT. During this period of maintaining the VIP score, users can accumulate additional scores in Minitia, and from Minitia's perspective, this has the advantage of inducing user retention. Another way to utilize $esINIT is to deposit it as a liquidity pair in Enshrined Liquidity to receive rewards for the deposit.

4.2.3 The Direction of Tokenomics Proposed by Initia's VIP

In summary, VIP is Initia's tokenomics designed to economically connect L1 and L2 and create continuous demand for $INIT. In the 1) allocation process, it aims to increase use cases for $INIT and encourage governance participation as a way to activate the ecosystem by providing devices such as Balance Pool and Weight Pool with different distribution methods. In the 2) distribution process, it aligns the interests of Minitia and users by allowing Minitia to induce specific user behaviors through VIP scores. And the 3) unlock process functions as a device to induce user retention or direct contribution to the Initia ecosystem through liquidity provision.

Through this process, Initia aims to prevent the economic fragmentation of the Minitia ecosystem while creating multifaceted use cases for $INIT and generating factors for fundamental token demand accordingly. As modular blockchain-centric infrastructure becomes more common, the economic fragmentation of ecosystems is recognized as a chronic problem that must be traded off against the benefits of modular-based development environments. In this regard, the VIP proposed by Initia presents a meaningful direction for designing tokenomics in future modular ecosystems.

Unlike Berachain and Initia, which haven't even launched their mainnets yet, Injective has been known in the market since 2018. However, it has consistently improved its tokenomics even until very recently through updates like INJ 3.0 and Altaris, building a unique deflationary tokenomics with its burn mechanism. Therefore, when discussing L1 tokenomics in terms of value capture, I thought it was a noteworthy use case and wanted to introduce it in this section.

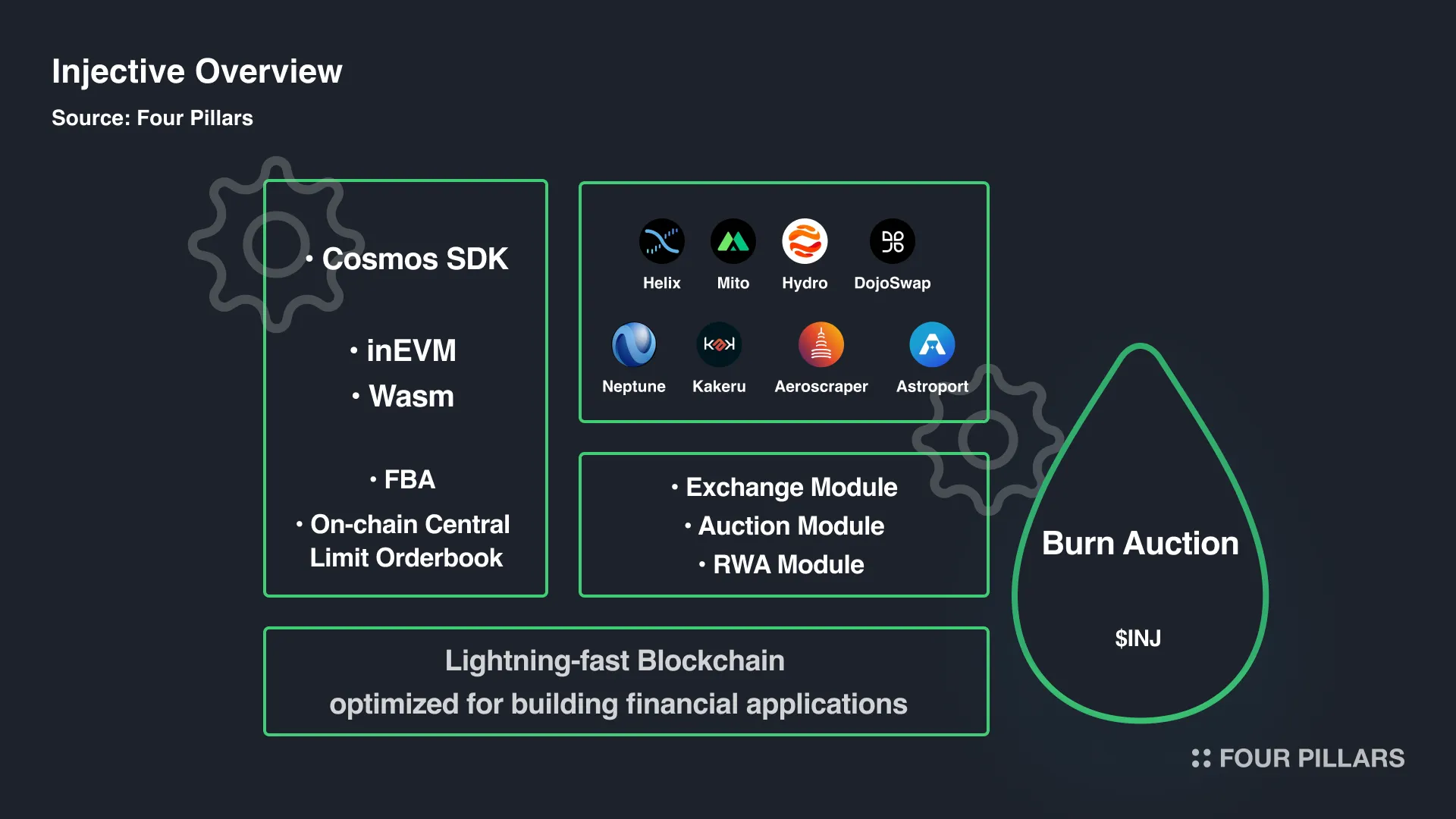

4.3.1 Injective Overview

Injective is a L1 blockchain built based on the Cosmos SDK and custom consensus mechanism based on TendermintBFT, optimized for finance from spot trading to perpetual futures trading or RWA. As a L1 built for finance, it provides a blockchain environment with high performance of over 25,000 TPS to handle high-frequency trading, and utilizes on-chain order matching models like FBA (Frequent Batch Auction) to prevent MEV for capital-efficient trading. Additionally, Injective provides plug-and-play modules as part of its development resources. Particularly, using the Exchange Module, processes such as order book operation, trade execution, and order matching can be easily handled, and financial service environments can be built without the effort of attracting separate liquidity by utilizing the built-in shared liquidity in Injective.

4.3.2 Injective Tokenomics

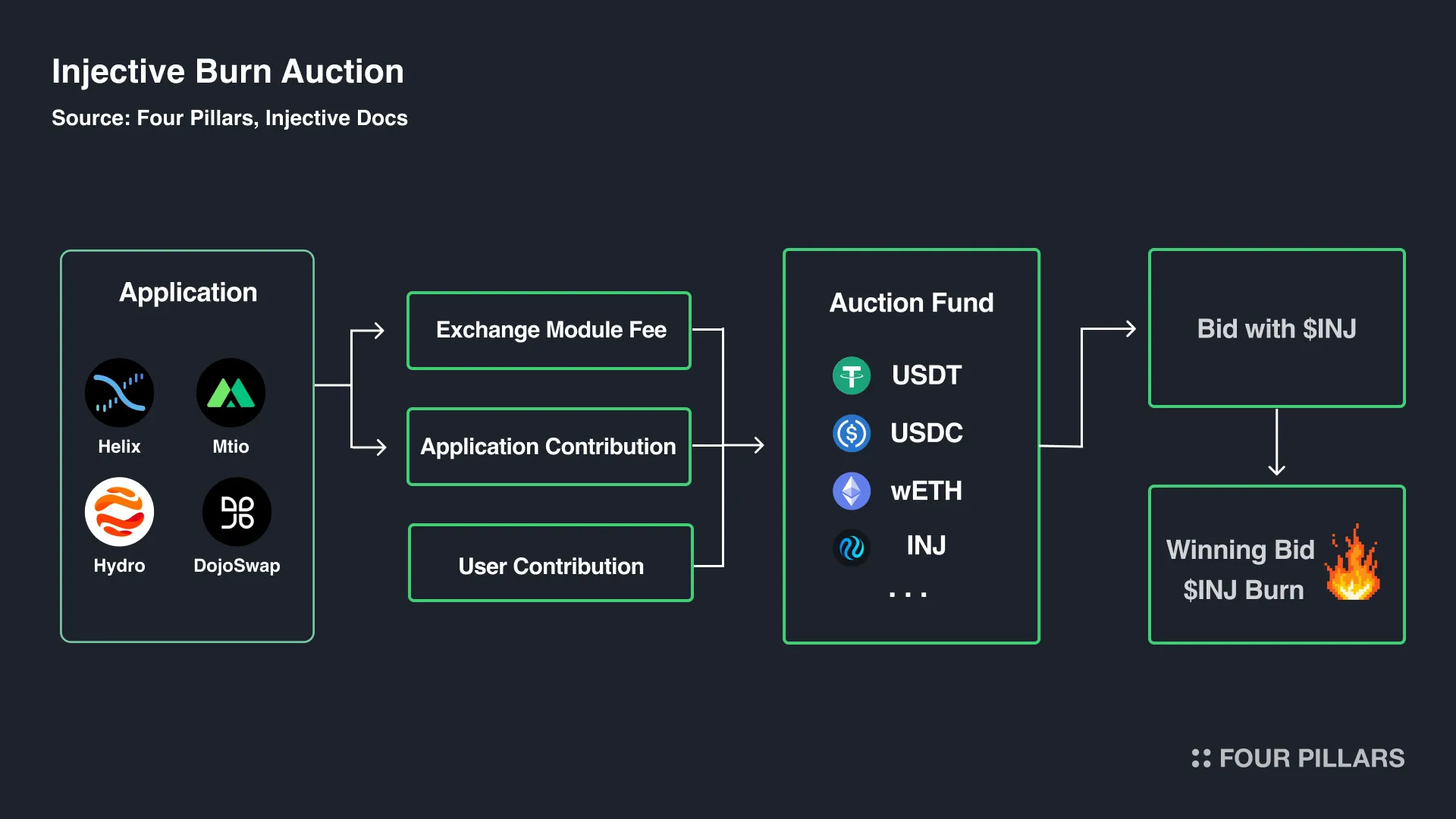

Source: X(@Injective)

IInjective is known for its tokenomics that achieves deflation through a burn auction designed to reduce the circulating supply of $INJ in the market. The burn auction process works as follows: when assets accumulate in an auction fund from a portion of the revenue generated by Injective's applications or direct contributions from individual users, these assets are put up for auction where they can be bid on with $INJ. Once the auction is completed, the winning bidder exchanges their $INJ used for bidding with the tokens in the auction fund, and the $INJ used for bidding is burned, removing that amount of $INJ from the total token supply. Injective conducts these auctions weekly, and as of October 2024, 6,231,217 $INJ (~$142,000,000) of the total token supply has been burned through auctions.

To delve deeper into the burn auction procedure, it's conducted through the Auction Module, which handles processes such as bidding, winner determination, and $INJ burning, along with the Exchange Module. First, the auction fund assets are gathered through three routes. One is that a portion of the revenue from applications using the Exchange Module is transferred to the auction fund. Another is that applications not using the Exchange Module can transfer a nominal amount or a certain percentage of fees to the auction fund. Lastly, individual users can independently contribute to the auction fund.

The assets accumulated in this auction fund are mainly accumulated as USDT, USDC, or $INJ, and anyone can participate in the auction for this fund using $INJ. Auction participants have the opportunity to acquire the fund's assets at a slightly discounted price, for instance, winning a $100 worth auction fund with $95 worth of $INJ, naturally leading to bidding competition. Finally, the successful bidder exchanges their $INJ used for bidding with the tokens in the auction fund, and the $INJ used for bidding is burned.

4.3.3 The Direction of Tokenomics Proposed by Injective's Burn Auction

Injective's burn auction accumulates fees generated from the Exchange Module for bidding, creating a structure where the amount of $INJ burned increases as trading through the Exchange Module increases. Consequently, as Injective's trading activity rises, the circulating supply of tokens in the market decreases, allowing the token to capture value from the network. Thus, Injective aligns ecosystem growth with tokenomics value enhancement through its burn mechanism and appears to continue strengthening its growth-driven token burn mechanism in the future.

While most blockchains have a mechanism to burn a certain portion of network fees, few L1 networks adjust token supply as intuitively as Injective. Particularly, as most blockchains except Bitcoin and Ethereum (mainnet) are being developed with the premise of low gas fees, token burn mechanisms based on network fees show limitations in conducting significant amounts of burning. Injective also aims for near-zero transaction fees, recording an average fee of $0.0003 per transaction. In this context, the burn auction, which can conduct significant amounts of burning while maintaining low gas fees, aligns with the user environment that future L1 networks aim to develop, and Injective is proposing the most noteworthy use case in this regard.

Up to this point, we have examined the limitations faced by existing tokenomics and cases of improved tokenomics, identifying potential directions for the next generation of tokenomics. Notably, Berachain, Initia, and Injective show a common trend: they are enhancing their tokenomics through unique mechanisms implemented at the network level. Each project is building tokenomics that leverage their strengths in terms of mechanism design, Alignment with architecture, and value capture.

So, as we conclude, what constitutes ideal tokenomics for a L1? Is there an absolute tokenomics framework that moves the token flywheel? To answer this question, we've considered tokenomics as a comprehensive system that includes not just token-related discussions, but also the mission the L1 aims to solve, its technical architecture, and the behavior patterns of ecosystem participants. The key insight from this process is that tokenomics alone is merely an idea. The value of tokenomics manifests in the actual interactions between various elements that make up the L1 network and its participants.

Therefore, we need to shift our perspective from 'what is ideal tokenomics' to 'what makes an ideal L1, and what role does tokenomics play within it?' From this viewpoint, in my opinion, a L1 with great potential is an ecosystem where the mission, architecture, protocols, and tokenomics are organically connected with consistent logic and create synergy.

A clearly defined mission

Technical architecture built to faithfully reflect the mission

An ecosystem filled with protocols & applications optimized for the network's development environment or architecture, which could be called 'Only Possible on 000 Chain'

As a result, offering differentiated value to users

Tokenomics, which is missing from this list, doesn't exist independently but acts as a lubricant that moves the gears of architecture and protocols smoothly. Diagnosing the L1 networks we've examined today with this framework yields the following:

Berachain has devised a unique consensus algorithm called PoL to create an EVM-compatible L1 network that converts liquidity into security, and developed its own framework like Polaris that's compatible with EVM. On top of this, projects are emerging such as Infrared which liquidates $BGT, a non-tradable asset, Smilee Finance which hedges Impermanent Loss to offset the risks of PoL that must focus on liquidity provision, and Yeet Bonds which allows protocols to secure liquidity autonomously (Protocol Owned Liquidity) through bond product sales, minimizing resources spent on liquidity bootstraping (liquidity mining, bribes) and enabling self-voting to secure $BGT emissions autonomously. When these components are combined with PoL, which is both Berachain's purpose and means, and the tri-tokenomics of $BERA, $BGT, and $HONEY, we can expect the construction of a unique ecosystem where validators, protocols, and users create synergy and grow together.

Initia is a L1 network built for "Interwoven Rollup," aiming to solve the problem of fragmentation in modular blockchains. To this end, it has built various architectures to strengthen the connectivity between Initia and Minitia, from the Opinit Stack, a Minitia framework for building rollups based on Initia, to Enshrined Liquidity for securing Minitia's liquidity, and OSS (Omnitia Shared Security), a shared security framework for Minitia's fraud proofs. Based on Initia's architecture, Minitias specialized for modular infrastructure are emerging, including Tucana, an intent-based DEX that integrates liquidity from modular networks, and Milkyway, which aims to provide restaking services based on Initia. Here, the VIP tokenomics has the potential to create a virtuous cycle economy where Minitia accumulates value created in Initia, and Initia in turn increases Minitia's activity.

Injective has a technical architecture optimized for financial application development, faithfully reflecting its goal of being 'The Blockchain built for Finance'. Based on a high-performance blockchain environment to handle high-frequency trading, it supports plug-and-play modules that can be used for financial application development, from the Exchange Module providing shared order books and shared liquidity to Auction, Oracle, Insurance, and RWA modules. Injective houses various financial applications and products developed using these diverse modules. The on-chain orderbook exchange Helix, which provides a trading environment comparable to CEX by utilizing the Exchange Module, and the case of launching a tokenized index for Blackrock's BUIDL fund using Injective's built-in RWA oracle, I believe, well demonstrate what's 'Only Possible on Injective'. Here, Injective's tokenomics, the burn auction, plays a role in aligning ecosystem growth with tokenomics value enhancement, promoting more killer applications.

From this, we can say that these projects have the conditions for the components of the L1 network and tokenomics to create synergy and grow together. Of course, as Berachain and Initia have not yet officially launched, it's necessary to closely observe the interactions that will occur in the ecosystem from a long-term perspective. In particular, both chains are preparing tokenomics that are quite complex. Therefore, careful consideration from various angles will be needed to effectively lower the high learning curve that users will face and ensure that tokenomics can be executed as intended during the actual implementation process.

Meanwhile, Injective's tokenomics particularly requires the activation of the application ecosystem as the most critical precondition. Currently, Injective shows an average of 2-3 million daily transactions and a cumulative trading volume of $39.2 billion, indicating high activity and maintaining a stable $INJ burn rate. Going forward, the activation of financial products and applications that actively utilize the unique features of a finance-specialized chain, such as the BUIDL index or 2024ELECTION perpetual market, will continue to play a crucial role in maintaining the unique deflationary model inherent in Injective's tokenomics.

Is the crypto industry still a 'narrative game' without substance? Looking at the recent crypto industry, the atmosphere seems quite different. As the scale of the RWA market led by large institutions like BlackRock and Franklin Templeton has reached $12 billion, the influx of traditional institutions is accelerating, and market participants are paying attention not only to short-term narratives but also to the actual cash profitability and revenue distribution mechanisms of protocols like Uniswap or Aave. Given this status, fundamentals are becoming an increasingly important topic in the crypto industry.

When fundamentals become more important, tokenomics is undoubtedly the core criterion for evaluating the fundamentals of L1 networks. Based on the discussions we've had in this article, we can diagnose the fundamentals of tokenomics by examining whether network activity sufficiently leads to token demand, whether ecosystem participants actively interact for their own benefits centered around tokens, and whether these interactions converge into network growth. Furthermore, whether such tokenomics not only exists as an idea but also plays a role in synergy with various components of the network could become an increasingly important framework for judging the fundamental value of L1 in the future.

In this context, the reason to pay attention to Berachain, Initia, and Injective introduced today is that they attempt to overcome the limitations of existing models by directly engaging in tokenomics at the network level. Injective maintains unique tokenomics in terms of enhancing token value through its deflationary mechanism, while Berachain's PoL and Initia's VIP present a blueprint for L1 tokenomics in unprecedented ways. Considering the reality where many past L1 projects remain as 'zombie chains', I think the naively drawn token flywheel hardly moved. On the other hand, whether these new approaches actually build sustainable ecosystems and achieve the endgame of the flywheel will be an important point to watch in determining the next stage of L1 tokenomics.

Dive into 'Narratives' that will be important in the next year